Fast Takeoffs and Hard Landings: Ten31 Timestamp 938,757

Sovereign is he who decides the model weights

Another Saturday morning, another regime change strike on a key marginal producer of oil for China dangerous threat to Freedom and Democracy. Following last month’s Midnight Maduro Madness, President Trump greeted Americans this morning with news of an extensive attack on Iran coordinated alongside Israel, ostensibly to “defend the American people by eliminating imminent threats” from the current regime. The President explicitly encouraged the Iranian people to “take over the government” in the wake of the US’s attacks and expressed willingness to ramp up involvement to a degree that might include American casualties, a fairly radical shift from the “no new wars” tenor of Trump’s first term (though early reports suggest much of the country’s key leadership may have already been eliminated). While our security clearance is too low to grant us much insight on all the motivations driving what seems to be a politically unpopular military excursion, we have to imagine it doesn’t hurt that the successful installation of a US-friendly Iranian government – which, if the history of regime change wars tells us anything, should be a total walk in the park – would potentially boost American leverage in the ongoing soft decoupling from China.

The Pentagon also made stateside headlines this week through a highly public and acrimonious conflict with frontier AI lab Anthropic over the company’s attempts to place “safety” controls on what its models and tools licensed to the DoW will and won’t do. This press release war seemed to conclude with the White House directing the Pentagon to cease use of Anthropic products, but we think these two headlines are more intertwined than consensus may appreciate, as they jointly point in the same direction of the US government aggressively moving to reassert wartime control over (and potentially expand the definition of) its sphere of influence. Against a backdrop where Substack AI Doomposting can send stocks of the biggest companies in the world into freefall; where tech companies are beginning to tout benefits from large AI-driven cost rationalizations; and where the Executive Branch is consistently maneuvering to both subtly and kinetically undermine its main geopolitical rival, this week’s Hegseth/Amodei showdown sets up an interesting question of who actually has sovereignty over what increasingly looks like incredibly powerful, society-altering technology. The Trump administration’s attitude toward outright industrial policy and direct equity stakes in massive companies over the past year suggests to us that if you’re building a superweapon in US borders – and that weapon happens to be, for now, the country’s main technological edge against a rival that produces basically everything else – you shouldn’t be surprised when the US government declares you the junior partner. At the risk of beating a dead horse, we continue to believe these secular megatrends have significant implications for globally accessible liquid assets that can be held without counterparty risk.

Selected Portfolio News

AnchorWatch launched a wide array of customizable Vault options – including multi-institution support soon – as well as optional insurance policies, Coldcard integrations, and more:

Fold announced balance sheet updates to simplify its capital structure, enhance operational flexibility, and reduce potential dilution:

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Media

Maple AI Co-Founder Mark Suman joined What Bitcoin Did to discuss the rapid advancements in the AI landscape.

Ten31 Advisor and Zaprite Head of Business Development Parker Lewis appeared on What Bitcoin Did as well to discuss bitcoin’s role in the changing global monetary order.

Market Updates

The White House got everyone’s weekend off to a nice start with another Saturday morning dictator deposition, announcing overnight that the US military has initiated major strikes on Iran. President Trump’s address to the nation suggested the attacks are intended to defend the US against “imminent threats,” though after the ostensible total destruction of the country’s nuclear program last summer, it’s not entirely clear what those threats might be.

That said, we’d keep an eye on Iran’s status as a key marginal supplier of oil for China, as the country’s independent refineries reportedly turned to Iran to backfill some supply in the wake of last month’s Maduro ouster from Venezuela.

