Just Add a Zero: Ten31 Timestamp 951,709

The running it hot will continue until debt / GDP improves

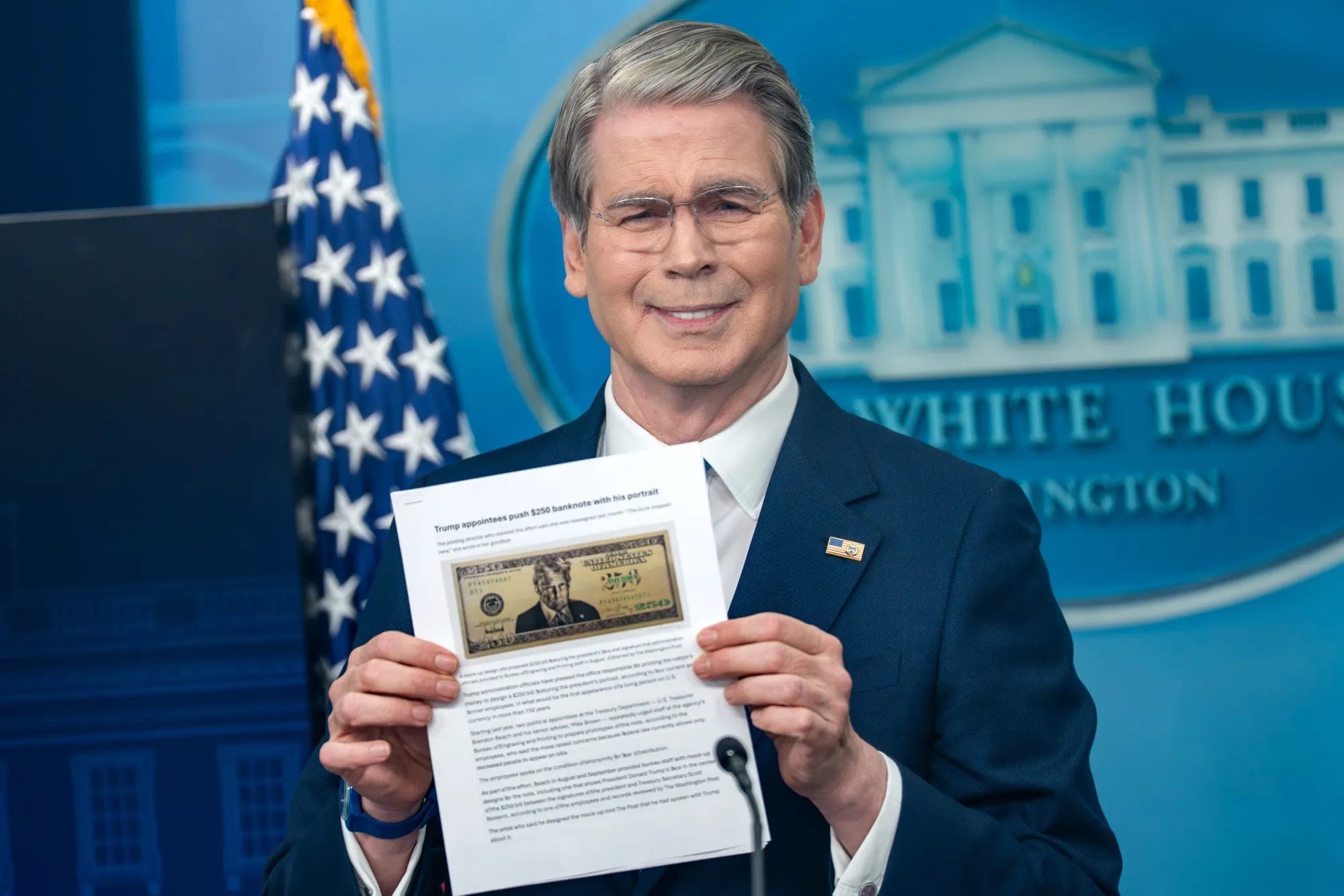

Like world-renowned prize fighter Randy Marsh, the market keeps insisting it didn’t hear no bell, as equity indices pushed to new all-time highs once again and Treasury yields backed off even as a normalization of oil prices remains elusive and various data points for the lower-end of the K-shaped economy kept looking worse. S&P earnings have continued to rip higher powered by the AI buildout, though GDP figures aren’t yet reflecting the productivity miracle that we’re assured is just over the horizon (despite some very strong leading indicator data out of trucking), and in the meantime consumer credit delinquencies have continued to spike while disposable income seems to be falling off a cliff. We’re starting to see more direct responses to the anxieties and cognitive dissonance produced by this state of affairs, including both Silicon Valley-led calls for “dividends” (the sophisticated thinking man’s rebrand of stimmies) paid to the public from the AI buildout, as well as the more blunt instrument of just taking people’s stuff championed by leftist bulwarks like Zohran Mamdani. Meanwhile, in a move that couldn’t have more poetically captured the current moment, Treasury Secretary Scott Bessent proposed that the Treasury issue a new higher-denomination $250 bill bearing President Trump’s face to commemorate America’s upcoming 250th birthday, because as all great regimes throughout history have learned, all you need to do when affordability becomes a problem is add a zero (or two) to the local bills. We are far from calling any kind of top in the AI trade; if anything, we’d bet we’re closer to the front half of the game than the back half, particularly given the national security implications and the untold financial plumbing tricks up the sleeve of the Fed / Treasury nexus. That said, all signs continue to point to an increasing fragility of the social fabric that we think only has one real response, regardless of whether it wears a MAGA hat or a $300 Che Guevara T-shirt. This administration (and the next one, whatever it may look like) needs to keep the music playing on S&P earnings growth while managing the inevitable backlash that same dynamic will incite among those who don’t own a piece of the revolution, and we continue to think that combination of imperatives has clear long-run positive implications for bitcoin.

