Ten31 Timestamp 915,758

After a brutal nine months wandering the desert of a stable Fed Funds Rate, the market finally found its long-awaited rate cut oasis this week, which is a welcome relief with most major asset classes at *checks notes* all-time highs. The path to totally remaking the FOMC to fit President Trump’s policy agenda got incrementally rockier as an appeals court averted the administration’s attempted removal of Fed Governor Lisa Cook, but recent Trump appointee Stephen Miran made his presence felt in the Eccles Building with a much more aggressive rate cut forecast than his peers and, perhaps more significantly, a revived focus on the Fed’s long-forgotten third mandate for “moderate long-term interest rates.” The importance of this pillar of Trump’s overall agenda has only continued to grow alongside the administration’s accelerating push toward a state-managed flavor of capitalism (euphemistically termed “industrial policy”) that looks set to entail not only greater Washington oversight of strategically critical sectors but also significant additions to the federal government’s already bloated budget. At the risk of sounding like a broken record, the President and his advisors seem increasingly committed (boxed in?) to a “run it hot” strategy, and we continue to think the near- to medium-term implications for scarce assets may be profound.

Portfolio Company Spotlight

Giga Energy is a leading bitcoin mining and data center infrastructure provider. The company helps energy and power producers optimize production and more efficiently use resources that would otherwise be wasted, through both proprietary mining deployments and the operation of tailored equipment including generators, data centers, and electrical infrastructure. Giga works with large players including Nvidia, Core Scientific, and Energy Transfer at the convergence of the energy production, high-performance compute, and bitcoin mining industries, all of which are trends we expect to gain notable momentum over the coming decade.

As the world’s largest investor focused entirely on bitcoin, Ten31 has deployed $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem, and we expect 2025 to be the best year yet for both bitcoin and our portfolio. Visit ten31.xyz/invest to learn more and get in touch to discuss participating.

Selected Portfolio News

Maple AI now offers encrypted and fully private voice chat:

StatMuse added comprehensive data for the Champions League:

Strike added new recurring deposit options:

Media

Ten31 Managing Partner Matt Odell appeared on the Bitcoin for Business podcast to discuss Ten31’s strategy and more.

Market Updates

Just hours before this week’s hotly anticipated FOMC meeting, a federal appeals court rejected President Trump’s request to remove Lisa Cook from the Fed’s Board of Governors on a 2-1 decision.

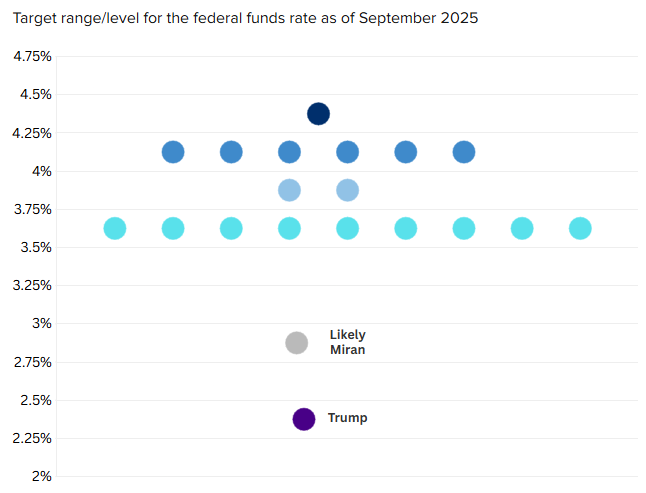

Following that small setback for the administration, the Fed meeting resulted in the 25bps cut to the Fed Funds Rate that the market had been broadly anticipating, with the central bank also signaling it expects two more cuts through year-end.

Notably, recent Fed appointee Stephen Miran – nominated by the White House following the recent unexpected resignation of Adriana Kugler – dissented from the group and argued for a 50bps cut, noting he’s relatively sanguine about the potential for tariff-driven pressure on consumer prices.

