Ten31 Timestamp 920,727

The temperature was decidedly not turned down during a week filled with headlines pointing to a growing US appetite for (or perhaps just acceptance of) a “decoupled” global trade order. The Trump administration announced several moves that seemed to bring the lines dividing the green, yellow, and red buckets into clearer resolution, including a new critical minerals pact with Australia, firmed up support for Argentina, abrupt cancellation of talks with Canada, aggressive new sanctions on Russian oil, and accelerating military maneuvers at the periphery of South America. Much or all of this may still just amount to the theatrics demanded by the Strategic Uncertainty playbook, but these moves collectively set up an intriguing and precarious backdrop for next Thursday’s pivotal Trump-Xi meeting at the APEC Conference in South Korea. Even after all the posturing, late night tweets, bazillion percent tariffs, and federal equity stakes, the modal outcome is probably still some kind of Artful DealTM given that Nothing Ever Happens. If that’s the case, it’s probably good for another leg up in stonks even from all-time highs, but we think most of the mainstream financial cognoscenti are still underweighting the probability of a more structural, long-lasting shift away from the Acela Corridor’s Flat World paradigm, not to mention the implications that such a transition would have for domestic industry, Fed independence, and scarce, credibly neutral reserve assets.

{kind=link}

Portfolio Company Spotlight

Debifi is a non-custodial lending platform providing institutional-grade liquidity for P2P loans backed by bitcoin, the world’s best collateral. The company, founded by Hodl Hodl CEO Max Keidun, offers robust, secure multisig vaults that ensure bitcoin collateral cannot be rehypothecated, solving one of the key problems plaguing most “DeFi” projects. Debifi extends the proven security of Hodl Hodl’s lending model to the institutional sphere and has an exciting roadmap ahead.

As the world’s largest investor focused entirely on bitcoin, Ten31 has deployed $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem, and we expect 2025 to be the best year yet for both bitcoin and our portfolio. Visit ten31.xyz/invest to learn more and get in touch to discuss participating.

Selected Portfolio News

Debifi announced a new partnership with Swiss Bank Sygnum to offer bank-grade bitcoin-collateralized lending secured by Debifi’s multi-sig custody platform:

Media

Battery Finance Founder Andrew Hohns appeared on the What Bitcoin Did podcast to discuss Battery’s strategy and the natural intersection of bitcoin and credit markets.

Ten31 Co-Founder and Managing Partner Jonathan Kirkwood published Bitcoin: Because We’re Right, a new essay on Ten31’s broad approach to the bitcoin ecosystem.

Market Updates

The US and Australia kicked off the week with a new critical minerals pact for rare earths processing projects worth up to $8.5 billion. Regarding the sensitive raw materials that have become a key lever in Chinese trade tensions, Trump assured reporters that we’re about to have “so much critical minerals and rare earths that you won’t know what to do with them.”

Shortly thereafter, the Treasury Department announced significant new sanctions on Russia’s two largest oil companies and their various subsidiaries. Notably, the new measures come with the explicit threat of secondary sanctions on foreign financial institutions transacting with the Russian oil majors, potentially creating another lever to pressure more countries into a US-centric trade sphere.

Later in the week, Trump abruptly shut down trade negotiations with Canada, ostensibly to win one for the Gipper, but perhaps really because of something else.

Down south, the US finalized a $20 billion financing package to support Argentina’s challenged economy (and indirectly US-friendly incumbent Javier Milei), which may have particularly interesting implications for some critical leverage points in the US-China tug of war as Argentina heads to the polls for midterms this weekend.

Elsewhere in Latin America, the US escalated its recent military overtures by moving various assets including an aircraft carrier into position near Venezuela and imposing new sanctions on Colombia’s President, likely signposts of the Trump administration’s attempts to consolidate its control of the Western Hemisphere.

Finally, Reuters reported that President Trump is weighing more aggressive controls on any G7 exports to China made with US software, potentially encompassing a huge array of goods.

Despite all this, a top Chinese official indicated this week that the country is opposed to “decoupling” from the US and wants to find constructive ways to maintain the US relationship (even as the Wall Street Journal reports that Xi’s inner circle is increasingly endorsing a more aggressive stance behind closed doors).

