Ten31 Timestamp 928,714

All the macro dominoes continued to fall into place for what looks to be a strong fiscal and liquidity impulse in 2026 (as long as you put aside the steadily increasing probability of World War III). The latest US CPI reading came in much cooler than expected (which may or may not have been a result of some creative interpolation by BLS statisticians) while the delayed November payrolls data showed unemployment ticking up to its highest level since fall 2021. Both components should continue to further bias the Federal Reserve, which already signaled a slightly more pro-liquidity regime last week, toward an even more accommodative stance going into the new year, though we admittedly might need a good old-fashioned market puke to really get the ball rolling. Overseas, the Bank of Japan followed through on its long-expected latest rate hike, though interestingly did not commit to a clear path for further hikes and highlighted an expectation for continued accommodation through the fiscal channel, a more dovish outlook that sent the Yen back toward multi-decade lows vs the dollar. Less encouragingly, the US military continues to aggressively build its presence near Venezuela, which no doubt adds a new piece to the geopolitical chess board that could upend most consensus paths for next year.

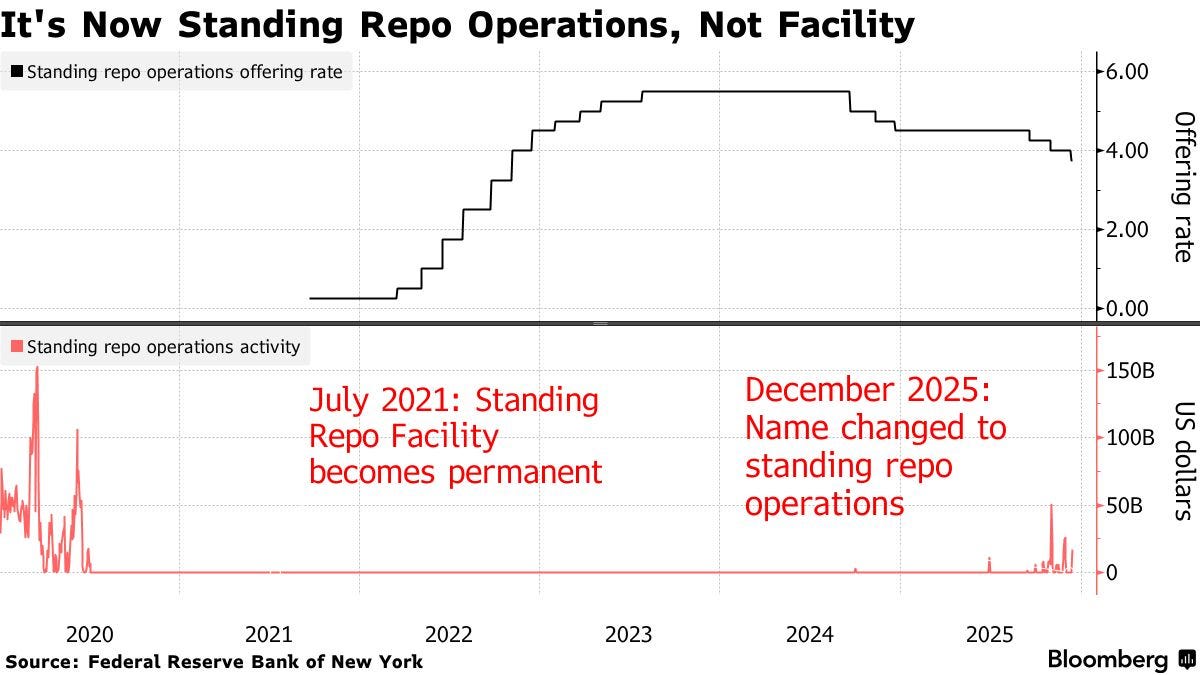

While the Fed was quietly renaming and expanding the Standing Repo Facility and President Trump was laying plans to Make Citgo Great Again, bitcoiners – true to typical form – coped with recent market chop by picking fights with each other on the issue of quantum computing. There is much to consider on this topic, and we’d like to resurface an article we published early this year that digs into these questions in some depth. More importantly, we’d highlight the recent progress on quantum research in bitcoin this year alone, which may add some nuance to the narrative that “bitcoin devs are asleep at the wheel” on this issue. Finally, we should note that – as with many domains of life where vocal advocates of a position insist Time Is Running Out to Do Something!TM – urgent and misguided action is often just as risky as inaction, particularly when considering a topic as complex as novel cryptographic security assumptions. For those interested in these topics, we strongly recommend digging in from first principles and deprioritizing hot takes from twitter-famous TA gurus.

Portfolio Company Spotlight

Fold is a leading financial services platform providing the most comprehensive bitcoin-denominated consumer rewards programs and a suite of services bridging bitcoin and traditional financial rails. Fold offers debit cards that accrue cash-back rewards in bitcoin that can be withdrawn to customer-controlled wallets, on top of unified checking and bitcoin custody accounts allowing users to seamlessly combine their USD and bitcoin activities to better preserve and grow their wealth. Fold has an exciting product pipeline – including a credit card set to be launched in the near term – and recently completed its public listing with 1,500 bitcoin on its balance sheet, giving the company one of the largest corporate bitcoin treasuries in the world.

As the world’s largest investor focused entirely on bitcoin, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem, and we expect 2025 to be the best year yet for both bitcoin and our portfolio. Visit ten31.xyz/invest to learn more and get in touch to discuss participating.

