Ten31 Timestamp 866,352

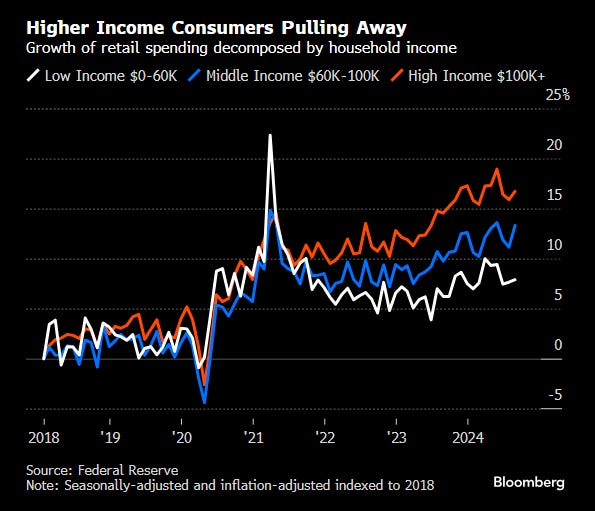

Bitcoin pushed back to $69,000 for the first time in several months to close out a strong week that saw over $2 billion in net ETF flows. As has been the case for much of this year, equity indices also notched another strong week, as already lofty investor sentiment was further buoyed by better than expected retail sales data (though as always the data looked far less rosy when adjusted for inflation), even as earnings growth for a broad swath of index components continues to look fairly stagnant. With mortgage demand declining sharply in recent weeks and US housing inventory ticking back to pre-COVID levels, it’s unclear how long the recent run can continue, but key sources of global liquidity – including inflecting US budget deficits, more rounds of aggressive stimulus in China, and globally cresting benchmark interest rates – seem likely to apply at least some degree of upward pressure to asset prices for some time to come (aggravating real-world consequences like the dynamic depicted in the chart above).

Portfolio Company Spotlight

Battery Finance is a credit opportunities asset management firm capitalizing on the many ways that bitcoin will impact traditional finance. Battery offers project finance vehicles with unique dual collateralization in the form of both underlying physical assets and bitcoin, as well as several additional strategies. All of the firm’s products aim to blend exposure to bitcoin’s upside with reduced medium-term volatility via project cash flows and the collateralization of traditional assets.

Selected Portfolio News

Vida announced integration of OpenAI’s speech-to-speech API as part of its voice platform:

Zaprite rolled out several new features this week, including flows for cash payments, integration with Authorize.net, and new sandbox environments for developers:

Debifi launched the a new version of its app, featuring several updates including integration with the Coldcard Mk4:

Strike launched a new referral program:

Media

Battery Finance Founder and CEO Andrew Hohns published an op-ed piece in Institutional Investor on the crucial role bitcoin allocations can play for pension funds.

Ten31 Managing Partner Marty Bent was quoted in a dubious new research paper on bitcoin by the European Central Bank. A brief summary of the paper’s conclusions can be found here.

Parker Lewis, Ten31 Advisor and Zaprite Head of Business Development, published a piece examining bitcoin’s value as a function of its enablement of exchange over time.

Zaprite Founder John Magill appeared on the Talking in Bits podcast to discuss Zaprite’s approach to merchant adoption of bitcoin payments.

Market Updates

In a headline so frequent that it’s barely worth a mention, equity indices continued to make new highs this week, with both the Dow and S&P500 marking their longest winning streaks of the year.

Sentiment was buoyed by better than expected retail sales and initial jobless claims data (even though this month’s retail figure was both negative on an inflation-adjusted basis and well below the long-term average).

Meanwhile, the share of the Rusell 2000 with negative LTM earnings is now back above 2008 levels and near the high set during spring 2020. Meanwhile, Street estimates point to another quarter of no earnings growth for the non-Magnificent 7 constituents of the S&P500.

Despite the Fed’s long anticipated first Fed Funds rate cut in four years and a recent decline of more than 100bps from peak on 30-year fixed mortgage rates, US mortgage applications declined 17% last week (following a 5% decline last week), good for the sharpest weekly decline since April 2020.

The latest monthly statement from the Treasury Department – released a week late without explanation – confirmed CBO estimates from earlier this month that the US tallied another $1.8 trillion deficit in fiscal 2024. The figure equates to 6.3% of GDP (up from 5.6% last quarter), a level increasingly disconnected from historical peacetime norms.

The IMF said the quiet part out loud this week with a new, aptly-timed report admitting that global public debt is “probably worse than it looks” (a discouraging sentiment given that it, in fact, looks pretty bad).

Overseas, the European Central Bank cut its benchmark rate by another 25bps and signaled more cuts to come as growth continues to stall. The move marks the first time in 13 years that the ECB has cut rates at consecutive meetings.

Elsewhere, Chinese GDP for Q3 came in a bit above expectations at +4.6%, though not high enough to alleviate concerns of missing the government’s 5% annual growth target. In response, the PBOC announced another $110bn+ stimulus program, including more direct support for the country’s equity markets.

Notably, the Chinese government has also quietly enacted new measures to more effectively tax overseas investment gains by the country’s wealthiest inhabitants, a potential headwind to various Western asset classes (including equity markets and metropolitan real estate) that have become a popular store of value for many ultra-rich foreign investors.

Recently converted bitcoin acolyte Larry Fink made more positive comments about bitcoin on BlackRock’s Q3 earnings call this week, noting he expects the asset to continue to grow regardless of November’s election outcome.

Larry had good reason to be bullish this week, as net spot bitcoin ETF flows cleared $2 billion on the week and total cumulative flows eclipsed the $20 billion mark for the year, extending the vehicles’ unprecedented run since inception.

Despite these strong flows and bitcoin pushing back to $69,000 on Friday, search volume for bitcoin remains at a one-year low, suggesting broad retail euphoria has yet to set in.

Regulatory Update

After clearing options for BlackRock’s IBIT ETF several weeks ago, the SEC approved options trading on the NYSE and Cboe for all spot bitcoin ETFs on Friday.

Republican Presidential candidate Donald Trump has proposed several new plans to levy tariffs as high as 100% on goods from countries moving away from the US Dollar as their reserve currency. While we sympathize with the underlying motivation, we encourage the Trump campaign to read their Rothbard and study Triffin’s Dilemma.

Italy announced a plan to raise capital gains taxes on bitcoin from 26% to 42%.

Norway enshrined into law the right to pay merchants with physical cash, a welcome move in an era that’s increasingly hostile to cash transactions.

Noteworthy

Coinbase announced it will end its direct deposit capabilities, a highly popular feature that is still live at Strike and Fold.

The trustee overseeing bankruptcy proceedings for long-defunct exchange Mt. Gox postponed the repayment deadline for creditors by one year to Oct 31, 2025.

Travel

Unchained / Bitwise Dinner in Nashville, Oct 23

Lugano Plan ₿ Forum, Oct 25-26

Nashville BitDevs and Nostrville, Nov 5-6

Austin BitDevs, Nov 21

BitcoinMENA, Dec 9-10