Ten31 Timestamp 919,671

After President Trump took a hatchet to the tentative trade detente with China last Friday – effectively deleting the accounts of many crypto degens worldwide in the process – this week began with some less aggressive headlines out of the White House, with the President reassuring the public “everything will be fine” and Treasury Secretary Scott Bessent suggesting that all sides would like to de-escalate. However, the administration continues to try to thread the good cop / bad cop needle (often within the same 10-minute CNBC appearance), as Bessent also indicated this week that China can’t be trusted, the US has many levers still to pull, and the administration won’t be deterred by higher volatility in equities. Whatever jawboning and saber-rattling tactics both sides choose to amplify, it seems increasingly unlikely that this genie is going back into the bottle with the US now explicitly promoting industrial policy, Chinese assets in the US sphere of influence being nationalized, and “decoupling” firmly etched into the mainstream policy lexicon. At the same time, US credit markets and liquidity plumbing are possibly starting to get a little squirrely, as it seems more downmarket lending “cockroaches” are scurrying in plain sight every week and key benchmark interest rates are showing irregular excursions outside Fed policy bands (possibly exacerbated by a protracted government shutdown impeding liquidity transmission on the margin). While it’s far too soon to call a 🚨CRISIS😱, we wouldn’t be surprised to see this confluence of developments pull forward a more accommodative Fed stance, particularly as the Trump administration becomes increasingly clear about its many ambitious and fiscally demanding policy objectives.

Portfolio Company Spotlight

Unchained is a bitcoin financial services platform offering a suite of products to consumers and enterprises for securing and managing bitcoin holdings through a multi-signature, collaborative custody model. Unchained’s infrastructure allows users and institutions to hold 2 of 3 keys in a multi-sig quorum, offering customizable custody experiences to meet a variety of personal, family, and business needs while enhancing security and mitigating custody risk. Unchained offers many additional financial services on top of its custody platform, including integrated trading services, bitcoin-backed lending, IRA and inheritance products, a mobile app for easy access to the platform, and much more to come.

As the world’s largest investor focused entirely on bitcoin, Ten31 has deployed $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem, and we expect 2025 to be the best year yet for both bitcoin and our portfolio. Visit ten31.xyz/invest to learn more and get in touch to discuss participating.

Selected Portfolio News

Strike announced the global expansion of its bitcoin-backed lending product:

Maple AI released a new version that represents a major rebuild offering a variety of new features:

Media

Ten31 Managing Partner Matt Odell appeared on the What Bitcoin Did show to discuss investing in open source projects, the nostr ecosystem, bitcoin treasury companies, and much more.

AnchorWatch Co-Founder and CEO Rob Hamilton joined the Guy Swann podcast to talk about the future of insuring non-traditional risks like bitcoin custody.

AnchorWatch Co-Founder and COO Becca Rubenfeld took part in a panel on enterprise custody at this year’s Custody and Treasury Summit at Bitcoin Park.

Market Updates

Following President Trump’s latest Leeroy Jenkins maneuver last Friday, China’s Ministry of Commerce accused the US of deliberately inciting panic over rare earth policy, while issuing a public statement over the weekend emphasizing that recent rare earth mineral controls should not be seen as blanket export bans.

On Sunday afternoon (just in time for the futures open a few hours later), the President returned to social media to assure the world that “it will all be fine” and that the US wants to help rather than hurt China, sending markets higher Monday after the sharp Friday afternoon selloff.

Treasury Secretary Scott Bessent reiterated that the lines of communication between the countries are open and that both sides want to de-escalate, but also suggested the US has many levers it can pull from here and is prepared to be aggressive, while highlighting that stock market volatility won’t deter the administration from pursuing its objectives (we imagine it might be a different story for the MOVE Index, which remains muted for now).

Perhaps more notably, Bessent also suggested China “can’t be trusted” and called for a “decoupling” of global supply chains away from the World’s Factory.

For all the massaged messaging being volleyed across the Pacific, the clearest indication of what time it is came on the other side of the Atlantic, as the Dutch government seized local assets of Chinese chipmaker Nexperia.

The EU, meanwhile, is considering requiring Chinese firms to transfer their technology into the control of local companies if they want to operate in Europe.