{kind=link}

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Selected Portfolio News

Strike significantly lowered loan minimums for users in Connecticut and Oregon:

Media

AnchorWatch Co-Founder and CEO Rob Hamilton joined the ARK Invest Bitcoin Brainstorm podcast to dig into how investors should think about quantum computing’s relationship to bitcoin.

Market Updates

President Trump spent the long holiday weekend teasing a deal with Iran, while also suggesting that all Persian Gulf countries – including Iran! – will be required to sign onto the Abraham Accords that normalized relations between the UAE, Bahrain, and Israel.

Trump’s “Why Can’t We Be Friends” proposal for Iran and Israel may have slim odds, but oil generally declined throughout the week on growing optimism that a deal is close, with reports throughout the week indicating that a framework has been established and now just needs Trump’s signoff (said another way, Lucy is currently holding the football in just the right spot, and Charlie Brown will definitely kick it this time).

Iranian state media suggested mid-week that a deal is indeed in sight, and that it would allow normalized traffic through the Strait of Hormuz managed by Iran and Oman, though the White House immediately dismissed this as fake news.

Former CIA Director (and therefore completely trustworthy source) David Petraeus suggested Iran is currently “in the process of blinking” in one of the most precarious games of chicken ever played, and President Trump shrugged off concerns about midterms, noting he can outwait Iran.

ExxonMobil executive Neil Chapman suggested someone needs to blink quickly, as global oil inventories will reach dangerously low, “unheard of” levels within weeks if the status quo persists.

Indeed, new data this week suggested that China is likely aggressively pumping out its petroleum reserves stock to forestall demand destruction from higher prices. And they’re not alone, as the US executed one of the biggest SPR drains in history this week, eclipsed only by last week’s outflow.

The bond market seemed less concerned about an oil apocalypse, though, as the US 10-year and 30-year both fell well below their recent 4.5% and 5% breakout zones.

Meanwhile, the latest Core PCE inflation reading – ostensibly the Fed’s favored metric for assessing inflation – printed in line with consensus at +3.3% Y/Y.

