Ten31: An Investment Platform for Bitcoin Adoption

October 31st is a special day for bitcoin: the anniversary of the whitepaper’s publication. From our first blog post when we announced Ten31, we stated our singular focus: helping build the world’s future bitcoin-enabled infrastructure. We did not follow the stereotypical VC approach of naming our firm after ourselves (e.g., Andreessen Horowitz, Kleiner Perkins). Our namesake, Ten31, is a direct reference to October 31st. This choice was intentional, signifying something bigger than ourselves and an unwavering dedication to bitcoin, which we view as critical for humanity’s positive evolution.

An Investment Platform, Not a Bitcoin VC Fund

Many external parties view Ten31 as a “bitcoin VC.” While this label brings awareness to a vital, overlooked vertical, it’s a limiting and inaccurate description of Ten31. From day one, we have identified ourselves as an “investment platform,” not a VC fund. In fact, in our initial announcement we went as far as to say we were the “anti-VC fund,” positioning ourselves against traditional venture capital. We envisioned a new strategy for supporting companies building technology relevant to bitcoin. Our goal was to become an investment platform dedicated to building the ecosystem for bitcoin adoption, one that runs counter to conventional venture capital strategy and wisdom.

VC funds are typically focused on a particular stage of an emerging company’s life cycle (e.g., pre-seed/seed, Series A, etc.). This dynamic evolved under a fiat standard, driven by the ‘growth at all costs’ mindset. Over the last few decades, as the cost of money has been artificially depressed, technology companies have been incentivized to burn cash for increasingly extended periods in pursuit of growth. This prolonged cash-burn phase made it advantageous for investors to specialize in stages of this unprofitable timeframe, as one investor often couldn’t finance all the accumulated losses.

For example, pre-seed investors would specialize in companies lacking a product or business model. Seed investors would assess if a cash-burning business can deliver on its plan. Series A investors would determine if a company (perhaps with some revenue but still unprofitable) can scale. This sequence would continue, with later investors assessing public market or acquirer potential for the still-unprofitable story. Rarely in this cycle, or perhaps only at the very end, would an investor consider if the company might one day actually generate a profit. In this sequence, an investor’s value at each stage was often just as much about making introductions and convincing the next group to subsidize the money-losing story as it was about supporting the company’s actual growth. It became a game of hot potato, burning any investor holding on when the company failed to reach sustainability and couldn’t pass it on to another group.

We believe bitcoin is changing how companies are built and funded. Profit generation is sought earlier, and the need for venture capital ‘fundraising stage specialization’ is less powerful than bringing bitcoin expertise and alignment to the full spectrum of a company’s lifecycle. Ten31’s experience and network are applicable across all company stages, and bitcoin’s growing global impact creates an expanding sandbox for our thesis. While stage specialization may still have its place due to scarce fund resources or specific risk/return mandates, we believe bitcoin adoption is so early that the opportunities to extend the thesis into other categories and markets are far greater. Driving asymmetric returns and an outsized impact on adoption requires widening the aperture, and that’s the approach we have taken at Ten31.

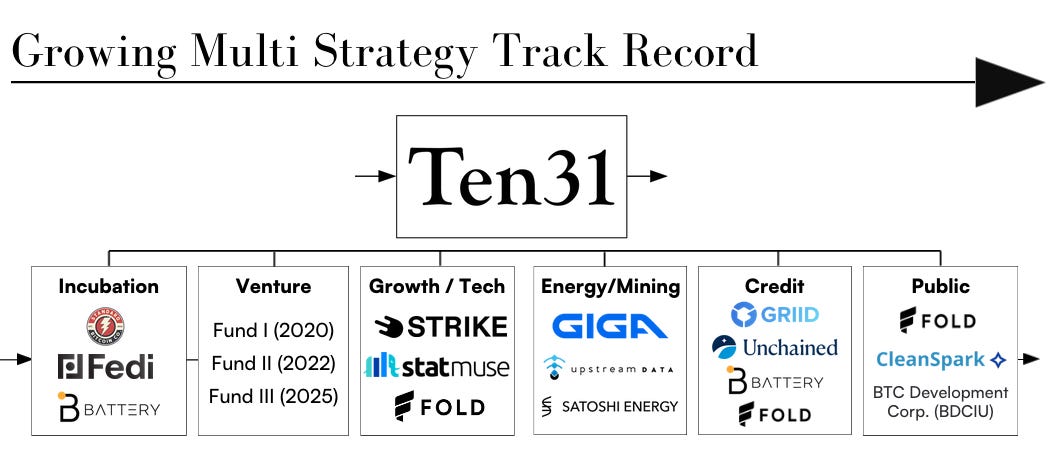

Ten31 has been partnering with companies building important technology and applications to enable bitcoin adoption for more than five years. Over that time, we have invested over $200 million into the ecosystem across several types of investment vehicles, including traditional closed-end private equity-oriented funds disclosed on our website (the “Low Time Preference Funds”), as well as undisclosed vehicles for alternative strategies (e.g. credit) and bespoke vehicles for specific opportunities, which we often pursue privately with our existing limited partners.

