Ten31 Timestamp 925,785

Markets flipped the Over / Back switch emphatically into We’re So Back mode heading into the long weekend, as the S&P500 and Nasdaq reversed much of the selloff from the prior few weeks and bitcoin reclaimed the $90,000 level, moving up as much as 17% from recent local lows. At least some of the improved sentiment was driven by tacit – but increasingly explicit – acknowledgments by the Trump administration that we are on the road to making AI too big to fail, as Crypto and AI Czar David Sacks highlighted how critical the AI capex buildout has been to the US real economy avoiding recession, while solemnly warning that “we can’t afford to go backwards.” President Trump himself followed up with an executive order establishing the “Genesis Mission,” which inaugurates a broad array of new AI initiatives and lays the groundwork for more slush funds budget allocations to ensure the United States emerges victorious in a program the administration views as comparable to the Manhattan Project. Further buoying sentiment this week were growing rumors that longtime Polymarket favorite Kevin Hassett – an outspoken inflation dove, close Trump ally, and former advisor to Coinbase – is likely to get the nod as the next Fed Chair. Meanwhile, the US’s key banking regulators moved even closer to exempting Treasuries from statutory leverage ratio calculations, potentially reopening a valve for federal debt absorption that has been partially closed off since the 2008 financial crisis. With Treasury Secretary Scott Bessent assuring his CNBC audience that the US won’t enter recession next year, the plan to run it hot to defeat America’s key geopolitical rivals (and / or to get reelected, depending on your perspective) appears to be taking shape more clearly by the week, and we continue to think that points to one ultimate outcome for hard assets.

Portfolio Company Spotlight

Start9 provides software and hardware to empower users to easily take control of their digital lives by self-hosting their own personal servers independent of third parties. With intuitive mass market software and one-click installations of popular programs like Bitcoin Core, Mempool.space, various lightning implementations, and 30+ other services, Start9 enables a move away from the current computing paradigm of custodial services that limit privacy, data integrity, and personal autonomy. The company’s exciting roadmap aims to do for personal servers what Microsoft and Apple did for personal computing, which we expect to become progressively more valuable over the coming decades as financial and tech counterparties become less reliable and more invasive.

As the world’s largest investor focused entirely on bitcoin, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem, and we expect 2025 to be the best year yet for both bitcoin and our portfolio. Visit ten31.xyz/invest to learn more and get in touch to discuss participating.

Selected Portfolio News

Strike now offers lending to customers in Michigan:

Media

Maple AI Co-Founder Mark Suman appeared on the What Bitcoin Did podcast to discuss the importance of private and decentralized AI tools.

AnchorWatch Co-Founder and CEO Rob Hamilton also joined What Bitcoin Did to dig into recent controversies in bitcoin.

The de-banking of Strike Founder Jack Mallers was featured in several media outlets.

Upstream Data Founder and CEO Steve Barbour appeared on the Blockspace podcast to discuss the latest in bitcoin mining.

Market Updates

White House Crypto and AI Czar (and erstwhile Chamath hype man) David Sacks kicked off the week with a Twitter post highlighting how crucial the unprecedented scale of hyperscaler capex has been for the US real economy, noting “we can’t afford to go backwards.”

While Sacks quickly clarified that he was not attempting to justify a federal backstop for the AI buildout – contrary to the trial balloon floated by OpenAI’s CFO a few weeks ago – President Trump shortly thereafter signed an executive order inaugurating the “Genesis Mission,” a sweeping set of AI-adjacent initiatives aimed at helping the US navigate what the administration calls this century’s Manhattan Project.

Whether you believe this is all laying the groundwork for direct federal support or is just the latest example of the administration’s foray into explicit industrial policy, it’s clear that keeping the capex fire burning is a critical component of Republicans’ plan to manage electoral sentiment into mid-terms, by which point Treasury Secretary Scott Bessent said he expects the US to be experiencing a “strong, noninflationary growth economy.”

Bessent did acknowledge that more interest rate-sensitive sectors are likely to remain under pressure in the near term, though the trends seem to be easing up on that front, as the Wall Street Journal’s Fed mouthpiece reported that Fed Chairman Jerome Powell’s allies are opening up the path to another rate cut in December, an outcome futures markets have now largely priced in once again.

Bessent’s remarks this week also acknowledged that the Fed has taken the country into a regime of ample reserves (as opposed to the looser “abundant reserves” regime of years past) which now “may be fraying.”

Right on cue, SOFR once again climbed above the top end of the Fed’s current policy rate corridor this week, while use of the Standing Repo Facility also ticked up through the weekend (though absolute numbers here still remain manageable and were likely affected by month-end / holiday timing).

President Trump’s year-long crusade for lower rates looks set to gain additional momentum early next year as well, as Bessent indicated Trump will likely announce his pick for Fed Chair before Christmas, and Bloomberg reported that the White House is leaning toward Kevin Hassett.

Hassett – currently the Director of the National Economic Council and the Polymarket favorite for the past several months – has openly called for lower rates all year, and it’s worth noting he previously served as an advisor to Coinbase (and remains a significant shareholder).

Secretary Bessent has repeatedly indicated – and reiterated this week – that he envisions a new paradigm whereby the Fed progressively “moves into the background” relative to the Treasury, and he might have gotten an important step in that direction this week, as the FDIC voted to advance measures proposed earlier this year to relax the weighting of commercial banks’ US Treasury holdings in the Supplementary Leverage Ratio (SLR), potentially opening up the banking system to move back into a role of federal debt absorption that it has largely ceded to households and hedge funds in recent years.

