Ten31 Timestamp 911,334

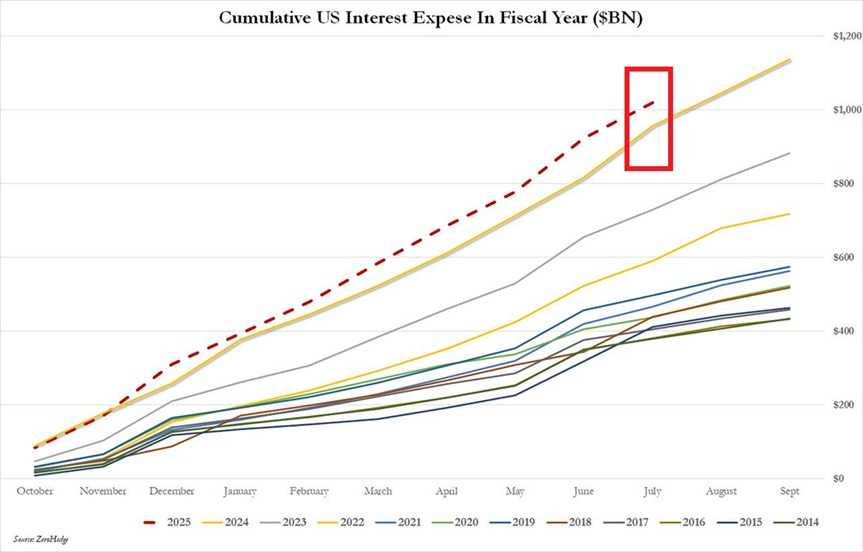

After a relentless downward head-fake as investors digested a week of data points and Fed commentary pointing away from near-term rate cuts, Jerome Powell delivered just the sugar rush the market was looking for, as his incrementally dovish commentary at Friday’s annual Jackson Hole speech sent equity indices right back to all-time highs. While the besieged Fed Chairman’s statement was perhaps a bit less overtly expansionary on a few key points than the market reaction might suggest, Powell did acknowledge growing risks in the labor market and suggested that “conditions may warrant” a change in the policy rate in the near term, which certainly appears to open the door to cuts at the September FOMC meeting. That said, we still tend to think that obsessing over the minutiae of Fedspeak – or what Alan Greenspan famously called “syntax destruction” – is missing the forest for the trees given the many seismic shifts in the US’s fiscal and regulatory backdrop that were further affirmed this week. An inexhaustive sampling of such shifts includes: YTD federal interest expense broke $1 trillion for this fiscal year with two months still to go, putting the government firmly on pace for its largest annual interest bill in history; President Trump threatened to fire Fed Governor Lisa Cook for what some may call relatively minor ethics violations, potentially setting up the administration to score yet another spot on the FOMC Board; and the US government announced it will take a 10% stake in Intel, making it one of the largest shareholders in the storied American semiconductor pioneer. The upshot is that, one way or another, and regardless of how the FOMC nudges rates in the next couple months, the global hegemon with a money printer and (for now) outsized geopolitical influence will find a way to fund itself and maintain its perceived control over critical resources, and we think it may be worth considering how to position one’s portfolio accordingly.

Portfolio Company Spotlight

OpenSecret provides app infrastructure empowering developers and platforms to better protect user privacy without sacrificing UX. The company provides end-to-end encrypted storage, secure authentication, and privacy-preserving AI integrations, and more. OpenSecret’s private AI tools are exemplified by the company’s Maple AI app, a consumer-facing platform allowing users to make queries to top of the line LLMs with verifiable privacy. These tools will become progressively more important as data breaches get more frequent and large tech conglomerates absorb increasingly sensitive user information from AI chats.

As the world’s largest investor focused entirely on bitcoin, Ten31 has deployed $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem, and we expect 2025 to be the best year yet for both bitcoin and our portfolio. Visit ten31.xyz/invest to learn more and get in touch to discuss participating.

Selected Portfolio News

Zaprite added new features including payment requests:

Media

Strike Founder and CEO Jack Mallers joined Stakwork Founder and CEO Paul Itoi for a featured discussion at the Wyoming Blockchain Symposium.

Ten31 Managing Partner Matt Odell was also a featured speaker at the event.

Elsewhere, Matt was profiled in a Bitcoin Magazine piece covering his work at Ten31 and OpenSats.

The Ten31 team released the latest episode of Bitcoin Alpha covering the tug of war with the Fed, the government’s stake in Intel, and much more.

