Ten31 Timestamp 875,738

It was a messy week for markets, with the Santa Rally reversing violently on the back of updated commentary out of the Federal Reserve. The single node that validates the world’s dollar transactions cut the benchmark Fed Funds Rate by 25bps as was broadly anticipated, but the central bank’s closely watched “dot plot” projecting the future path of rates pointed to fewer cuts than expected for next year, as well as a higher inflation outlook, pushing down the S&P500 as much as 5% on the week while driving the second largest VIX spike in history. The 10-year US Treasury yield and the DXY also ripped higher, putting pressure on all assets including bitcoin. After making a new all-time high of ~$108,000 to kick off the week, bitcoin fell precipitously before closing out the week around $98,000 (still among the highest weekly closes in the asset’s history). Markets were also roiled by the semi-annual re-run of government shutdown theater, a process that got a little added spice this time around when President-elect Donald Trump suggested that Congress should simply do away with the debt ceiling altogether, a refreshing acknowledgment that when it comes to US borrowing – as with bitcoin’s price – there is no top.

Portfolio Company Spotlight

Debifi is a non-custodial lending platform providing institutional-grade liquidity for P2P loans backed by bitcoin, the world’s best collateral. The company, founded by Hodl Hodl CEO Max Keidun, offers robust, secure multisig vaults that ensure bitcoin collateral cannot be rehypothecated, solving one of the key problems plaguing most “DeFi” projects. Debifi extends the proven security of Hodl Hodl’s lending model to the institutional sphere and has an exciting roadmap ahead.

As the world’s largest investor focused entirely on bitcoin, Ten31 has deployed nearly $150 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem, and we expect 2025 to be the best year yet for both bitcoin and our portfolio. Ten31 will hold a first close for its third fund at the end of this year, and investors in that close will benefit from attractive incentives and a strong initial portfolio. Visit ten31.vc/funds to learn more and get in touch to discuss participating.

Selected Portfolio News

Strike added USDT on/off ramps for eight more countries:

Debifi now offers support for Coinkite’s Coldcard Q:

Media

The Ten31 team hosted a new episode of Bitcoin Alpha featuring a discussion on quantum computing’s impact on bitcoin with longtime bitcoin developer Matt Corallo.

Managing Partner Matt Odell appeared on the Money Matters podcast with Strike CEO Jack Mallers.

Primal Founder and CEO Miljan Braticevic joined the Stephan Livera podcast to dig into the recent Primal 2.0 release and the future of Nostr.

Miljan also published a blog post detailing the capabilities of the newly launched Primal Premium offering.

Ten31 Advisor and CleanSpark CSO Harry Sudock appeared on the What Bitcoin Did podcast to discuss a potential strategic bitcoin reserve and the current mining landscape.

Strike was featured in an article about a USC football recruit taking a portion of his NIL payments in bitcoin.

Market Updates

The Federal Reserve threw the market a curveball this week, cutting its benchmark interest rate by 25bps – in line with consensus – but posting a more hawkish dot plot that indicated only two cuts next year. Fed Chairman Jerome Powell also suggested the central bank will be “cautious” on the pace of cuts from here.

Along with the less accommodating forward commentary, the Fed also raised its forecast for Core PCE (its preferred inflation gauge) from 2.2% to 2.5% for 2025, sparking more consternation about the path of inflation next year.

The Fed updates sent markets reeling, as the 10-year US Treasury yield spiked back above 4.5%, once again approaching multi-year highs. The DYX dollar strength index also rose to YTD highs and is now back to levels not seen since late 2022.

All of these dynamics pressured the rest of the asset complex, with the S&P500 down as much as 5% at one point and the VIX (a popular volatility gauge) posting the second-largest single day move in its history.

However, markets got some breathing room on Friday as the latest PCE update actually came in lighter than expected at +2.4% Y/Y (with core PCE +2.8% Y/Y).

Outside of the Fed-induced volatility, investors also had to reckon with yet another iteration of government shutdown WWE, as incoming President Donald Trump scuttled a proposed spending bill and left Congress scrambling to establish short-term funding for the next few months.

The saga ended the same as always with Congress passing a bill in the eleventh hour to keep the lights on; however, the legislation only extends through mid-March, at which point we look forward to copying and pasting these same headlines once again.

The currently-suspended debt ceiling is set to come into effect again starting on January 1, prompting President-elect Trump to call for abolishing the debt ceiling altogether since it “doesn’t mean anything, except psychologically,” the latest instance of an increasingly frequent pattern of government officials saying the quiet part out loud.

Bitcoin was not immune to the broad market selling pressure and fell as low as $93,000, but only after it opened the week by making a new all-time high of $108,000, which included a new all-time high in gold terms.