The graphic below depicts the breadth of our involvement and the flexibility in our approach to date. While we typically lead any investment we make and usually pursue opportunities on an exclusive basis, the nature and structure of our partnerships have been incredibly diverse. We have done everything from being the first check in a pre-seed opportunity or helping incubate a new idea, to leading later stage and growth equity rounds, to structuring credit investments and also participating in various ways in public markets transactions.

The companies we back are also diverse. Some fit the traditional early stage bitcoin technology profile, while others do not look anything like a traditional venture capital backed business, such as hardware (Coinkite) or capital-intensive energy infrastructure (e.g., Giga, Upstream Data). Furthermore, Ten31 has solely funded numerous companies that achieved profitability and became self-sustaining without relying on any future capital injections, a benefit of this new approach to growth. Additionally, while most of our partners began with a bitcoin focus, some partnered with us to incorporate bitcoin into their existing business (like StatMuse, a leading search and knowledge platform that now offers a leading bitcoin search capability). We are also actively exploring this theme in the public markets, as seen with our recently announced SPAC transaction (BDCIU), further extending our prior public markets activity from Griid and Fold.

An Ecosystem Approach to Investing

Ten31’s scope is much larger than traditional VC. We take a holistic “ecosystem approach,” with opportunities relevant for multiple strategies (equity/debt, private/public, various durations). In building Ten31 we have taken inspiration from the early days of Sequoia to influence our strategy.

Sequoia is one of the pioneers of the modern technology investment era, funding some of the storied technology companies of our time which now represent trillions in market capitalization, from Atari to Apple, to Oracle and Cisco, to Google to Instagram to Airbnb and Stripe, and beyond.

Many view Sequoia as a quintessential VC fund, but a more accurate framework, especially given their early evolution and contribution to the modern technology world, is that Sequoia is an investment platform. Sequoia founder Don Valentine came from the semiconductor industry, and the central idea behind their thesis was the coming proliferation of microprocessors. Sequoia brought a deep technical literacy to their approach. They were early to this idea and pursued this worldview aggressively.

There is a parallel to Ten31’s founding thesis. In our first published post, we specifically called out that bitcoin will be the future world reserve asset, and we have been pursuing opportunities aggressively to further express this thesis ever since. It is only over the last 12-24 months that this thesis started to become more accepted as a possibility in institutional circles, though it is still a non-consensus view and undoubtedly still early.

Sequoia became an investment platform in its early years by investing in the companies which would shepherd in the future behind their microprocessor thesis, and also supporting the interdependent layers which would be beneficiaries of this secular trend. First it was interactive electronics (Atari), and soon after personal computing (Apple). With the rise of personal computing and proliferation of data, the second order beneficiaries were data management (Oracle) and networking (Cisco). They continued to invest in the enabling companies around the PC and peripherals, including disk drives, printers, and components companies. Sequoia pioneered the ecosystem approach, which has been referred to as an “aircraft carrier” strategy (investing in the ship and everything in its orbit). Sequoia knew these categories were interconnected and would multiply each other’s value, meaning the value of individual investments would be much greater when combined in a complementary, synergistic portfolio.

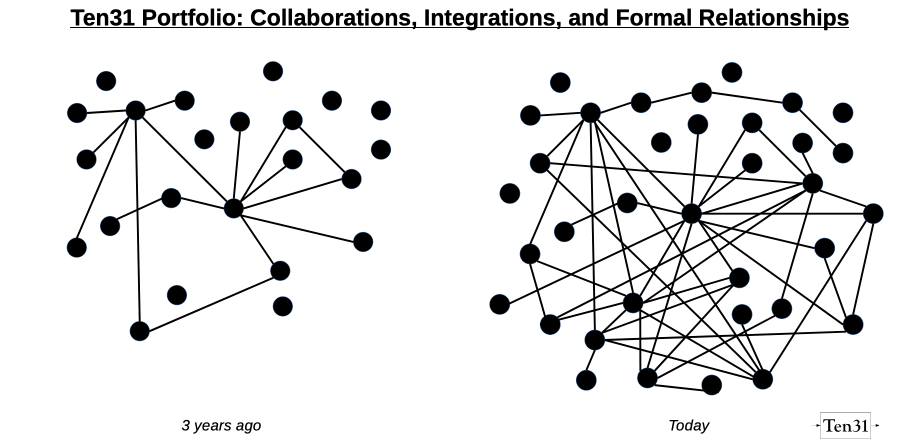

Ten31’s ecosystem approach is similar. We have invested in the essential, interconnected layers of the bitcoin ecosystem, the areas we believe are the building blocks to a new financial and economic system with bitcoin as the foundational reserve asset. This includes bitcoin exchange/brokerage, custody, lending, node infrastructure, energy and mining infrastructure, applications, and security, among other categories. Similar to Sequoia’s early investments, the nature of the companies we back span traditional technology and software, as well as hardware and other categories that do not fit the traditional VC profile. And just as Sequoia’s portfolio added value to the rest of its investments, the companies in our portfolio are interconnected by bitcoin’s open, interoperable network, enabling multiplicative benefits which have increased over time. This remains a dynamic which is not well understood or appreciated, and difficult to replicate by others without the scale of capital and breadth and depth of industry involvement Ten31 has brought to the market.

