Have Your Agent Call My Agent: Ten31 Timestamp 936,562

@KevinWarshBot, prevent social collapse, make no mistakes

After realizing en masse this week that there might actually be something to this whole AI thing after all, Portfolio Managers worldwide proceeded to trigger rolling selloffs across industries ranging from commercial real estate and trucking to ratings agencies and insurance. The carnage was no doubt driven by a lot of kneejerk shooting – perhaps best exemplified by a karaoke company driving a 20% single-day drawdown in freight forwarding stocks – and we’d guess the questions saved for later will reveal a good deal of institutional inertia and implementation frictions that will insulate legacy models for longer than some of the most galaxy-brained AI maxis may imagine (everyone would probably benefit from brushing up on their James Burnham). That said, based on our own firsthand experience using the increasingly impressive tools, it’s tough to say a real technological acceleration isn’t happening, and it’s reasonable to think that the current pace of change will leave the state of employment looking very different over the next five years.

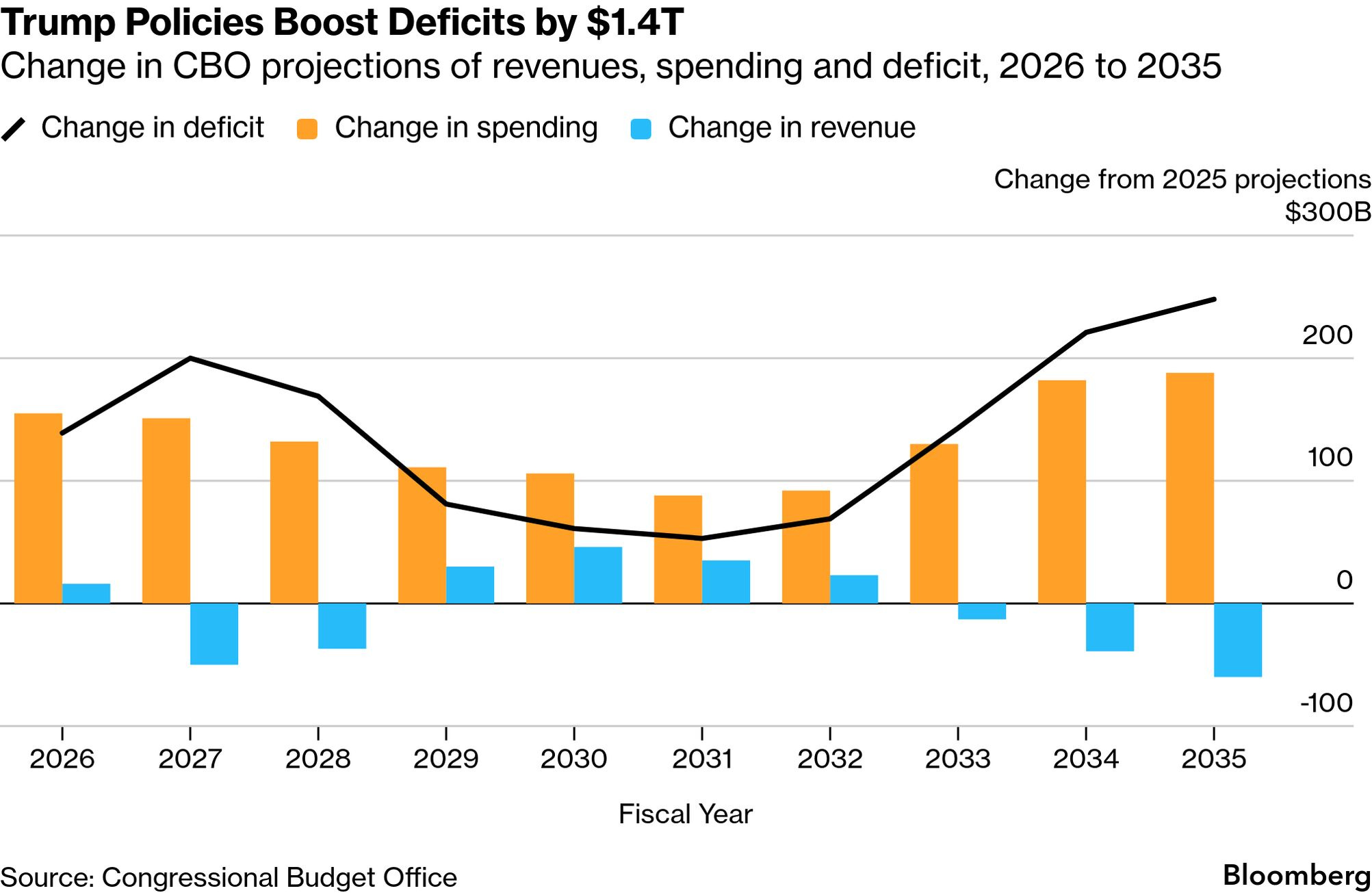

It was a poetic week, then, for the Congressional Budget Office to release its latest 10-year fiscal projections, which show an additional $1.4 trillion cumulative deficit added relative to last year’s estimates. The CBO’s forecast – which is generally biased toward underestimating deficits anyway – accounts for recent changes like the Big Beautiful Bill, but does not incorporate any of the projected AI disruption impacts that drove investors to dump stocks all week, highlighting just how tenuous the setup is for the Treasury and Fed. To be sure, a proliferation of extremely useful AI tools could give a big lift to gross productivity (and therefore nominal GDP, and therefore tax receipts), but if that turns out to be a jobless productivity boom, how much of that flow of receipts will be eaten up by automatic stabilizers and unemployment benefits? How many new federal programs like broad re-skilling will need to be authorized to manage that transition? How might that interact with a massive (and probably still underestimated) surge in defense spending and an industrial re-shoring agenda that offsets the decades-long subsidy of just-in-time international supply chains? Amid upcoming regime change at the Fed and all the recent talk of SOMA balance sheet reductions, we expect all these questions to be top of mind in Washington’s backrooms over the coming year, perhaps explaining why Treasury Secretary Scott Bessent thought it prudent to suggest this week that the Fed won’t be reducing its balance sheet for “at least a year” as it weighs all the moving pieces.