Selected Portfolio News

Giga announced the near-term ramp up of its new Houston factory:

Strike opened up lending to customers in California:

While expanding lending services in Montana:

Fold became the first publicly traded bitcoin financial services company operating in all 50 states in partnership with BitGo’s new federally chartered trust framework:

Fold also began rolling out its new credit card to a limited group of early users:

Media

Ten31 Managing Partner Marty Bent appeared on The Bitcoin Podcast to dig into a wide variety of topics related to bitcoin’s intersection with broader culture.

Market Updates

The latest US inflation data points came in much cooler than expected for November, as headline CPI clocked in at 2.7% vs consensus of 3.1%, while Core CPI was also lower than expected.

Some critics immediately (and perhaps fairly) argued that the Bureau of Labor Statistics was too, um, creative in its tabulations for the period. New York Fed President John Williams agreed the data were probably distorted by gaps in reporting, though not enough to fully explain the delta from consensus.

Recent Fed appointee Stephen Miran – who has argued for much of this year that elements of the CPI basket have tended to overstate actual inflation – took to Twitter for a victory lap on the news.

At the same time, delayed payrolls data for November showed better than expected job gains after a sharp downtick in October, though unemployment also rose to its highest level in over four years at 4.6%, which – in conjunction with lower wage growth – may bias the Fed further toward an easing stance.

The Fed Chair sweepstakes continued to generate fresh clickbait this week, as new reports suggested that the White House has received strong pushback to the appointment of frontrunner Kevin Hassett given his close relationship with President Trump.

Hassett, for his part, argued those meanies are being no fair while paying lip service to the importance of Fed independence.

Meanwhile, current Fed Governor Christopher Waller – who is much less of an outspoken inflation dove – underwent his formal interview for the position this week and allegedly left a “strong” impression on the President.

Whoever ends up winning the monetary Game of Thrones, the Fed certainly seems to be subtly shifting into a more accommodative posture, as the central bank quietly removed existing limits on use of the Standing Repo Facility – a mechanism meant to avoid liquidity spams in the increasingly important overnight repo market – while rebranding the tool to “standing repo operations” to decrease the stigma associated with tapping it.

Elsewhere in central banking alchemy, the Bank of Japan raised its benchmark interest rate to a 30-year high of 0.75% after several weeks telegraphing that decision. Notably, the Bank’s commentary around the rate hike suggested real interest rates are likely to remain “significantly negative” and that financial conditions should remain net accommodative to economic activity.

Even more notably, the Yen fell on the news, as investors responded to that commentary and the lack of clear guidance on the forward path of additional rate hikes from here.

Those in BOJ inner circles are also suggesting the Bank will begin selling off some of its huge ETF portfolio starting in January, though this process will likely be quite gradual and is expected to take decades to unwind.

Over in China, a growing number of economists are increasingly publicly agreeing with the (perhaps inadvertently) Trump-aligned view that the country needs to begin allowing its currency to appreciate.

Other reports out of China this week indicated that the country has finally been able to reverse engineer a working prototype for an EUV lithography machine, the lynchpin of leading-edge semiconductor development that is essentially controlled today by Dutch giant ASML. This could eventually have meaningful strategic implications in the US-China rivalry, though we’d suggest taking these reports with a decent grain of salt.

As geopolitical fault lines continue to form alongside the unraveling of the post-’71 “rules-based global order” built on US Treasuries, Russia’s central bank filed a lawsuit seeking $230 billion in damages from Belgian depository institution Euroclear related to 2022’s seizure of Russia’s sovereign US Treasury reserves.

Down south, in a possibly connected set of developments, the US has continued to aggressively build up its naval presence near Venezuela, with President Trump refusing to rule out a war as of Friday. Fox News has framed the buildup as related to narco-terrorism, while MSNBC insists it’s a naked imperialistic oil grab, but we tend to think neither narrative holds up well relative to other possible motivations.

Regulatory Update

Samourai Wallet Co-Founder Keonne Rodriguez reported to prison to begin his 5-year sentence this week. A few days prior, President Trump mentioned he will “look at” a pardon for the Samourai co-founders, and we encourage any readers interested in freedom-oriented open source software to sign and share the petition to that effect.

Four years after its notorious crackdown on bitcoin mining operations in the country, China has reportedly initiated new rounds of adversarial actions against remaining miners running as much as 2GW of capacity (a headline that once again calls into question the efficacy of prior “bans”).

The US Senate confirmed Michael Selig – who has previously spoken out about the dangers of regulation by enforcement – to lead the CFTC, which will be taking an increased role in the regulation of bitcoin infrastructure in the US.

Pro-bitcoin Wyoming Senator Cynthia Lummis – the sponsor of the BITCOIN Act to build a large strategic bitcoin reserve in the US – announced that she will not seek reelection in the upcoming mid-terms.

The Federal Reserve withdrew guidance from 2023 that previously limited smaller banks from engaging in “novel” business activities like digital asset-oriented financial services.

The SEC posted a new memo on digital asset custody options geared toward retail investors.

Noteworthy

Coinbase announced it is launching stock trading with up to 20x leverage on its platform, a development we would suggest is highly bearish for non-bitcoin “crypto,” whose main product-market fit since inception has been giving retail investors an ever-increasing menu of high-volatility tokens to trade.

Travel

Nashville Energy & Mining Summit, Jan 2026