Ten31 Timestamp 910,330

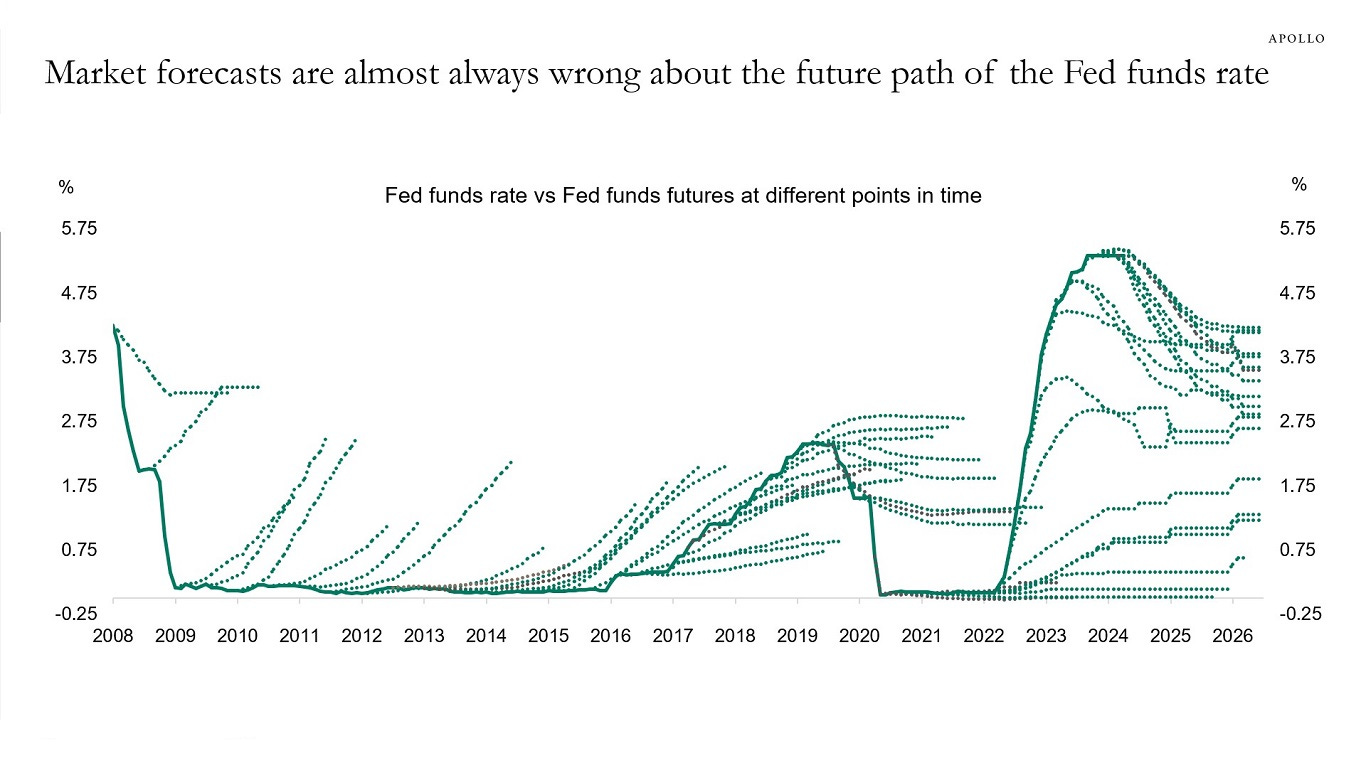

Investors continued to digest Schrödinger’s Rate Cut this week, as July’s headline CPI came in well below expectations, instantly giving the Trump administration more air cover to push for lower benchmark interest rates. Treasury Secretary Scott Bessent suggested rates should be cut by up to 175bps, while Trump himself once again proposed that a rate as low as 1% should be considered, and Fed Funds Futures quickly moved to price in a ~98% chance of a cut at the next Fed meeting. However, some components of the headline were potentially more concerning, and those concerns were intensified by the PPI figures released a few days later, which came in substantially above consensus estimates and potentially hinted at the start of some tariff flowthrough. Regardless, Trump’s team is now engaging in a very public Fed Chair interview process among up to 11 candidates who seem to be in a mini-Hunger Games battle where the object is to signal as much monetary accommodation as possible, so we continue to think the ultimate policy pathway is nearly locked in regardless of what happens at Jackson Hole or the next FOMC meeting. While policy wonks may argue that Trump’s focus on rate cuts is unreasonable given a backdrop of all-time high asset prices, we suspect that the latest federal deficit numbers for July and the administration’s ongoing escalation of fiscally aggressive industrial policy (including the suggestion of a direct federal stake in Intel this week) will ensure a continued insistence on lower rates, for better or worse.

