Going Vertical: Ten31 Timestamp 948,645

A Tale of Three Charts

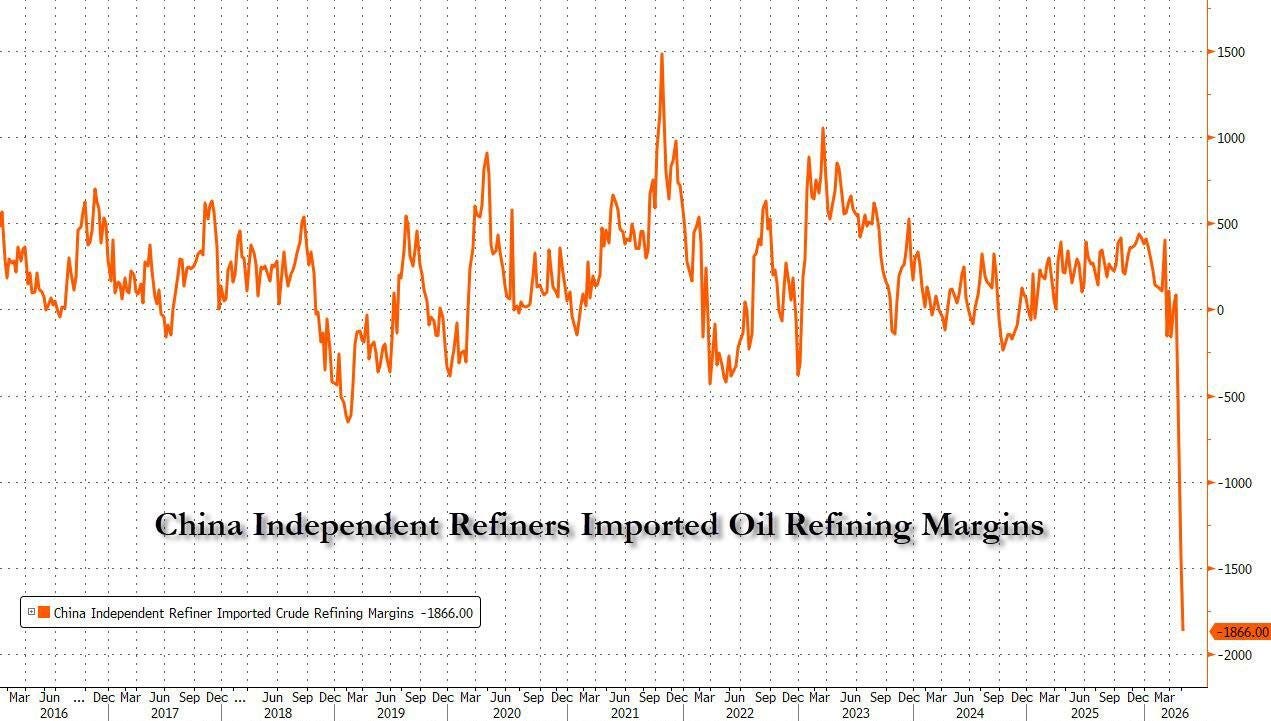

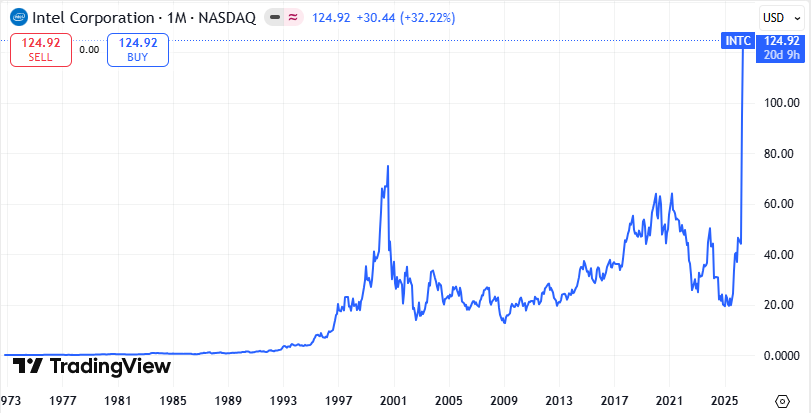

As nature abhors a vacuum, so markets abhor a vertical chart. Even in the midst of wars, famines, heavy-handed state interventions, and Presidential AI slop, demand and supply responses inexorably work to bring both euphoria and depression back to reality. The market seems to be giving us more and more vertical charts lately as global change gets more discontinuous and nonlinear, and we got two this week that highlight a key dichotomy and open question we’ve been writing about for much of the last year: can the US weaponize its remaining advantages over China quickly and durably enough to provide the necessary air cover for critical industry reshoring? For now, China appears to be on its back foot, with local independent oil refiners (the main historical Chinese buyers of Iranian crude) taking an unprecedented bath on margins as the country’s government prevents refineries from passing on huge input cost increases prompted by US-led chaos in the Persian Gulf. At the same time, the “Don’t Call It a Comeback” tour for once-ailing American semiconductor stalwart Intel – perhaps the consummate poster child for the past 30 years of American industrial own-goals – continued its shocking run, with the stock up another 25% this week (after already ripping off a 140%+ YTD move beforehand) on news of a landmark deal with Apple partially coordinated by the White House. The Intel story no doubt remains highly speculative, as the company’s topline, EPS, and free cash flow all have yet to meaningfully inflect, though the market seems to be increasingly pricing in the potential that strategically important US industry champions are now too big to fail. These eye-watering moves notwithstanding, we expect market forces to eventually drive some level of mean reversion on both of these charts: China or the US will blink, deals will be cut, capacity will expand, demand will soften or reroute, new entrants will come online. Dread it, run from it, the supply response arrives all the same.