Recently exited Fed Governor and prominent low rates enjoyer Stephen Miran published an article arguing that core PCE inflation has also effectively been overstating true experienced price changes because of recent upticks in software pricing, as well as questionable measurement practices for software inflation.

Whether you think this reads as interesting and thoughtful analysis or classic goalpost-shifting to massage numbers favorably may depend on your relative affinity for Orange Man, but in any case Fed Governors Michael Barr and Chris Waller did not seem convinced by the logic, as both publicly signaled opposition to lower rates (as well as a smaller balance sheet) this week just as new Fed Chair Kevin Warsh takes the helm at the Eccles Building.

Despite the ongoing tension in the Middle East and a potentially divided Fed, equities continued to party like it’s 1999, with memory titan Micron officially joining the trillion dollar club. The company’s market cap has now tripled since the last local bottom on March 30th. At the same time, Dell announced blowout earnings thanks to a push for on-premise enterprise AI that drove the stock up to new all-time highs, also good for a ~2.5x in two months.

S&P500 earnings in general have continued to rip through the year, with FY26 forward estimates now up 24% Y/Y, reflecting basically unprecedented earnings growth outside of post-recession snapbacks.

Of course, the boom in public market valuations and corporate earnings continues to reflect only one part of the increasingly divided K in the economy, as credit card and auto loan delinquencies have continued to push to new post-2008 highs while the personal savings rate has declined to 20 year lows and some data show ongoing declines in real disposable income.

At the same time, the latest official estimate for Q1 real GDP was revised down by 40bps to just 1.6%, driven primarily by cuts to investment spending estimates (which is exactly the wrong place for downward revisions if you’re trying to run it hot).

Things may not be getting any easier for the lower rungs of the labor and services market, as OpenAI announced that an internal model has solved a complex math problem that has stumped human thinkers for 80 years, and Anthropic announced its latest fundraise at a valuation just under $1 trillion.

Prominent tech investor Brad Gerstner suggested this week that he’s working with the White House to address some of that underlying workforce anxiety via “very tangible and profound dividends” from AI gains paid out to the public.

But Comrade Zohran Mamdani has a different proposed solution for the wealth gap: in a preview of a policy response that may be coming to a city near you, the recently elected leader of the financial capital of the world announced his administration will “transfer ownership” from certain private landlords that he believes are mismanaging their properties.

Internationally, the US has continued to place strategic bets well outside the Strait of Hormuz that may have downstream implications for energy, resource access, and leverage over China, with new reporting this week indicating that the Pentagon has continued to ramp up its Navy presence around Cuba.

The US and the Philippines have continued to work on finalizing the massive shared economic development zone announced last month, though with some controversy around the US’s request for diplomatic immunity in the region.

To the north, Canada officially entered a technical recession, which is probably not a fantastic negotiating position going into USMCA renegotiations in July.

While AI bottleneck stocks continued to trade like 2017-era ICOs, spot bitcoin ETFs have experienced 10 consecutive days of outflows, a new record that included a $1.3 billion single IBIT block trade. That said, despite the selling pressure, bitcoin has largely continued to trade sideways over the past several weeks.

Regulatory Update

Texas appointed a five member advisory committee for the state’s bitcoin reserve activities, including the CFO of Cleanspark and a former senior member of one of the largest pension funds in the state.

The CFTC approved the launch of the first onshore bitcoin perpetual contracts. These derivatives have long been a popular way for traders to express levered bets on bitcoin price movements via offshore exchanges.

The long-delayed CLARITY Act appears to have run into another major roadblock, as JP Morgan chief Jamie Dimon declared – alongside some choice words for Coinbase CEO Brian Armstrong – that the banking lobby will “fight it” aggressively from here.

Noteworthy

The week saw a variety of exciting technical updates for bitcoin, including significant progress on the use of secure enclaves to minimize trust assumptions needed for Cashu, an implementation of ecash and a promising vector for improving mass market bitcoin-denominated payment UX.

Similarly, the latest Bitcoin++ technical conference highlighted the ways that emerging protocol Ark can interoperate with the lightning network to further expand the innovation surface for bitcoin payments and onboarding.