Ten31 Timestamp 891,077

Are you not entertained?

After months of speculation and hand-wringing, Liberation Day finally arrived and was immediately successful in liberating the world from high asset prices. In the hallowed Rose Garden, President Trump pulled out an oversized infographic informing the world that it’s time to pay what he deems their fair share, as the US will now be charging a blanket base tariff of 10% on all imports, as well as all-in duties running higher than 50% for some countries including China. The tariffs were notably more aggressive than pretty much anyone’s worst case expectation, and the proposed rates for most countries appear to be significantly higher than the simple “reciprocal” tariffs the administration has floated for the past few weeks, ostensibly in an effort to fully account for all the non-tariff trade barriers erected by America’s various trading partners. Trump’s proposal sent shockwaves through markets, with investors trying to decipher what’s going on here – is it just another Art of the Deal negotiating tactic? Is he trying to force the Fed’s hand? Is this an attempt to scare risk capital into Treasuries for better refinancing rates? Should it just be taken at face value as an historically aggressive gambit to reshore manufacturing? Maybe a little of each? Regardless of the right answer, investors shot first and sent equities tumbling, with both the S&P500 and Nasdaq down over 10% in just the last two trading days of the week.

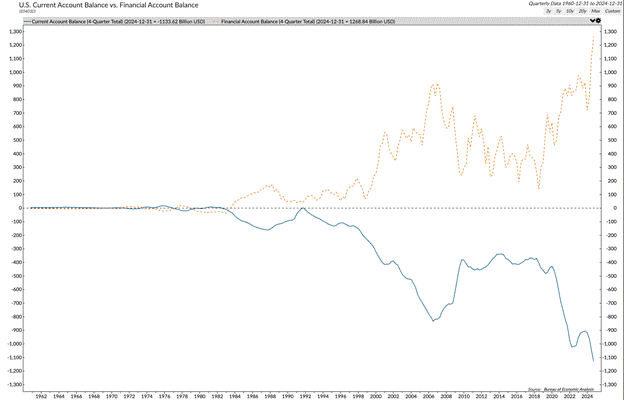

Whether President Trump knows it or not (we suspect some on his team definitely know while others may not fully grasp it yet), if anything like this tariff regime sticks, the new framework will be a direct repudiation of the post-1971 order of global trade. As Robert Triffin explained decades ago, our trade imbalances are not ultimately a matter of unfair or manipulative trade policies by our dastardly neighboring countries (though certainly such policies likely exist), but rather a structural overvaluation of the US dollar as the world’s reserve currency and US Treasuries as the world’s reserve asset. The whole deal in this historically unprecedented global experiment following the Nixon Shock is that the US prints dollars and financial assets and provides a global security apparatus, while the rest of the world in turn produces manufactured goods for export and recycles the resulting trade surpluses largely into US assets – said another way, we have a massive capital surplus on the other side of our trade deficit. To the extent that the administration chooses to make such foreign exports prohibitively expensive and truly wants to rebuild its manufacturing base – and there may well be strong arguments in favor of that path – the other side of that coin is a sacrifice of USD-denominated and USG-issued assets as the default savings account of trade surplus nations (a dynamic China has perhaps been front-running for the past decade).

{kind=link}

Whatever the reality and however the policy path shakes out, we continue to think the events of the past few months have validated the macro case for neutral assets in general and bitcoin in particular like never before. If the above scenario plays out and the US is serious about totally reworking global trade, the world will be in the market for new store of value assets to replace at least some percentage of their US Treasuries, Magnificent 7 holdings, and Park Avenue real estate, and there’s no better home for that capital than a non-sovereign, instantly transportable, highly resilient asset with credibly fixed supply. If, on the other hand, the shock of Trump’s proposal and attempts to enforce it plunges the world into recession as many mainstream economists fear, the inevitable result with US Debt / GDP above 120% and interest expense already north of defense spending will be a new wave of central bank liquidity that bitcoin will absorb better and faster than any alternative. When coupled with the Trump administration continuing to take steps to embrace sound money assets like bitcoin, we think all paths are increasingly converging on the orange block road, which may partially explain bitcoin’s impressive relative resilience this week.

Portfolio Company Spotlight

Giga Energy is a leading bitcoin mining and data center infrastructure provider. The company helps energy and power producers use bitcoin mining to optimize production and more efficiently use resources that would otherwise be wasted, through both proprietary mining deployments and the provision and operation of tailored power generation equipment including generators, data centers, and electrical infrastructure. Giga sits at the forefront of the convergence of the energy production and bitcoin mining industries, a trend we expect to gain notable momentum over the coming decade.

As the world’s largest investor focused entirely on bitcoin, Ten31 has deployed nearly $150 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem, and we expect 2025 to be the best year yet for both bitcoin and our portfolio. Visit ten31.xyz/invest to learn more and get in touch to discuss participating.

Selected Portfolio News

Battery Finance Founder and CEO Andrew Hohns collaborated with Matthew Pines of the Bitcoin Policy Institute to publish a policy brief on BitBonds:

Giga Energy announced a re-branding alongside some statistics on the company’s impressive growth:

Media

Ten31 Managing Partner Matt Odell hosted a fireside chat with Tennessee Governor Bill Lee on the growing role of bitcoin mining in local energy grids and the increasing divergence of pro-bitcoin states like Tennessee from much of the rest of the country.

Ten31 Advisor and Zaprite Head of Business Development Parker Lewis gave a talk at this year’s Bitcoin Takeover on Zaprite’s approach to building infrastructure for bitcoin payments.

