Strait Outta Kharg: Ten31 Timestamp 940,668

Mr. President, today we are all oil analysts

If you’re anything like us, the last thing you want to read is another half-baked screed on the hourly direction of oil prices, how the US is totally cooked, or how Iran’s military has been completely annihilated. You’ll find plenty of Strait of Hormuz content below, but we think it’s helpful in weeks like this – amid the unending noise of White House claims that the war is almost won and dubious anonymous sources covertly predicting the US’s imminent downfall to corporate media – to step back to the 10,000 foot view of what might really be guiding decisionmaking at the highest level. While we fade anyone who claims to have the perfect Rosetta Stone for complex geopolitical events, we continue to think the China decoupling angle remains the most legible way to understand much of what’s really going on as the US dukes it out over 100 miles of waterway in the Middle East. There are far too many variables and reflexive relationships in the mix to make a call on how that agenda may ultimately play out, but with bond volatility back on the menu, US Treasuries failing to catch a safe haven bid, and a major source of Chinese oil increasingly threatened even as the country’s export model faces growing challenges from tariff policy, it increasingly feels like the core question for the world is who says uncle first: Western sovereign debt markets or Chinese industrial capacity? We could probably paint a case in either direction (and FinTwit is replete with attempts to do so), but we’d argue that consensus has not yet captured that either path has extremely pro-liquidity implications in the long run, as the system of mutual dependency between the East and West cannot be unwound without some form of financial repression either at home or abroad. The road ahead will be filled with potholes and detours, but we continue to believe that the events of the past 18 months point very clearly in one particular direction for neutral, globally accessible hard assets.

Selected Portfolio News

Coinkite announced the new Mk5 Coldcard, the company’s latest update to its flagship product line of the most widely trusted hardware wallets in bitcoin:

Strike increased early direct deposit limits to $10,000:

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Media

Ten31 Managing Partner Jonathan Kirkwood published a new essay on the role of bitcoin and stablecoins in the evolving global capital circuit.

Ten31 Principal John Arnold appeared on the Build with Bitcoin podcast to discuss Ten31’s strategy and current views on the bitcoin ecosystem.

Unchained collaborated with ARK Invest for a deep dive look at the potential long-term threat of quantum computing and likely mitigation strategies for bitcoin.

Market Updates

The world’s key base input to *checks notes* everything traded like an illiquid shitcoin all week, as the whiplash of oscillating headlines out of the Middle East sent oil’s price spiking to nearly $120 on Monday morning.

This move retraced after some reports on various G7 countries considering a massive drain of their strategic petroleum reserves, then even more violently reversed after President Trump suggested the war in Iran is “very complete, pretty much.”

Later in the week, the President told reporters “there’s practically nothing left to target” in the country, even as Iran seemingly continued to launch attacks on tankers in the key shipping chokepoint of the Strait of Hormuz.

Meanwhile, the country’s new supreme leader insisted the Strait must remain impassable to pressure the US while warning of an imminent 2-handle on the price of oil.

Outside the Strait itself, things continued to get even more squirrely for the oil market all week, as drone strikes compelled the UAE to close its largest oil refinery, taking close to 1 million barrels per day offline. Even more notably, the world’s largest LNG plant in Qatar has now been dormant for a full week, and Iraq totally shut down its oil ports.

On the flipside, Saudi Arabia has dramatically ramped up throughput of their pipeline to the Red Sea, potentially freeing up another net new ~6 million barrels per day.

In response to oil flows out of the Gulf grinding to a trickle and sustained pressure on prices, the International Energy Agency said its member countries will release a record 400 million barrels from global reserves “on a timeframe that is appropriate.” At the same time, the White House indicated the US will release over 170 million barrels from the US SPR, which would push the reserve to its lowest level since it was established.

President Trump also announced a massive new $300 billion oil refinery project in Texas, though this is unlikely to help matters before midterms. However, reports this week indicated the President is preparing to suspend the Jones Act, which would allow foreign tankers to bring in more supply for US refiners.

At one point in the week, Iran apparently indicated that China had reached out to discuss a ceasefire, which is kind of an interesting non-sequitur for the narrative that China holds all the geopolitical cards.

Either way, Iran later said a negotiation is off the table for now, and tanker data suggest Iran has continued to send oil to China through the Strait – though so far it looks like the total shipped is about half a day’s oil consumption in China, and in any case there’s a decent argument that this kind of selective blockade may not matter regardless.