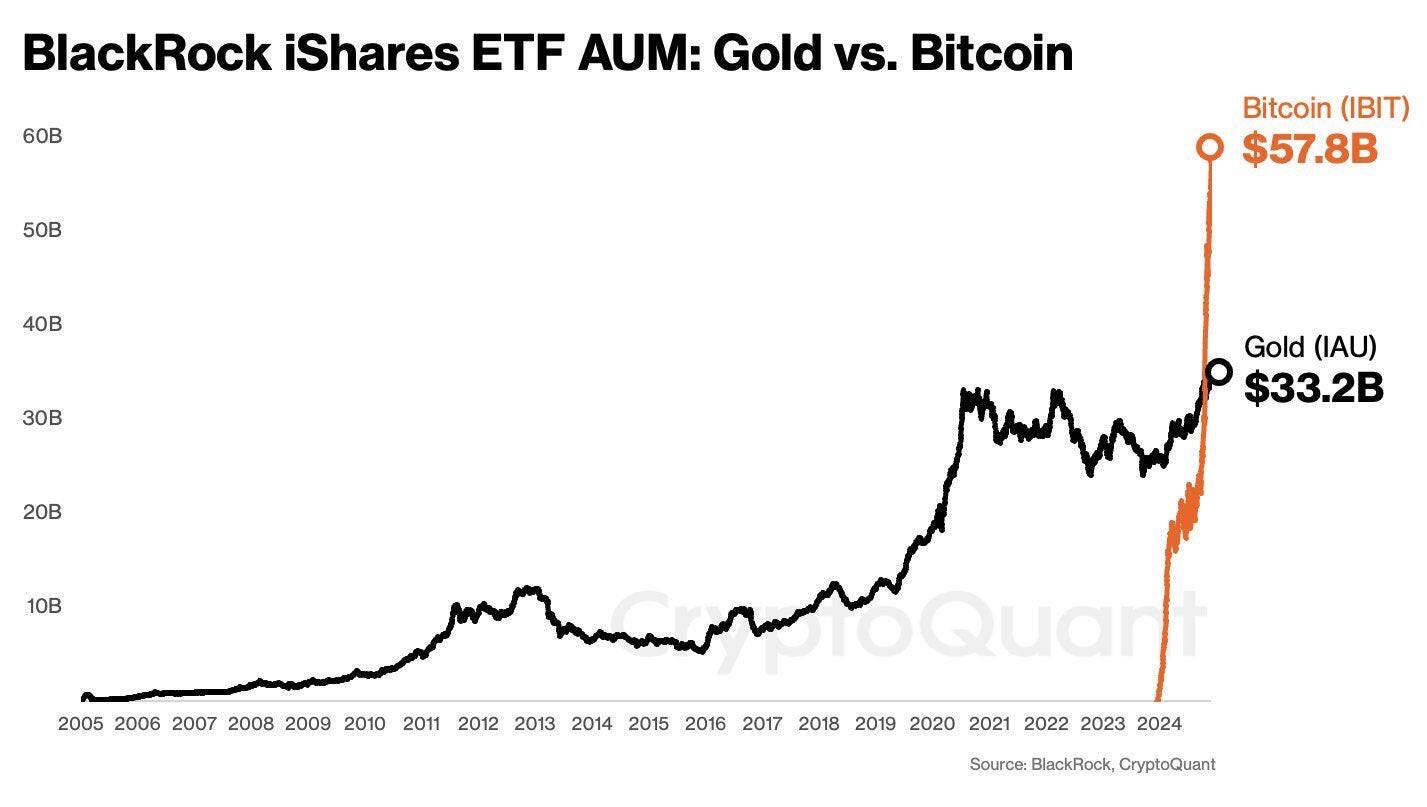

Even amid the broad market choppiness, spot bitcoin ETFs still registered net positive flows of ~$500 million on the week.

US existing home sales jumped significantly in November, up 4.8% M/M for the highest reading in eight months (though still well below pre-COVID trend). US GDP growth estimates for the third quarter were also revised higher this week, moving up to +3.1% Y/Y vs the +2.8% reported previously.

Less encouragingly, new data out of the Philadelphia Fed suggested US payrolls actually declined by 0.1% for Q2 (vs the BLS’s initial estimate of 1.1% growth from a few months ago).

Overseas, China’s 10-year government bond yield extended its recent rapid decline this week, falling ~40bps on the month and breaking below the 2% level for the first time ever as macro data in the country have generally continued to look very weak and regulators have promised even more stimulus to stabilize equity and property markets.

Meanwhile, the Bank of Japan surprised markets by holding its benchmark rate steady instead of hiking, driving the JPYUSD down to levels not seen since August’s sharp move higher.

Regulatory Update

The Bitcoin Policy Institute published a paper dissecting some of the problematic precedents set by the DOJ’s case against Samourai Wallet. Counsel for Samourai also appeared on the What Bitcoin Did podcast to discuss the case and its concerning implications.

Elsewhere, the Bitcoin Policy Institute published a draft executive order that would direct the creation of a $21 billion strategic bitcoin reserve, as well as a proposal for de minimis tax exemptions for small bitcoin transactions.

An Ohio state representative introduced a bill that would create a framework for a strategic bitcoin reserve at the state level.

Meanwhile, a French MP for the European Union called for the creation of a strategic bitcoin reserve in the EU, and Germany’s outgoing finance minister publicly expressed regret that Germany has not taken advantage of bitcoin.

The Senate Banking Committee will not move forward with a re-nomination of SEC Commissioner Caroline Crenshaw, who voted against the approval of spot bitcoin ETFs earlier this year.

Noteworthy

El Salvador reached a new deal with the IMF that will see the country relax some of its bitcoin acceptance laws, shutter its Chivo Wallet, and make taxes payable only in US dollars. The country reportedly still plans to continue building its national bitcoin reserves.

Chinese automaker Cango surprisingly emerged as the third largest publicly traded bitcoin miner this week, as the company has recently acquired 32 EH/s of ASICs.

The latest CNBC CFO Council survey showed only 11% of respondents now view bitcoin as “a fraud,” down from 28% in 2017 and 19% in 2021, while the percentage holding no view at all has declined from 30% in 2017 to just 4% today (though interest in adding it to corporate reserves still remains limited).

MicroStrategy announced that Brian Brooks, former US Comptroller of the Currency, and Jane Dietze, Chief Investment Officer at Brown University, have joined the company’s Board of Directors.

Travel

Austin BitDevs, Jan 16

Nashville BitDevs, Jan 28