Selected Portfolio News

Giga Energy brought its latest HPC site online:

Strike updated its loan liquidation policies to give users more flexibility during periods of volatility:

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Media

Ten31 Managing Partner Matt Odell was featured on the Cyphertank show.

Market Updates

The US federal budget deficit came in at $696 billion for the first four months of this fiscal year, down Y/Y thanks largely to higher tariff revenues, but still on pace for $2.1 trillion in the full year.

The Congressional Budget Office also released its latest fiscal projections for the next decade, which show a $1.4 trillion cumulative increase over the period relative to last year’s forecast. The CBO now expects “large, historically unusual” deficits of 6-7% of GDP for the next 10 years.

President Trump tried to assuage concerns over the ballooning deficit this week by suggesting that we could simply not have a deficit anymore if new Fed Chair Kevin Warsh were to aggressively lower rates (we think the long end may beg to differ here without some creativity).

The President also suggested he thinks the economy can grow 15 or 20% under new Fed leadership. With the latest Atlanta Fed GDP Now print coming in at 3.7% for Q4, Mr. Warsh may have his work cut out for him on hitting this target.

However, the latest inflation data pointed to some air cover for the Fed, as both headline and Core CPI for January were a bit below expectations and are now in the mid-2% range, even as January’s topline jobs data also came in well above consensus (just don’t look at the latest downward revision to last year’s numbers, the largest such revision since 2009).

Policymakers will also need to contend with growing issues like student loan delinquencies, which have continued to rip vertically to new all-time highs, and a sluggish housing market, where existing home sales fell by over 8% in December as part of what the National Association of Realtors labels a “new housing crisis” (in other news, the National Barbers’ Guild reported a historic national deficiency of haircuts last month).