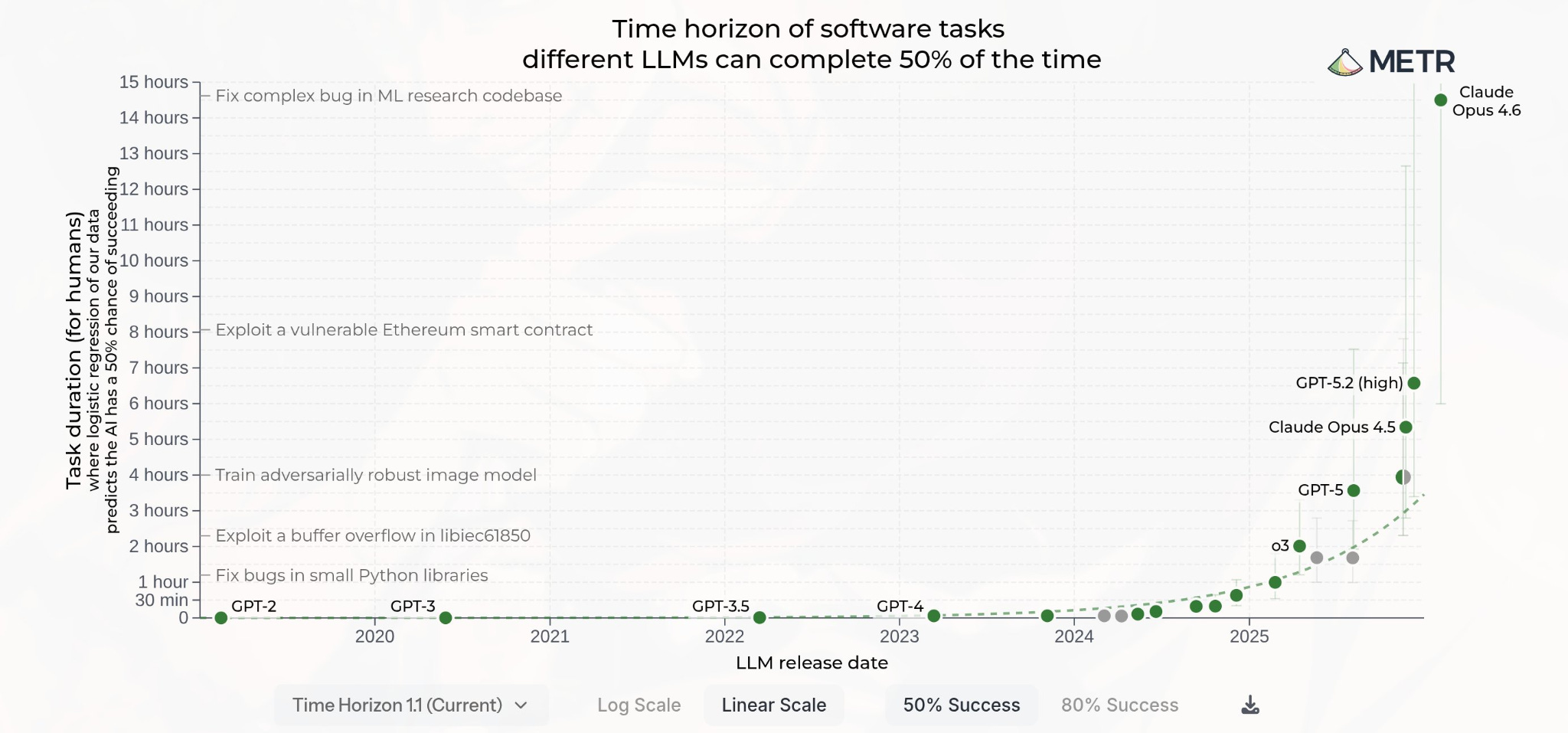

The headlines weren’t much more encouraging earlier in the week, as independent research firm Citrini posted a widely circulated report highlighting the potential for massive disruption to wide swaths of the economy from rapid advancements in AI.

While the report largely highlighted scenarios that terminally online AI maxis have been ranting about for years, and various Wall Street shops quickly responded with obligatory takedown pieces, the report was apparently fresh enough to send stocks from Blackstone to DoorDash to Visa reeling on Monday morning.

Fed Governor Chris Waller shrugged off the concerns, arguing that the risks of AI to the labor market are overstated, which is very comforting coming from the institution that gave us “subprime is contained.” His colleague Lisa Cook, meanwhile, suggested she’s not so sure.

It was a bit of an awkward week, then, for fintech giant Block to announce it will cut its workforce by nearly 50% thanks to productivity gains delivered by AI tools. This announcement sent the stock up nearly 25%, which will no doubt give other executives with large org structures something to think about.