This update still needs authorization from the OCC and the Fed itself, but newly appointed Fed Governor Stephen Miran issued a statement not only agreeing with the FDIC vote but saying regulators should go even further and remove Treasuries from the SLR calculation entirely. It’s worth noting that, while this change would no doubt open up new capacity for quasi-private Treasury demand, there’s likely more than meets the eye at stake under the surface.

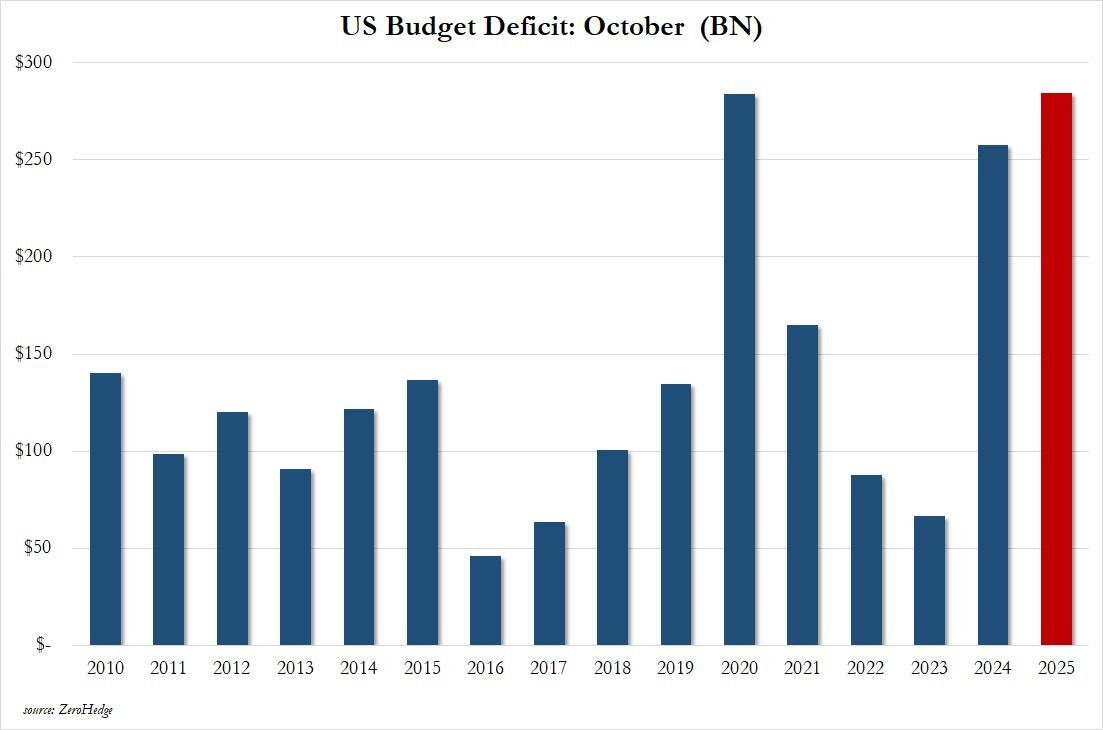

Either way, assuming the Fed wants to avoid more aggressive balance sheet action and hedge funds are mostly tapped out, such a move will likely become important sooner than later, as the October 2025 federal budget posted the largest October deficit in history despite a surge in tax receipts and tariff income.

Purists will argue that a chunk of the increased deficit was explained by shifting some payments originally meant for November into October, but on net the story over the last few months looks pretty clear.

In a relative afterthought for the federal budget, the Department of Government Efficiency (DOGE) officially shut down months ahead of its statutory expiration date, having saved at least tens of dollars.

The week was quieter on the whole international trade decoupling thing, though very notably, Chinese President Xi Jinping put in a call to President Trump regarding China’s relationship with Taiwan, which has become the world’s main source of leading edge semiconductors, and thus the key physical chokepoint in the race for AI dominance.

After the call, Trump reportedly asked his Japanese counterparts to stop harshing the vibe with their recent Taiwan rhetoric. Meanwhile, Taiwan’s President responded with a public rebuke of Xi and announced an increase to the country’s military budget.

Elsewhere in the international theater, the US officially designated Cartel de los Soles – which the Trump administration claims is run by Venezuelan President and color revolution candidate Nicolas Maduro – as a foreign terrorist organization, potentially another step toward regime change in an oil-rich region key to US dominance of the Western Hemisphere.

On the bitcoin front, as the orange coin rallied back to touch almost $94,000 after checking down to $80,000 last week, several noteworthy headlines hit the IBIT complex. First off, the latest 13F filings show that BlackRock boosted IBIT exposure by 14% in its internal Strategic Opportunities Fund during the third quarter.

Meanwhile, Nasdaq submitted an SEC filing to increase limits on outstanding IBIT options per account to 1 million from the current cutoff of 250,000, which would bring standards in line with some of the largest and most liquid ETF options markets.

Finally, JP Morgan announced a new IBIT derivative product offering holders structured payouts for specific bitcoin price paths over the next several years.

Regulatory Update

The government of Texas announced it has purchased $10 million of bitcoin, making the Lone Star State the first state in the US to officially acquire bitcoin.

A Spanish parliamentary coalition proposed raising the bitcoin capital gains tax rate to 47% while making it easier for the government to seize digital assets.

Noteworthy

Rumble – a video streaming platform that received a large strategic investment last year from Tether – launched beta testing for in-platform bitcoin and USDT tipping for content creators.

Travel

Bitcoin MENA, Dec 8-9

Nashville Energy & Mining Summit, Jan 2026