Back at home, the US’s national debt reached the $38 trillion mark for the first time, showing just how much is possible even when the government is shut down. White House Economic Advisor Kevin Hassett suggested the shutdown could end this week, which proved to be juuust a bit outside.

Perhaps somewhat encouragingly, the US posted a $198 billion budget surplus for the last month of the fiscal year, though the lion’s share of the final tally seemed to be driven by one-time items and timing adjustments.

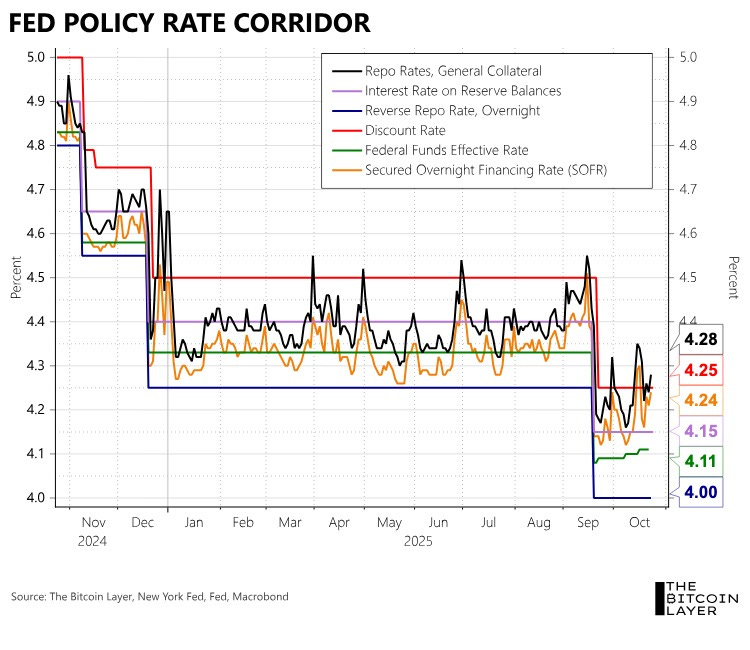

Some key benchmark US interest rates once again drifted back above the Federal Reserve’s policy corridor after getting some relief late last week, potentially exacerbated by the marginal strain on liquidity from the shutdown.

Meanwhile, banking system reserves continued to decline and remain below the closely watched $3 trillion threshold, and the Fed’s Standing Repo Facility – intended to backstop tightness in the repo market – has been tapped with growing frequency (albeit in small quantities) for the first time in years, and atypically outside of a quarter-end period.

On the positive side for the credit complex, default rates in various parts of the economy seem to be rolling over.

September CPI came in at 3%, still firmly above the Fed’s long-held 2% target but slightly below consensus expectations, likely firming up the path for more rate cuts at next week’s FOMC meeting. At the same time, US PMIs in both manufacturing and services moved up slightly M/M.

New Japanese Prime Minister Sanae Takaichi announced a new economic package to support various strategic sectors and combat inflation, embracing the time-tested practice of reducing inflation by ramping up federal subsidies.

Bloomberg reported that JP Morgan plans to allow bitcoin to be used as collateral in some institutional loan arrangements, the latest sign of the US’s largest financial services institution slowly capitulating to the influence of Satashi’s pet rock.

Regulatory Update

In a rare move, the Department of Energy directed the Federal Energy Regulatory Commission (FERC), which has jurisdiction over interstate electricity transmission, to initiate rulemaking related to interconnecting large loads, particularly those facilitating AI and manufacturing buildouts, to the interstate transmission system. Notably, the order recommends expedited pathways for flexible power loads (e.g. bitcoin mining).

President Trump issued a pardon to Binance Founder, crypto luminary, and recent World Liberty Financial partner Changpeng Zhao (“CZ”), who was convicted of money laundering in 2023.

Noteworthy

The team behind Bitkey – Block’s recently launched bitcoin wallet – announced “Chain Code Delegation,” a new BIP that aims to offer better privacy for collaborative bitcoin custody setups, potentially allowing co-signers to participate in wallet recovery without knowing total user balances.

Travel

Labitconf, Nov 7-8