Beyond his more aggressive views on rate cuts, Miran also raised some eyebrows this week by calling out the Federal Reserve’s long-forgotten third mandate to maintain “moderate long-term interest rates” in addition to “full employment” and stable consumer prices, clearly pointing to one of Miran’s key priorities for his time with the FOMC.

On the trade front, President Trump demanded this week that all of NATO levy 50-100% tariffs against China as a means of preventing the world’s factory from buying oil from Russia. China, for its part, announced a ban on Nvidia chips for domestic tech companies.

Despite all the consternation, however, Trump assured the world on Friday night that he had a tremendous call with Chinese President Xi Jinping and expects a direct in-person meeting next month.

Treasury Secretary Scott Bessent also indicated a major and long-delayed trade deal with China should be completed before November (hopefully not a manifestation of the principle that the longer you wait, the longer you will be expected to wait).

In support of Bessent’s timeline, the US and China appear to be closing in on a resolution to the long-running TikTok problem. Per reports, Oracle, Andreessen Horowitz, and Silver Lake will form a consortium to own 80% of a new US entity that will operate the popular app domestically, with the remainder owned by Chinese shareholders.

Elsewhere in the federal government’s rapidly expanding industrial policy, the White House is reportedly working on a massive plan to spur additional manufacturing investment in the US that would leverage the $550 billion of domestic industrial funding ostensibly pledged by Japan several months ago.

In a similar vein, the Trump administration invoked its “golden share” in US Steel – recently acquired by Japanese behemoth Nippon with the understanding that the federal government would maintain strategic influence over the company – to prevent the shutdown of a company plant in Illinois.

After some recovery in the past month, the DXY dollar strength index made new YTD lows this week as the market digests the administration’s commitment to a weaker dollar (though the index arguably has much more room to the downside, as it remains historically elevated vs much of the past quarter century).

Despite the Beltway tumult and trade uncertainty, US retail sales data came in strong once again in August, with July numbers also revised higher.

Less encouragingly, subprime auto lender Tricolor filed for Chapter 7 Bankruptcy – opting to liquidate the company rather than restructure – on a spike in delinquent loans, tagging JP Morgan, Fifth Third, and other large banks with losses. It’s unclear at this point whether the bankruptcy was tied more to idiosyncratic issues like immigration or a broader strain on the downmarket consumer.

Overseas sovereign debt markets continued to see increasing volatility this week, as the UK’s latest federal deficit came in much higher than expected despite stronger tax receipts and France’s government collapsed in the wake of the Prime Minister’s resignation.

Meanwhile, the Bank of Japan surprised investors by indicating openness to more rate hikes in the near-term, potentially reintroducing awkward dynamics for the “Yen carry trade” that rocked markets last summer. The Bank also began selling down its $250 billion ETF portfolio.

Regulatory Update

Various bitcoin and crypto industry leaders gathered with several Republican Congressional leaders in Washington to advocate for and discuss the mechanics of building a larger US Strategic Bitcoin Reserve.

Thailand’s government froze several million bank accounts – ostensibly as part of an attempt to crack down on fraudulent activity – before reopening them later in the week.

Noteworthy

A report from Fidelity Digital Assets highlights that bitcoin’s illiquid supply – the aggregate amount of bitcoin that hasn’t transacted in 7+ years – has continued to inflect sharply higher throughout this year, even as large “ancient” wallets have made recent headlines with their reactivation.

Coinbase CEO Brian Armstrong indicated the company is exploring a native token for Base, the company’s proprietary “layer two” built on Ethereum. We see this as yet another data point (following recent announcements of proprietary tokens from Circle and Stripe) undercutting the value accrual narrative for the native tokens of non-bitcoin blockchains.

Google launched a new framework for autonomous agent payments with support for various cryptocurrencies. We expect this kind of agentic payments flow will continue to gain traction over the coming decade, and that it will steadily gravitate toward bitcoin.

Travel

Portfolio Company Retreat, early October

Global Bitcoin Summit, Oct 7-9

Labitconf, Nov 7-8