Bitcoin responded to the whipsawing of the inflation picture by briefly breaking out to a new all-time high of almost $125,000 before retrenching back to its recent consolidation range just under the $120,000 level. At least some of the selloff was likely driven by Secretary Bessent’s apparent suggestion that the US will not look to buy more bitcoin for the strategic bitcoin reserve, though Bessent later backtracked (or clarified, depending on your point of view). We continue to believe it’s extremely likely that the most powerful government on earth – which is in a potentially existential geopolitical battle to shore up its wobbling fiscal position and maintain its current level of global hegemony – will want to aggressively accumulate a meaningful share of the scarcest asset on the planet (whether or not said government ever chooses to announce or affirm this intention), but either way, the week was filled with evidence that other major institutions are continuing to load up on the orange coin.

Bitcoin’s latest all-time high was also accompanied by a new high for publicity of “Digital Asset Treasury” (DAT) companies, some of which substantially upsized their public offerings to acquire various altcoins on the hopes that such tokens will benefit from the recent boom of interest in stablecoins. We found it telling, then, that the week saw multiple announcements of proprietary blockchains from major players like Circle and Stripe that will be dedicated to facilitating their own stablecoin flows, outside the purview of the so-called “public” blockchains ostensibly set to benefit from stablecoin growth. As the market piles into DATs partially on the thesis that the blockchains underpinning these tokens will be the new “rails” for the (allegedly) emerging stablecoin economy, we encourage investors to consider how the value accrual pathway for these tokens might be challenged by the growth of private blockchains (which just get us one step closer to simple centralized databases, the logical conclusion of non-bitcoin blockchains). A weekend review of the relevant literature may be instructive in helping capital allocators to stay humble and stack sats.

Portfolio Company Spotlight

Satoshi Energy provides market-leading services and analytics for behind-the-meter data center development projects bringing together bitcoin mining operators, high-performance compute projects, and power producers. The company offers plug and play power contracts and project monitoring services, as well as cutting edge tools for sites to manage credit exposure and real-time settlement of invoices. With a large pipeline of projects under development and a growing suite of products and services, Satoshi Energy is pioneering the accelerating convergence of power production and advanced data centers.

As the world’s largest investor focused entirely on bitcoin, Ten31 has deployed $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem, and we expect 2025 to be the best year yet for both bitcoin and our portfolio. Visit ten31.xyz/invest to learn more and get in touch to discuss participating.

Selected Portfolio News

Fold posted very strong Q2 2025 results this week:

Fold also announced that its bitcoin gift cards are now live on giftcards.com, one of the most active gift cards sites in the world:

AnchorWatch announced it now offers K&R coverage on top of its unique, industry-leading 1:1 bitcoin insurance policies:

Strike rolled out a more detailed dashboard for tracking cost basis data:

Media

Unchained’s Jon Melton joined the Investor’s Podcast to discuss the growth of bitcoin-backed lending and the emergence of bitcoin as pristine lending collateral.

Market Updates

The latest CPI reading came in at +2.7% Y/Y, a bit below consensus expectations, even as the “Core” reading (ex-food and energy) moved back above 3% again for the first time in several months.

The calls for near-term Fed rate cuts followed very quickly thereafter, with both Wall Street strategists and Treasury Secretary Bessent suggesting the central bank now has room for a half-point cut in September.

Bessent also indicated the FFR should ultimately be 150-175bps lower (so ~3% or less), and President Trump perhaps unsurprisingly indicated the rate should be just 1%.

Amid the slightly softer data and rallying cries from the administration, Fed Funds futures quickly moved to bake in as much as a 98% probability of a cut next month.

However, these projections have almost always been wrong (even just 1-2 months out), and the PPI data released later in the week threw a major wrench into this narrative.

The wholesale inflation data ticked up meaningfully, with the index showing a +0.9% M/M jump vs expectations of just +0.2%, the largest increase since March 2022, with several of the figure’s major drivers potentially showing the early stages of tariff impacts. While one interpretation of the two reports is that producers are largely eating tariffs and not passing them on to consumers, it’s unclear how long that dynamic might prevail.