Around the same time, China imposed new sanctions on five US subsidiaries of large South Korean shipbuilder Hanwha, which has become increasingly instrumental in maintaining US naval capacity. Taken together, these data points suggest the ongoing and perhaps accelerating fragmentation of global trade into increasingly distinct and controlled spheres of influence.

On the back of these fraying global trade relationships, Secretary Bessent pointed to an explicit plan to ramp up industrial policy – a wartime economic stance and something we’ve been floating in this newsletter for several months – to counter China, a paradigm that would include “price floors and forward buying” (the history of which is admittedly somewhat checkered) as well as more direct equity stakes in strategically sensitive corporations.

Evidence of the growth of these policies was on full display this week, as the Financial Times reported the Pentagon has become much more aggressive in stockpiling critical minerals, while JP Morgan announced plans to invest $10 billion into key national security industries.

Meanwhile, the US is reportedly working on a $20 billion private financing facility for Argentina – coincidentally a major potential source of critical minerals – on top of the $20 billion swap line opened up last week, and President Trump indicated he has authorized covert CIA activity in Venezuela (presumably to Make Regime Change Great Again), two headlines that point to a potential new Monroe Doctrine to counter Chinese influence in the US’s backyard.

Elsewhere in the budding US geopolitical sphere of influence, South Korea expressed optimism this week about its massive, recently announced trade deal with the US, but reiterated its need for its own currency swap line to “ensure commercial feasibility” of the $350 billion proposal.

Newly appointed Fed Governor and low-rates enjoyer Stephen Miran popped his head up to remind everyone that all this global economic reordering is another great reason for more aggressive benchmark rate cuts.

This more accommodative stance perhaps got a bit more credence from the credit markets this week, as JP Morgan CEO Jamie Dimon flagged that recent auto sector debt issues at Tricolor and First Brands are “early signs” of excess in corporate lending and that we should expect more “cockroaches” to emerge in the credit complex.

This proved to be a very well-timed comment, as regional banks Zions and Western Alliance disclosed write-offs and lawsuits related to fraudulent borrower activity this week, taking their stocks down by 10%+ and putting pressure on banking equities overall.

It remains to be seen how much of this noise is idiosyncratic rather than systemic, but regional bank debt seems to be generally holding up for now, and in a headline that should no doubt give everyone comfort, ratings agency Moody’s says the credit complex looks just fine.

In an unfortunately timed development, though, US banking system reserves this week fell below $3 trillion (ostensibly the level the Fed considers to be the minimum threshold to avoid credit spasms), a dynamic exacerbated by the extended government shutdown keeping marginal liquidity trapped at the Treasury.

These factors seem to have driven SOFR to its highest level above the Fed Funds target range (outside of quarter-end window-dressing periods) in several years.

As some potential relief for this dynamic, Fed Chairman Jerome Powell reiterated this week that the central bank is finally getting close to ending its multi-year Quantitative Tightening program of reducing its government bond holdings.