As it relates to the real question on everyone’s mind, the US has so far refused requests to escort tankers through the embattled Strait, and there are basically two schools of thought on this fact in the mainstream press: those that think this suggests the US military is a paper tiger incapable of securing the Strait, and those that think the US may actually want the passage to remain closed for asymmetric geopolitical leverage. For what it’s worth, the President said this week that keeping the Strait open “really pertains more to China than to us.”

But Secretary of War Pete Hegseth suggested that both camps should calm down, as we “don’t need to worry about” the Strait (even as the Pentagon moves another 5,000 troops into position around the Middle East).

Perhaps one reason Hegseth is so unruffled is that, per the President, the US may just “take over” the Strait, a plan that was possibly given a little more credence on Friday evening when the US, to quote the Orange Man, “obliterated” all military installations on Kharg Island, a key structural shipping hub in the area (though some experts argue taking Kharg wouldn’t be enough to clear the logjam).

Noted Adult in the Room and Amateur Pugilist Scott Bessent said, regardless of the posturing, the US will escort vessels through the Strait as soon as militarily possible, and – despite all appearances – the administration has been planning for this reality for months.

Most notably for all the bondholders out there, Bessent said in that same interview that there is no conceivable price to this conflict that would make him see it as “unaffordable.”

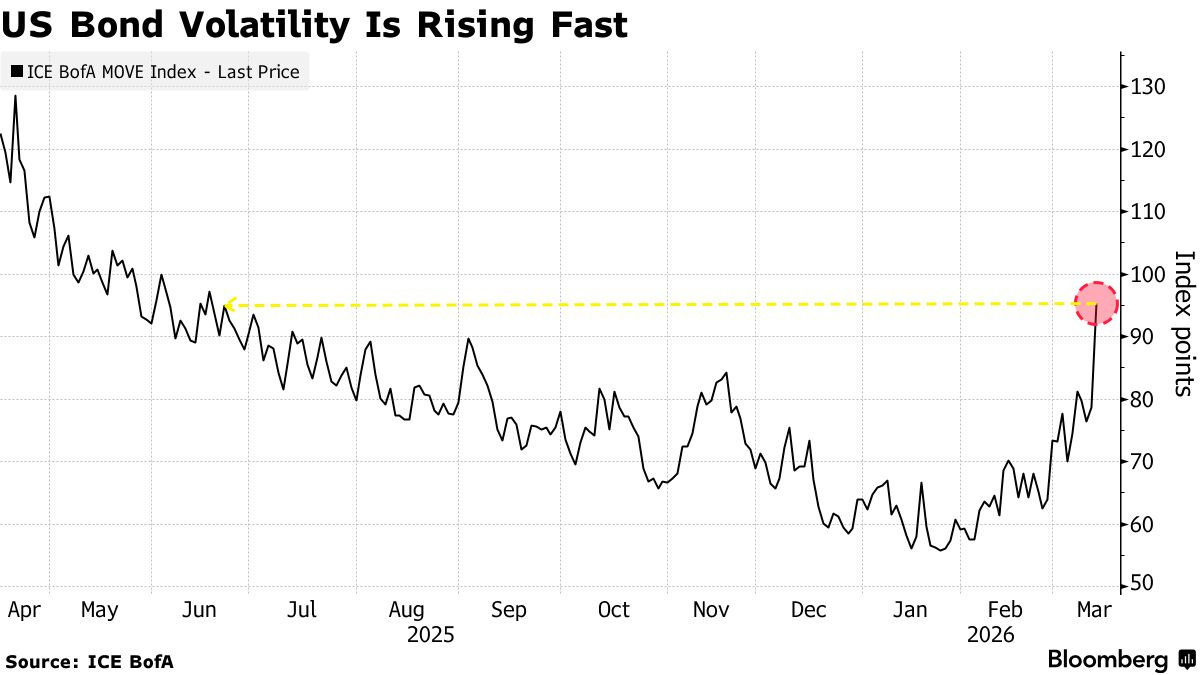

That comment brings us to the real pivot point in this whole thing, which is how well sovereign debt markets behave as the conflict drags on and keeps oil prices elevated. To that point, the US 10-year Treasury yield nearly touched 4.3% this week after taking back a 3-handle just a couple weeks ago.

This is not yet true breakout territory as it’s basically just the prior local top from early this year, but the lack of a “flight to safety” bid in the world’s “risk-free” asset continues to be notable, as does swiftly rising bond volatility, with the MOVE Index ticking back to post-Liberation Day highs.