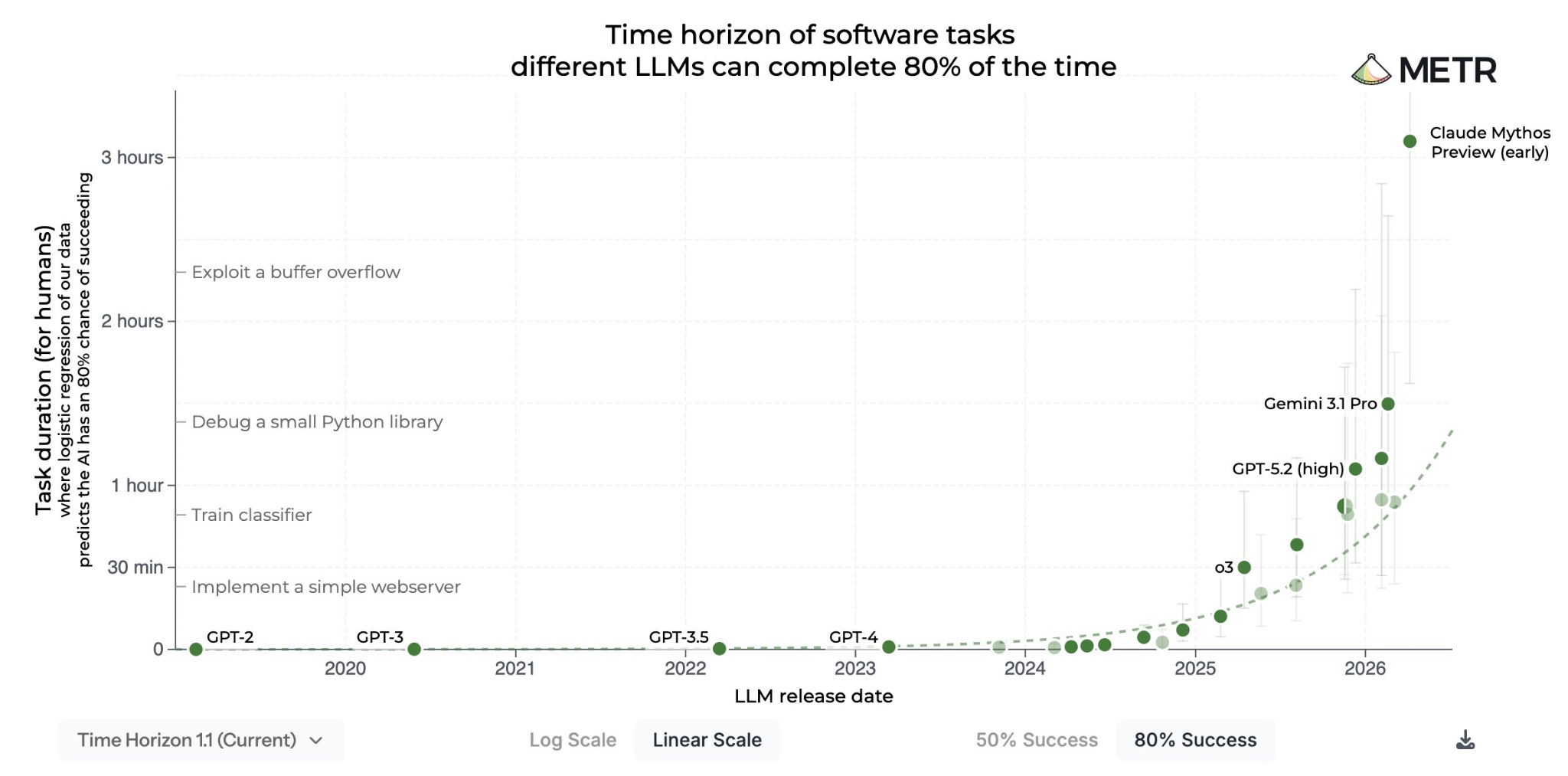

There is, of course, a third vertical chart that’s also drawing more and more mainstream attention, and which is arguably the underlying driver of the prior two. However you cut it, charts measuring AI capabilities are continuing to ramp parabolically, but unlike the other two charts, there’s no obvious market-based gating mechanism to enforce mean reversion here, other than the hard constraints of the physical reality (read: watts) needed to sustain ever-greater gains in these capabilities. But what if you’re in the middle of a Great Power Competition that pivots on who gets to own and control the curve that never mean-reverts? What if the incentives and exigencies at play have convinced decisionmakers that this is a winner-take-all game and that, because demand for intelligence is infinite, any level of investment and “creative” financing is justified? What if they’re right, and the implications for the labor market become more apparent more quickly? What if they’re wrong, and the players at the table have no way out but to paper over the resulting losses? In any of those worlds, all of which will be filled with many more vertical charts (direction TBD), what would be the value of the one asset on the planet with no possible supply response?

Selected Portfolio News

Strike continued its strong pace of new product introductions with a variety of announcements this week:

Unchained launched a new media and education campaign on bitcoin in partnership with The Atlantic:

Maple rolled out a new look, new features, and the brand new Maple Agent:

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Media

Ten31 Managing Partner Jonathan Kirkwood appeared on a panel discussing bitcoin and private credit at this year’s Bitcoin Conference.

AnchorWatch Co-Founder and CEO Rob Hamilton joined a panel on the intersection of bitcoin and insurance at the Conference.

Start9 Founder and CEO Matt Hill joined Ten31 Managing Partner Matt Odell on Citadel Dispatch to discuss Start9’s latest operating system and ambitious roadmap.