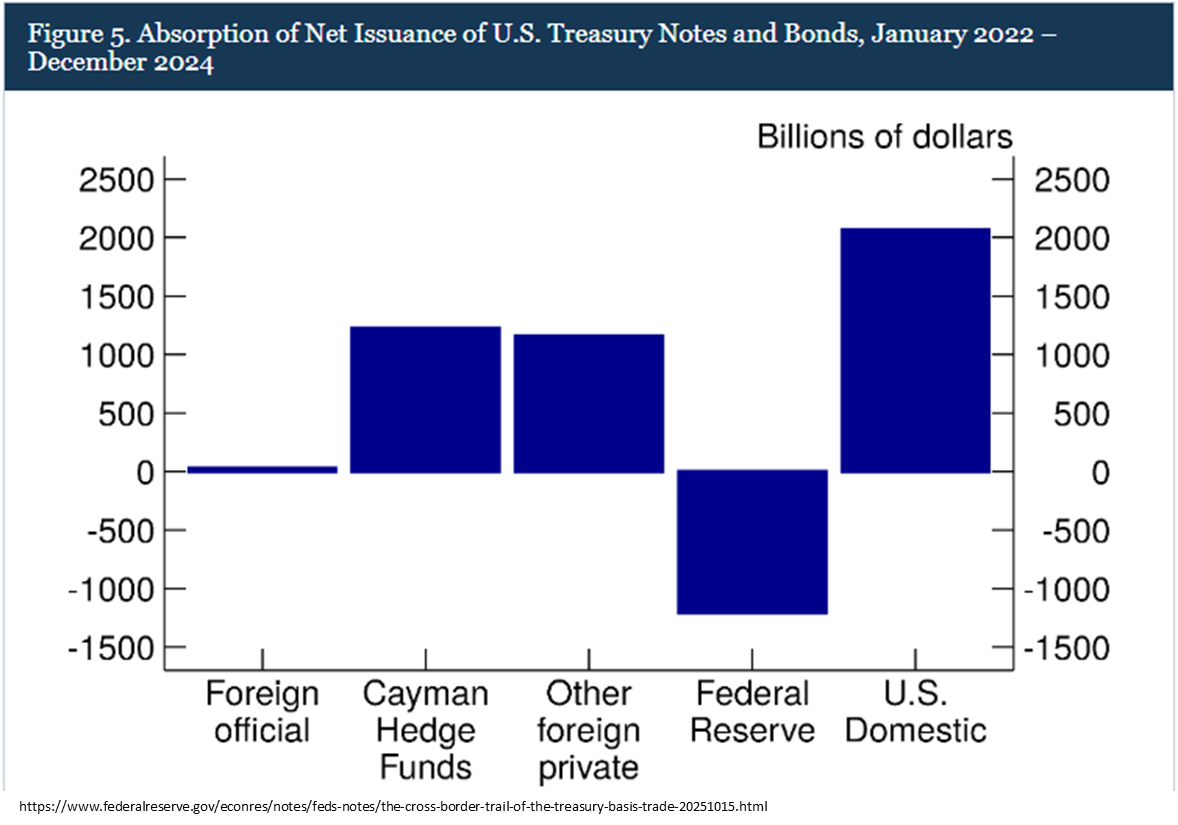

This more accommodative stance is looking more critical every day, particularly given a new Fed paper this week showing that Cayman-domiciled hedge funds engaging in Treasury basis trades are a much greater source of Treasury purchases than previously understood and have been the key marginal buyer in the market for some time:

On the same thread, bank regulators are reportedly planning to increase leverage ratios for community banks, potentially stimulating local lending and, more notably, additional balance sheet capacity for Treasury absorption.

These increasing credit and geopolitical jitters briefly pushed the 10-year below 4% for the first time since last year, while gold extended its monster rally to ~$4,350/oz, good for a +60% YTD move.

But despite all these question marks, the “run it hot” strategy appears to be working well enough for now, as the latest FedNow model points to almost 4% growth for Q3 GDP (though the latest Philadelphia Fed manufacturing index reading came in well below expectations and down sharply after a strong September print).

Bitcoiners didn’t get to join in the goldbugs’ fun this week, as bitcoin remains mired in the sub-$110,000 range following last week’s crypto annihilation. However, leading bitcoin influencer Larry Fink joined 60 Minutes to compare bitcoin to gold, while promoting IBIT on CNBC as the fastest ETF in history to reach $100 billion of AUM. So, we have that going for us.

Regulatory Update

A Florida House representative re-introduced a bitcoin reserve bill that would allow the state to invest up to 10% of its treasury in “digital assets.”

Noteworthy

The US Department of Justice seized over 127,000 bitcoin (over $14 billion) from a Cambodian fraud ring, its largest civil asset forfeiture event in history.

Stablecoin giant Tether donated $250,000 to OpenSats to support open source development in bitcoin and freedom tech.

Not to be outdone, stablecoin challenger Paxos printed $300 trillion of PayPal’s PYUSD token on Ethereum. For those keeping score at home, that’s just slightly more than global GDP.

The developers behind open source ecash project Cashu launched a fork of popular private messaging service Signal that natively integrates simple ecash payments.

Asset management giant Charles Schwab reiterated its plans to launch spot bitcoin trading on-platform next year.

Travel

Labitconf, Nov 7-8

Spot on. Genie's out, AI will only accelarate decoupling.