While the inflation story remains murky, the Trump administration maintained its adversarial stance toward what it sees as a dysfunctional Federal Reserve, as Trump suggested he’s now considering a lawsuit against Jerome Powell regarding the central bank’s new headquarters.

Meanwhile, Bessent indicated that he sees “foundational issues” at the central bank that need to be addressed. Perhaps the Fed and Treasury should reach an agreement on how to address these differences…maybe some kind of “accord”?

After pointing to a preference last week for Christopher Waller to replace Jerome Powell, President Trump is now reportedly considering a list of up to 11 candidates, including several current Fed Governors, BlackRock’s CIO of Fixed Income, and Kellyanne Conway’s boyfriend.

Notably, shortlist candidate Marc Sumerlin took to CNBC this week to support the idea of a 50bps rate cut in the near term, potentially part of his audition for the big seat.

All-time high stock prices or not, we expect this issue is not going away anytime soon given the federal government’s clear appetite to ramp spending and borrowing, with July’s Treasury statement snapping back to a $291 billion deficit for the month, reversing a small surplus from June and putting the department on pace for a $1.9 trillion deficit to round out the year.

We’d expect this pace to continue ticking higher going into next year partially thanks to what appears to be a growing appetite for outright industrial policy on the part of the new administration. Following last month’s deal to make the Pentagon the largest shareholder in MP Materials, Trump floated the idea of the government taking a direct stake in chip giant Intel (but only after demanding that the CEO resign immediately due to his alleged connections to China).

On the same theme, Nvidia and AMD announced a deal to pay 15% of their revenues from China sales directly to the US government. Headlines like these suggest the administration increasingly views this as a wartime economy, and we encourage investors to consider what that might mean for federal spending and non-state monetary assets.

That said, the tariff story saw some slight de-escalation this week, as Trump confirmed that gold bars will in fact not be subject to tariffs, as feared last week. The President also said he’ll hold off on new China tariffs after his successful meeting with Russian leader Vladimir Putin in Alaska.

Following several headlines last week about the potential IPO of Fannie Mae and Freddie Mac, Trump hinted at a “Great American Mortgage Corporation” listing as soon as November 2025.

On the 13F front, it was yet another week of strong institutional accumulation of bitcoin ETFs, as Abu Dhabi’s sovereign wealth fund and Hong Kong-based Avenir both pointed to significant increases in their IBIT positions in Q2.

Large institutional investor Brevan Howard also more than doubled its position in IBIT and is now the largest disclosed holder of the ETF.

Regulatory Update

Bo Hines, the White House’s special advisor for digital assets, announced his resignation and intention to return to the private sector. At his departure, Hines indicated that the administration’s plan to grow the strategic bitcoin reserve will “continue and accelerate.”

Treasury Secretary Scott Bessent threw some cold water on that message, though, indicating in somewhat awkwardly phrased commentary that the government “won’t be buying” bitcoin for the SBR. However, later the same day (and potentially after a few frantic donor phone calls), Bessent tweeted that the Treasury continues to evaluate budget-neutral ways to accumulate bitcoin.

New reports this week indicated that the Google Play store will no longer allow noncustodial bitcoin wallets unless app developers have MTLs or a banking license. After significant public backlash, including by Block CEO Jack Dorsey, Google walked back the policy, though it remains unclear whether this was an oversight or just a trial balloon.

The Bank for International Settlements published a proposal for a new system to “score” bitcoin wallets for KYC/AML purposes, with lower-score wallets potentially to be flagged as risky or non-compliant by exchanges.

More encouragingly, the Federal Reserve announced it will sunset its “novel activities supervision program,” which had previously been part of the more adversarial, anti-bitcoin banking regime that characterized the prior administration.

Noteworthy

After much speculation and excitement, Block unveiled its new Proto bitcoin miner. The mining industry broadly greeted the news very positively, as the unit’s specs are roughly on par with the latest state of the art from leading Chinese producer Bitmain, while offering a modular design intended to minimize repair downtime and potentially allow for a much longer useful life.

Leading stablecoin platform Circle (issuer of the USDC token) and payments giant Stripe are both reportedly developing their own proprietary blockchains dedicated specifically to stablecoins, a development that doesn’t surprise us but also may pose challenges to the stablecoin-linked value accrual thesis associated with many non-bitcoin blockchains.

Public bitcoin miner TeraWulf announced that Google has taken an 8% stake in the company as part of a hosting agreement for high-performance compute capacity.

Travel

Bitcoin Park Imagine IF Summit, Sep 19-20

Portfolio Company Retreat, early October