Matt also gave a talk on information sovereignty at this year’s Bitcoin Conference.

Market Updates

You already know the drill. In a series of re-runs that are quickly getting old, the week started off with attacks on the UAE and the US sinking some Iranian ships, but the US/Iran ceasefire is somehow still active.

Bond markets started to get a little queasier on the delayed progress in talks, with the US 30-year Treasury yield breaking through the 5% level for the first time in a year. Overseas debt markets saw more violent action, as the UK 30-year continued its recent run up to nearly a 30-year high.

But the classic market-managing playbook worked once again this week, as oil and yields fell on reports from Axios (why is it always Axios?) that the US and Iran are finally close to an elusive deal.

The S&P500 notched yet another record high on the news and hit its longest daily winning streak in two years, though as of Saturday morning the US is still awaiting a formal response from the Iranian side.

In the meantime, Treasury Secretary Scott Bessent said the US is successfully “suffocating” Iran’s oil industry as the country is closing in on a critical juncture for its oil storage capacity within the next several weeks.

A new “confidential CIA report” uncovered by the Washington Post this week suggested that Iran may be able to hold out much longer than that, though it’s unclear if Iranian officials themselves actually agree with that take.

In any case, Chevron’s CEO warned that oil shortages will soon start to become more prevalent (notably, beginning with Asia).

China told local independent oil refineries (who are key customers of Iranian oil) not to comply with US sanctions on Iran, an order that seems to have been met with mixed results so far.

New data out this week showed that use of the Yuan and CIPS (China’s answer to SWIFT) for sanctioned transactions jumped to a new high in March.