Market Updates

It started out as a rough week for anyone positioned for a near-term rate cut, as the latest Fed minutes suggested the FOMC remains more concerned about inflation than any softness in the labor market.

Meanwhile, the President of the Kansas City Fed hinted at ongoing hesitation about rate cuts at the September Fed meeting, and Cleveland Fed President Beth Hammack indicated she does not currently support cuts.

The case for a downtick in rates also didn’t get any support from the latest US Manufacturing PMI release, which came in well above expectations for the strongest reading since 2022.

This accumulation of data points weighed on markets all week until Fed Chairman Jerome Powell’s annual Jackson Hole speech on Friday, which acknowledged that current policy is restrictive for the first time since January and indicated that “conditions may warrant” a change in the Fed’s stance given potential downside risk in the labor market.

Powell’s comments also notably pointed to a return to the pre-2020 inflation targeting framework, which eliminates the more flexible “long run average” targeting construct that the central bank adopted in the wake of COVID. This update arguably points to an incrementally restrictive stance on inflation, though some investors seem to have interpreted it in the opposite direction.

In any case, the tone of the remarks certainly seems to open the door to a cut at the September meeting, and this wouldn’t be a moment too soon for the federal government, whose YTD interest expense eclipsed $1 trillion in July with a couple months still remaining in the fiscal year.

Notably, Treasury Secretary Scott Bessent reiterated this week that the GENIUS Act and the proliferation of stablecoins will lead to a “surge in demand” for US Treasuries (whether this plays out in practice is uncertain but also less relevant than the degree to which it has become a clear focal point for the Treasury).

On the same theme, the Financial Times said the quiet part out loud this week, noting “growing pressure” on global central banks to cap interest rates as a means of managing spiraling public debt burdens.

And that pressure on the Fed looks set to keep ramping up, as President Trump demanded the resignation of Fed Governor Lisa Cook this week due to allegations of mortgage fraud. The President later indicated that he’ll fire Ms. Cook if she doesn’t resign.

Trump went on to post what appears to be a Microsoft Paint rendering of his vision of the new Fed Board of Governors, which notably shows how he views the partisan divisions of the board’s current composition. Following the sudden resignation of Adriana Kugler a few weeks ago, another vacant spot would give the administration an opening to potentially tilt the board firmly in Trump’s favor.

Elsewhere in heavy-handed Executive Branch action, the Trump administration confirmed on Friday afternoon that the government has taken a 10% stake in Intel, making it one of the top few shareholders in the beleaguered semiconductor giant.

The investment will not involve the deployment of any new capital but rather will see funds granted to Intel under laws like the CHIPS Act converted to equity, with a warrant for the US to purchase up to 5% more of the company under certain conditions. This represents a substantial escalation from the MP Materials deal we flagged in this newsletter last month, and we think it signals a pretty clear direction of travel for the government’s relationship to what it deems strategically sensitive industries (as well as the private sector generally).

After months of saber-rattling, finger-wagging, and pearl-clutching, Canada quietly dropped most of its retaliatory tariffs against the US.

Overseas, Japan’s 10-year government bond broke out to a new 52-week high while 30-year government bond yields put in new all-time highs this week, a dynamic worth monitoring given the close relationship between Japanese interest rates and the global complex of risk assets.

Bitcoin sagged to as low as $112,000 on the week (imagine reading that just a few years ago) on a particularly rough outflow week for ETFs before ripping back to $117,000 on Powell’s Jackson Hole comments.

Regulatory Update

Eric Trump indicated this week that an unnamed country recently “quietly bought” 200,000 bitcoin without issuing any public announcement, to which we can only say, big if true.

{kind=link}

Senator Cynthia Lummis suggested the so-called digital assets “market structure bill” could be enacted by the end of this year.

Legislators in the Philippines introduced a new strategic bitcoin reserve bill that would direct the country’s central bank to acquire 10,000 bitcoin over the next five years.

Noteworthy

The latest Bank of America fund manager survey indicated that over half of surveyed investors now expect some kind of Quantitative Easing or Yield Curve Control in the US, though curiously the vast majority also report having no allocation to bitcoin despite this viewpoint.

Insurance giant Allianz and Voya Financial released a paper on bitcoin this week that lists the orange coin as a “credible store of value.”

Global stablecoin leader Tether announced it has hired Bo Hines, former digital assets advisor to the White House, to help drive Tether’s US expansion strategy.

Travel

Bitcoin Park Imagine IF Summit, Sep 19-20

Portfolio Company Retreat, early October