Market Updates

The American Golden Age got off to a swimming start this week, as US equities officially closed out their worst quarter since 2022 (so far).

The second quarter kicked off with the hotly anticipated “Liberation Day,” the Trump administration’s announcement of its proposed tariff framework. President Trump announced a 10% blanket base tariff on all imports, with substantial incremental duties on a list of countries the President deems to be particularly bad actors, including all-in rates well north of 30% for China, Vietnam, and others.

The administration has spent much of this year indicating that the tariffs would largely be reciprocal in nature, but the calculation of reciprocality underlying this proposal seems to go well beyond standard measures in an effort to fully capture all international trade barriers.

This policy shift was just a bit outside of what most investors expected and prompted an immediate and intense selloff, with the S&P 500 and Nasdaq totally reversing recent relief rallies to put in new YTD lows. All key US indices lost 10% or more over the last two trading days this week and posted the worst one-day performance since 2020’s COVID crash.

At the same time, the US 10-year Treasury yield finally started to show some real downward momentum, heading below 4% for the first time since October (though the benchmark rate interestingly gave back some of that progress and closed Friday right at 4%).

The DXY Index of USD strength also moved in tandem with US yields, breaking lows not seen since last October before regaining a bit late Friday.

China was quick to respond with their own extremely high retaliatory tariffs, a move Trump quickly dismissed as “panic.” On the opposite end of the spectrum, Trump indicated that Vietnam has already expressed a desire to eliminate their tariffs entirely.

Amid the carnage, President Trump reposted a video from his Truth Social account explicitly indicating that the administration’s strategy is to scare capital into US Treasuries to lower yields while also forcing the Federal Reserve’s hand to cut rates, perhaps an oddly overt admission for a man many regard as the reincarnation of Sun Tzu.

To the extent that is indeed the plan, we continue to wonder whether the Treasury may need a bigger boat to get yields materially lower, particularly since Fed Chairman Jerome Powell insisted again on Friday that the central bank doesn’t need to be in a hurry to cut rates.

Even so, investors responded to the week’s violent moves by upping bets for additional FFR cuts this year, with consensus now settling on 4-5 cuts vs the Fed’s stated plans for just 2.

Overseas equity indices weren’t immune from the pain this week either, as the Japanese Nikkei Index continued its recent selloff and reached its lowest level since last summer’s Yen carry trade unwind. The German DAX Index also gave up most of its recent gains.

As the world tries to digest what could be a generational shift in the order of global trade and capital flows, it’s interesting to note that gold was among the few goods explicitly exempted from the tariff proposals.

Meanwhile, gold transfers into US-based Comex vaults have continued to go vertical, blowing past record highs set in 2020.

In another noteworthy signpost, Treasury Secretary Scott Bessent noted without prompting in a Tucker Carlson interview Friday that bitcoin is becoming a store of value comparable to gold.

While the tariff noise and resulting equity bloodbath drowned out almost everything else, the US actually saw some half-decent jobs reports for March, with both ADP and Non-Farm Payrolls coming in a bit better than expected.

However, new job cuts also increased sharply in March (largely driven by DOGE activities), and prints for both ISM Manufacturing and Services were weak, with Services in particular putting in its weakest reading since last June.

Also buried in some of the week’s headlines was a report that Elon Musk is likely to step back from his role in the Trump administration shortly, potentially further undermining the credibility of the DOGE narrative following record-breaking federal deficits in January and February.

Through all the volatility, bitcoin held in quite well, closing the week basically flat against a backdrop of massive equity drawdowns. That said, bitcoin typically front runs broader markets in both directions, so the asset likely also pulled forward much of this downdraft over the last 6 weeks.

Finally, it proved to be a poetic week for BlackRock to release its annual Chairman’s Letter to its shareholders, as world-renowned bitcoin influencer Larry Fink continued to sound more and more like a 2011 Ron Paul speechwriter with his declaration that the US federal debt burden may ultimately threaten the dollar’s reserve currency status in favor of something like bitcoin.

Regulatory Update

Texas Senator Ted Cruz introduced the FLARE Act, which would enact measures to incentivize energy producers to use bitcoin mining to capture natural gas that would otherwise be flared or vented.

A new bill proposed in Rhode Island would allow state residents to spend up to $10,000 in bitcoin per month without incurring local capital gains taxes.

The SEC officially clarified that stablecoins meeting certain conditions are not securities, though it’s unclear if the agency’s criteria would exclude Tether, the leading stablecoin by market cap.

Noteworthy

President Trump’s sons founded a new bitcoin mining venture in collaboration with public miner Hut8, the latest sign of the Trump family’s growing involvement with bitcoin-oriented ventures.

Elsewhere in public bitcoin miners, IREN paused bitcoin hashrate expansion to focus on further buildouts of HPC capacity, and Chinese automaker Cango announced a sale of its auto business to fully focus on its bitcoin mining operations.

The storied Bitcoin Dev mailing list – which recently migrated to Google Groups – was briefly and unexpectedly banned from the platform this week, apparently due to “unwanted content.” Access has since been restored, but the episode is the latest indication of the vulnerabilities posed by centrally controlled communications platforms and the corresponding need for protocols like Nostr.

Travel

BitBlockBoom, Apr 5

MIT Bitcoin Expo, Apr 5-6

Austin Bitdevs, Apr 17

Bitcoin 2025, May 27-29