Sats Flow Investment Framework

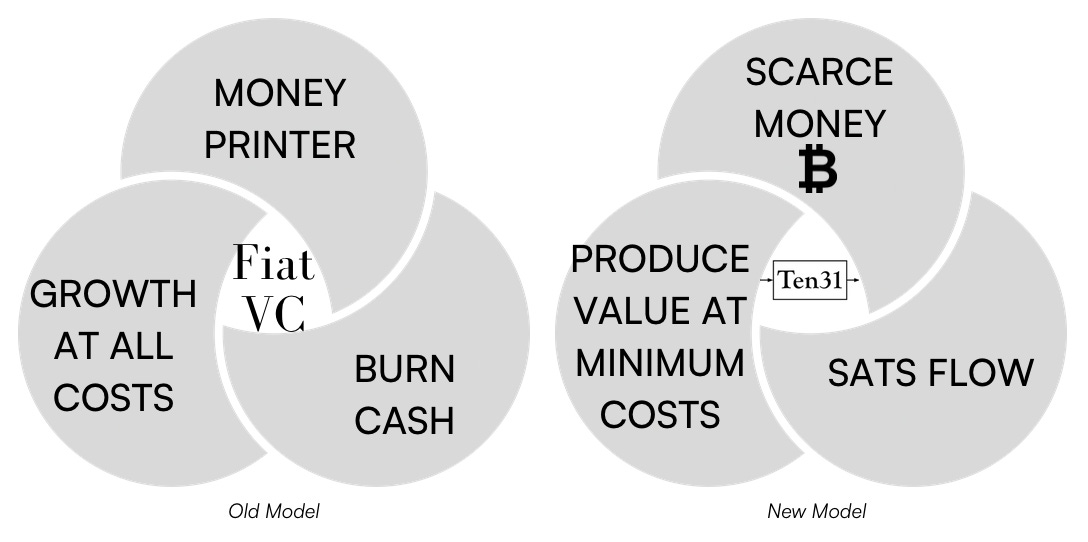

The single biggest contrast between Ten31’s approach and traditional venture capital is our focus on investing in sustainable business models we believe can generate “sats flow,” or the accumulation of profits which over time will increasingly be denominated in bitcoin. Traditional Silicon Valley VC has become synonymous with growth at all costs, burning cash, and relying on a money printer world. As the world shifts to bitcoin as a fundamental barometer of value and the future world reserve asset, we understand the days of easy money are over. With it, all economic actors will increasingly gravitate towards a focus on generating (bitcoin) profits in a sustainable way (sats flows), by providing a product or service to the market at a higher price than its costs to deliver. While this won’t eliminate money-losing endeavors, it will increase the urgency to reach a sustainable model, as external subsidies can no longer be relied upon in perpetuity.

This is the underlying philosophy for our investment selection. Every meaningful investment we make must have a strong prospect of generating profits and sats flows in the near term. This is a high bar because bitcoin itself is the opportunity cost. We have to believe an investment can outperform bitcoin, otherwise we would be better off just holding bitcoin instead. At its most basic level, there are only three ways to outperform bitcoin: financial leverage (add risk), multiple arbitrage (buy low / sell high, difficult to underwrite), and sats flow (our focus).

Based on the above, as compared to a traditional VC approach, our approach looks a lot more like a private equity style of investing (which is no coincidence, since that is my professional background for the prior 15 years before co-founding Ten31).

Over 50% of the capital we have deployed is invested in companies expected to be profitable in the next twelve months, and some of the companies we back already provide bitcoin denominated dividends, another core part of our thesis for investment monetization as we move to a bitcoin standard. We have been saying for years bitcoin technology companies could be viewed as synthetic bitcoin miners, with the prospect of producing an ongoing stream of bitcoin income but often with much less capital intensity and competitive pressure as bitcoin miners.

Conclusion

Sequoia didn’t identify as being in the venture capital business. They were investing early across the entirety of a technology ecosystem based on a set of principles that diverged sharply from the prevailing wisdom of the time. Sequoia was in the company building business, and to this day their website says “We help the daring build legendary companies.”

We view Ten31’s opportunity similarly. We are not in the venture capital business, we are in the bitcoin adoption business. We are an investment platform, singularly focused on bitcoin, with many ways we believe we can help drive further bitcoin adoption and asymmetric investment performance. We partner with enduring, industry-defining companies that are helping us achieve those goals. We deliberately go against the grain, break the mold of traditional venture capital, and carve our own path.

I explained our ambitions in a presentation during SXSW last year, saying “just as Sequoia made their name early on by supporting a wave of technology adoption and backing many of the companies which became the technology leaders of today, we think there’s a similar opportunity for Ten31 to back and support this new wave of bitcoin adoption, and back many of the bitcoin companies which will become the technology leaders of tomorrow.” We believe the size of the opportunity and the potential impact on the world is comparable to what we’ve seen Sequoia accomplish, and we will be humbled if we can even have a fraction of the impact they’ve had on the world. We certainly believe bitcoin will, and for that it’s worth the effort.