To be fair, Block CEO Jack Dorsey has freely admitted to overhiring in recent years, and the company’s headcount still remains well above its pre-COVID hiring spree, so a chunk of this reduction is likely just standard right-sizing, but we would fade the idea that that’s the entirety of the explanation.

As another data point in the same direction, spending on US data center construction officially surpassed spending on new office construction after clearly trending in that direction for several years.

Meanwhile, US Senator Brian Schatz introduced two new AI bills that would tax AI revenues to fund retraining programs and, perhaps more significantly, invoke an automatic “whole government response” if unemployment climbs above 5.5% for two quarters. It’s still not necessarily our base case, but we’d argue kneejerk UBI in response to rapid AI advancements is definitively still not priced in (to anything).

Interestingly, despite the market increasingly reckoning with the potential for massive disruptions from these themes, AI lynchpin Nvidia sold off hard despite very strong earnings this week.

All the consternation pushed the US 10-year yield down below 4% for the first time since October (though we’ll see how that move holds up Monday morning if Iran successfully closes the Strait of Hormuz) while handing bank stocks their worst session since Liberation Day on growing concerns over the health of private credit in an AI-disrupted world.

All the upheaval was the last thing the illiquid side of the market needed, as Bain said this week that the ongoing private equity dealmaking dry spell is now worse than the trough of 2008.

Despite the tremors, Chicago Fed President Austan Goolsbee suggested the central bank should keep rates on hold for now as inflation remains too far above target. Goolsbee’s case got another data point in its favor late in the week, as January’s Producer Price Index reading came in substantially above expectations at +0.8% M/M.

For what it’s worth, though, Bessent / Warsh mentor Stan Druckenmiller said in an interview this week that he expects the Fed is still likely to cut rates, alongside a call for disinflationary growth. The Soros protégé also suggested he remains bearish on the dollar as trade imbalances correct.

Overseas, recently elected Japanese Prime Minister (and former Abenomics acolyte) Sanae Takaichi has reportedly started taking a “tougher stance” with the Bank of Japan in an effort to discourage further rate hikes.

Elsewhere in Japanese financial plumbing, new reports this week indicated that January’s well-publicized Fed “rate check” on the USDJPY cross was initiated by Treasury Secretary Scott Bessent, and not at the request of the Japanese.

On the tariff front, Bessent said that Treasury’s tariff revenue projections for the year remain unchanged despite the Trump administration’s Supreme Court loss last week, though he admitted that the $175 billion in cumulative tariff revenue thus far will likely never hit consumer wallets given the many companies suing for refunds.

Jane Street, the quant trading giant that has proven to be everyone’s favorite boogeyman in recent months, was hit with an insider trading lawsuit this week regarding the company’s alleged involvement in 2022’s massive Terra / Luna unwind.

Denizens of various Fintwit subcultures celebrated the news as a sign that their preferred bags can now rise uninhibited by supposed manipulations like the “10am slam.” We’ll just say we have our doubts.

Saturday’s Iran headlines predictably tanked bitcoin’s price, though as of this writing the orange coin has recovered to $65,000 following a week that saw over $1 billion in ETF inflows. Despite the drawdown since last fall, sentiment in the gutter, and ongoing global uncertainty, cumulative net flows into bitcoin ETFs have declined only ~12% from their October all-time highs.

As bitcoin ranges between $60-70,000, more than half of bitcoin supply is now being held at a loss, a common condition for finding a bottom during prior bear markets. Meanwhile, essentially every on-chain mean reversion model now points to the same conclusion.

Morgan Stanley filed for a de novo national bank charter geared toward providing direct custody of bitcoin and other digital assets for clients, the latest headline out of traditional finance that looks nothing like what we were seeing the last time bitcoin took a 50% drawdown.

Regulatory Update

Missouri advanced its latest bitcoin reserve bill, while Indiana passed a bill to allow public retirement plans to add exposure to bitcoin ETFs.

Noteworthy

Pseudonymous bitcoin and eCash developer Calle launched Numopay, a free open source POS app enabling NFC-based tap-to-pay capabilities with any bitcoin or eCash wallet.

Travel

Bitcoin Jawn, Philadelphia, March 2

OPNext, New York, April 16

Bitcoin 2026, Las Vegas, April 27-29