Perhaps more notably in the near-term, European debt continues to get smoked, with both 10-year German bunds and French OATs reaching levels not seen since the Eurozone crisis of the early 2010s. In our view, global sovereign yields are among the most important KPIs to watch over the coming weeks as and if the Sparkling Kerfuffle in Iran escalates into an acknowledged war, potentially driving both material fiscal strain on over-levered sovereigns and a true “oil shock” that keeps commodity prices inflated for the medium term.

At the same time, the DXY Index broke the 100 level and moved to its highest reading since May 2025 as uncertainty and spiking rates drove a rush for dollars. The USDJPY, a key component of the DXY basket, moved back to just under 160, nearly a 40-year high and above the level that triggered January’s well-publicized US rate check.

With all eyes on the Persian Gulf, Senator Holden Bloodfeast hinted that Cuba is up next on the administration’s regime change shortlist, though other reports suggested this may take the form of an “off-ramp” deal for the Castro family rather than another Saturday morning visit from Delta Force.

Colombia may also be setting up for a cozier relationship with the Trump administration, as anti-cartel hardliner Paloma Valencia won a much larger than expected share of a key primary vote this week. Valencia has openly discussed wanting to strengthen ties with Washington.

Elsewhere, various elements of the simmering global trade war continued to escalate, as the dispute between China and semiconductor manufacturer Nexperia – which is headquartered in the Netherlands but owned by a Chinese firm and was briefly seized by the Dutch government last fall – heated up again, potentially tightening global chip markets further.

Just as notably, the latest trade data showed that Chinese exports into Europe surged both last year and for the first two months of this year, as the export-heavy economy rerouted output away from the US and to other developed markets, which may put an unwelcome strain on the already struggling European industrial base.

Domestically, the US launched Section 301 trade probes into 60 countries, laying the legal groundwork for replacement of IEEPA tariffs that were recently overturned by the Supreme Court.

The private credit complex continued to take more lumps this week, as Cliffwater and Morgan Stanley both capped withdrawals out of large funds (with $33 billion and $8 billion of AUM, respectively). The Cliffwater fund was hit particularly hard, with investors reportedly seeking to redeem 14% of fund assets.

Saba Capital launched a tender offer at a 35% discount for shares of the Blue Owl fund that made headlines by closing down withdrawals and pivoting to a return of capital model last month (though the head of Saba says he remains bullish on many of the platforms, including Blue Owl itself).

The CEO of ServiceNow, one of the largest publicly traded enterprise software companies, also didn’t do the complex any favors with comments this week that agentic AI could drive new graduate unemployment “easily into the mid-30s” over the next couple of years, potentially portending major headwinds for sectors where private funds are overweight.

On the broader macro front, the latest CPI reading printed in line with consensus at 2.4%, with Core CPI putting in its lowest level since 2021. GDP growth figures for Q4, meanwhile, were revised down from an already weak initial print to just 0.7%.

The US federal deficit topped $1 trillion for the first five months of the year, an annualized pace of well over $2 trillion (though we’ll see how tax season affects the trajectory). This five-month tally was down 12% Y/Y, but it also still has yet to lap the benefit of tariffs (which didn’t begin taking effect until last spring).

Strategy’s STRC product extended its multi-week streak of holding the $100 par level up until Friday’s ex-dividend date, when it fell slightly below par. MSTR acquired ~5,300 bitcoin with STRC proceeds in the prior week and likely more than doubled that this past week. The company has now purchased over $6 billion of bitcoin in Q1 alone vs just $176 million in all of 2022.

Regulatory Update

Amid recent banking system wins for some crypto exchanges, US banking lobbyists are reportedly weighing a lawsuit against the OCC to prevent any more such licensing.

On a related note, the Federal Reserve announced it will initiate a public comment period on Basel capital rules that would apply a massive negative risk-weighting to bitcoin.

More encouragingly, a new Treasury report to Congress explicitly acknowledged legal and legitimate uses of digital asset privacy technologies like mixers, a substantial shift in tone relative to much of the past decade.

However, the Southern District of New York also filed this week for a retrial of Tornado Cash developer Roman Storm following last year’s lawsuit that ended in a hung jury.

The National Bank of Kazakhstan announced plans to shift up to $350 million from its gold reserves to investments tied to bitcoin and other digital assets.

Noteworthy

The bitcoin network mined its 20 millionth coin this week, leaving just 1 million new bitcoin to be issued over the course of the next ~114 years.

Travel

OPNext, New York, April 16

Bitcoin 2026, Las Vegas, April 27-29