But at the same time, China also directed its banks to pause new loans to sanctioned refiners, while reportedly pressing Iran not to ramp up conflicts and come to a deal to resolve fighting in the Gulf.

American industrial policy saw its latest major manifestation this week in the form of a preliminary deal between Intel and Apple (partially orchestrated by the White House) for the long-underperforming American semiconductor giant to produce some chips for Apple products, which would be a very noteworthy shift given Apple’s decade-long exclusive relationship with Taiwan’s TSMC for its most advanced chips.

To be sure, it’s not totally clear which chips Intel will actually produce, when they’ll start, or what the revenue implications of the arrangement might be, but Intel shares rocketed higher regardless, making DJT Capital’s INTC position a 5-bagger since September.

Elsewhere in what has swiftly become the world’s most important industry, the US announced that Norway, home of the world’s largest sovereign wealth fund, will join Pax Silica, a consortium of 15 US-aligned countries focused on responding to Chinese dominance in critical minerals.

At the risk of stating the obvious, we don’t think we’re close to a global top on policymakers’ appreciation of the strategic importance of Intel and other lynchpins of the semiconductor supply chain, a theme that was further highlighted this week by preliminary benchmark data on Anthropic’s much-hyped Mythos model, which appear to be literally off the charts.

The Atlanta Fed’s GDPNow forecast jumped to 3.7% for Q2, while corporate profits through most of this quarter’s earnings season have continued to push higher in a fairly broad-based trend that seems to be supporting both large and small cap names.

Meanwhile, the latest jobs report came in better than expected, including a significant boost from trucking and freight, which may be the latest data point highlighting the early green shoots of reindustrialization activity.

However, this seems to be an increasingly bifurcated phenomenon, as large public tech companies like Cloudflare, Upwork, and Bill.com all announced 20%+ workforce reductions this week. All of these decisions were ostensibly driven by AI productivity gains, though as unprofitable or marginally profitable businesses with decelerating growth, we think there may be a little more going on under the hood.

Kraft Heinz’s CEO also struck a less optimistic tone in an interview this week, noting bluntly that “consumers are literally running out of money.” The CEO of McDonald’s was similarly pessimistic on the lower-income consumer on the company’s latest earnings call (admittedly, there may be some idiosyncratic GLP1 selection bias baked into both of these data points).

Coinbase had its own terrible, horrible, no good, very bad week, as it kicked things off by announcing layoffs affecting 14% of its workforce. The move was partially enabled by AI tools which have, per CEO Brian Armstrong, allowed non-technical people to begin pushing production code, which…uh, yeah.

The company then went on to post worse than expected Q1 results that marked its second consecutive quarter in the red.

Following last week’s Supreme Court redistricting ruling that gave Republicans a potential major win heading into midterms, Virginia’s Supreme Court stuck down a proposed electoral map for the state that could open up another opportunity for Republicans this fall. We’re not taking a view on either party, but these updates are worth watching as they could pave the way to what is currently a fairly counter-consensus view on the outcome for November.

Bitcoin couldn’t quite keep up with stocks this week, but it did maintain its recent directional strength and touched $83,000 before retracing a bit. Notably, Brown University’s latest 13F filing showed that the prestigious endowment held pat on its bitcoin position despite all of the first quarter’s volatility.

Strategy Executive Chairman and Bitcoin Slop Connoisseur Michael Saylor ruffled many feathers this week when he suggested the company will consider selling some bitcoin to pay dividends on its preferred stack, ostensibly just to “inoculate” the market to such a move.

CME Group plans to launch regulated bitcoin volatility futures starting next month, the same day it begins offering 24/7 digital asset derivatives trading.

Regulatory Update

The long-delayed CLARITY Act got yet another new compromise revision that seems to appease most sides at the table. Congress is scheduled to vote on the new version next week.

White House digital assets adviser Patrick Witt suggested an update on the Strategic Bitcoin Reserve will be released in the next few weeks.

Noteworthy

A researcher at Paradigm proposed a new quantum “escape hatch” protocol that could give holders of quantum-vulnerable coins a potential path to reclaiming compromised funds in the future without a soft fork today (though a fork would eventually be required).

AI is the curve that doesn't mean-revert - that's the part founders should sit with. we read 600+ VC newsletters daily so you can read the same room

AI is the curve that doesn't mean-revert - that's the part founders should sit with. we read 600+ VC newsletters daily so you can read the same room