Elsewhere, new headwinds to the budget may emerge via AI’s indirect impacts on capital gains tax receipts, as a variety of non-software sectors like commercial real estate endured violent selloffs driven by investors attempting to price the potential for broad, near-term AI disruption.

Meanwhile, UBS said it foresees increasing vulnerability in the $3.5 trillion private credit market – much of which is tied to traditional software companies – from the accelerating pace of AI improvement, with analysts forecasting up to $120 billion of defaults this year and potential for less likely but much more violent tail risks.

Amid all these crosswinds, Bloomberg notably ran a feature on Kevin Warsh’s desire for a new Fed-Treasury accord – something we’ve been flagging in this newsletter for close to a year – though it remains unclear exactly what this means in Warsh’s mind.

As a potential hint, Treasury Secretary Scott Bessent mentioned this week that – despite frequent discussion of shrinking the Fed balance sheet in the near term – the central bank is unlikely to make any such changes for “at least a year.”

Under the hood, it was also a busy week for the international chess board defining the administration’s policy options. Most notably, pro-Trump Japanese Prime Minister (and former Abenomics acolyte) Sanae Takaichi won a landslide victory after calling a snap election, while her party took a supermajority in the country’s legislature.

The US, Japan, and Europe also announced the initiation of a critical minerals pact whereby key allies will cooperate with the US to mine, process, and stockpile materials key to national defense and artificial intelligence.

President Trump is reportedly considering withdrawing from the USMCA, the North American trade agreement that replaced NAFTA in 2020 and which is due for its first renegotiation this summer, likely another move to exert leverage over Canada and Mexico.

Congress attempted to throw sand in these gears this week with a vote to roll back Trump’s tariffs on Canada specifically, though the President will likely just veto this measure. That said, other reports suggest Trump is weighing his own rollback of some steel and aluminum tariffs because, in a shocking turn of events no one could have predicted, they are driving increased prices for consumers.

Either way, we may be close to some real and potentially market-moving clarity on this overall agenda, with the Supreme Court’s next wave of rulings, which could include a decision on the constitutionality of Trump’s tariffs, to be released in the next 1-2 weeks.

China’s regulators made headlines this week by urging domestic banks to avoid and reduce US Treasury exposure, though official data already suggest exposure has been trending down for years.

Reports elsewhere suggested that Russia is exploring the opposite path by quietly preparing proposals for a new partnership with the Trump administration that would see it move back toward the dollar nexus. Russia’s central bank quickly threw cold water on this idea, and as we all know, you should never believe something until it has been officially denied.

Bitcoin’s price generally stabilized close to $70,000 for much of the week, but Blockfills – an institutional digital assets platform backed by Susquehanna that handled $60 billion of volume last year – halted withdrawals and limited trading this week. This is the first iteration of a classic bear market headline that we’ve seen this cycle, and we would be surprised if it’s the last.

Regulatory Update

Amid ongoing conflicts between the “crypto” industry and legacy banks, Secretary Bessent again reiterated his view on the importance of passing the CLARITY Act, criticizing a group of “nihilists in the industry” that prefer “no regulation over very good regulation.”

In a move we can’t imagine will help the progress here, the American Bankers Association submitted a formal request for the OCC to pause new national bank charter grants to various crypto companies including Coinbase.

Brazilian lawmakers reintroduced legislation to initiate a national strategic bitcoin reserve. If passed, the law would allow the country to accumulate up to 1 million bitcoin over five years.

Noteworthy

BIP360, a bitcoin improvement proposal that could help pave the way for long-term quantum resistance, was officially merged into the BIPs repository, a step toward potential eventual activation.

Dr. Alex Wissner-Goss, a prominent physicist / computer scientist, futurist, and AI doomposter extraordinaire, referenced an OpenClaw agent autonomously using bitcoin’s lightning network as part of the latest entry in his widely read series on AI acceleration.

Lightning Labs launched a new L402 toolkit designed for AI agents to more easily integrate lightning payments.

Travel

OPNext, New York, Apr 16

Bitcoin 2026, Las Vegas, Apr 27-29