The Global Capital Circuit

Bitcoin to Stablecoins, and Back Again

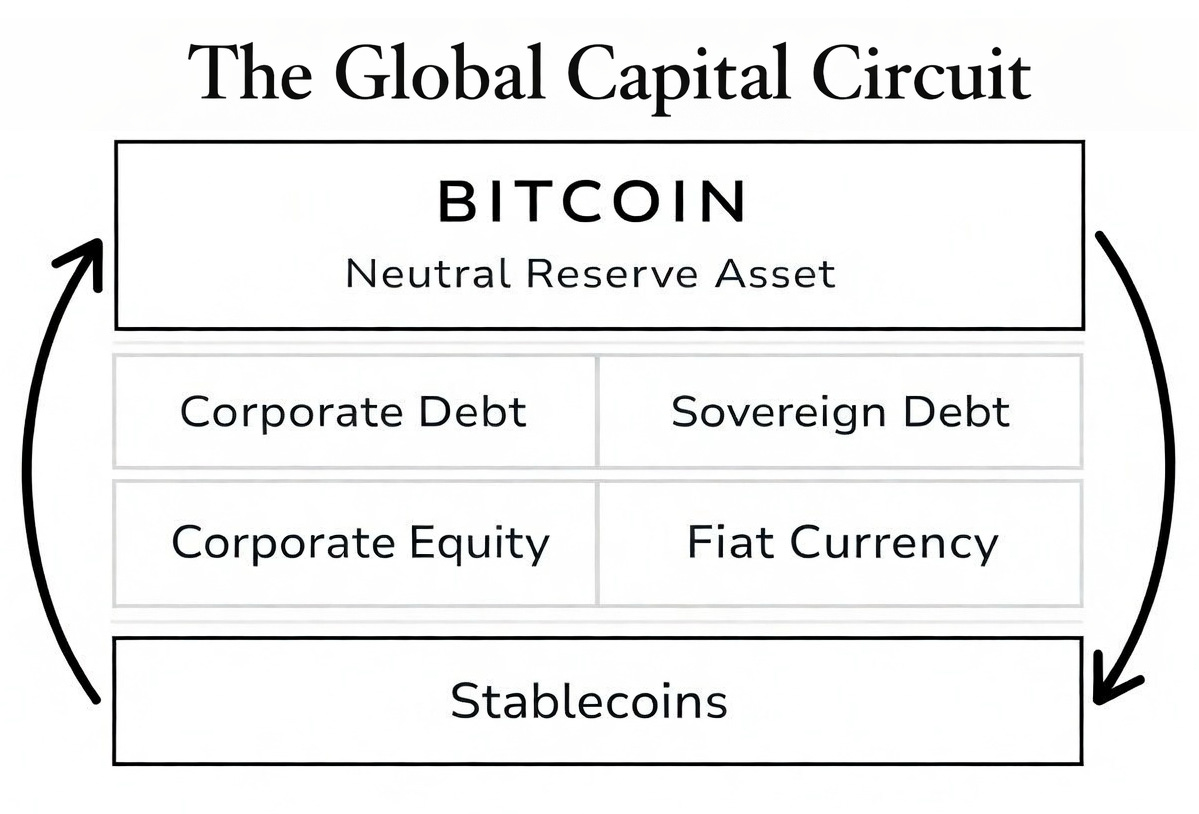

Capital has always operated within a stack of claims. A layered hierarchy where senior obligations enjoy contractual priority and junior layers bear the residual risk. In the digital era, a once more static ladder becomes a high-velocity circuit. Capital can now migrate from sovereign equity to neutral reserves and back again, driven by real-time market discipline. Historically, sovereign discipline relied on external anchors that evolved from a physical limit (gold) to a relative tether (U.S. Treasuries). Bitcoin breaks from this pattern. Its protocol-fixed finite supply operates within a decentralized, permissionless settlement network, creating the first truly digital neutral reserve asset. Bitcoin serves as a true hard cap on the global capital stack immune to alteration by any single authority as an asset without an issuer or superior claim. Market participants frequently dismiss bitcoin as speculation today because they are still calibrating to an asset whose core role is not to supplant fiat currencies, but to serve as the immutable benchmark against which all claims are measured in real time. And at this same moment, digital dollar mechanisms like stablecoins extend fiat liquidity into programmable, borderless networks, enabling participation in sovereign currency systems while maintaining a seamless, neutral exit into bitcoin. The mere existence of this new circuit fundamentally shifts incentives across the entire system.

We can dive into this perspective using some fundamental principles of accounting. Every public company operates within a capital structure that markets assess with precision. Equity forms the junior-most layer, bearing the highest risk as the residual interest that absorbs uncertainty and embodies management’s credibility. Debt sits above, as senior claims defined by contractual obligations, enjoying priority in repayment. A company’s equity functions as its currency. When executives over-leverage or dilute shares irresponsibly, the market does not lodge formal objections. The market simply adjusts prices. Capital flows toward more competently managed opportunities. This is not theoretical abstraction but the essential operation of markets, where credibility is hard-won and price discovery acts as the impartial regulator.

Applying this framework to nation-states reveals profound implications. A government’s capital structure mirrors the hierarchy already defined but with currency functioning as the junior-most equity tranche. This tranche absorbs the sovereign’s variable claims on fiscal responsibility, growth, and security, all of which are ultimately reflected in the market’s adjustment of purchasing power in the nominal unit. The government’s bonds are senior debt above, secured by its creditworthiness (order and taxing ability). But an inherent distortion persists in plain sight: sovereign debt is settled in sovereign currency. This flaw is essentially a Payment-In-Kind (PIK) system, whereby senior creditors can be serviced through the dilution of junior equity holders. When debt accumulation exceeds productivity gains, the facade of seniority crumbles. Creditors obtain full nominal repayment, but the real value of that repayment (purchasing power) erodes. Inflation is a byproduct serving as the veil for fundamental economic vulnerabilities.

History abounds with efforts to address this flaw. A golden path was paved as a durable safeguard providing a physical, auditable restraint on sovereign overreach. However, its very materiality proved its undoing: too cumbersome to handle and verify at scale, it demanded centralized custodians and thereby laid itself open to appropriation. When gold’s limitations clashed with state imperatives, authorities intervened decisively: a litany of examples, including the USA’s most recent via executive orders in 1933, the closure of the gold window in 1971, and finally the flood of ad-hoc liquidity facilities post 2008. The enduring lesson is that any constraint vulnerable to suspension in crises is illusory. Savers found themselves exposed, dependent on issuers’ restraint and the slow pace of bond market signals. Lagging indicators on what had already happened.

Bitcoin could impose accountability on sovereign mismanagement by functioning as a relentless real-time market enforcer, disciplining irresponsibility by allowing for instantaneous, global capital reallocation. Unlike traditional assets susceptible to regulatory capture or confiscation, bitcoin’s decentralized protocol remains impervious to unilateral intervention. Thereby ensuring poor governance (manifested in unchecked monetary policy, unsustainable fiscal deficits, or excessive household/personal indebtedness) triggers immediate and measurable consequences. Capital does not have to wait for diplomatic rebukes or credit rating downgrades. Debasement-driven value transfer has already begun to diffuse and crowd into traditional assets (stocks, real estate, and commodities) thereby concentrating and overexposing holders to geographic, political, and execution risks. Now, any allocator can instead migrate to bitcoin’s verifiable finite scarcity, evading the offending currency’s value erosion and compelling policymakers to confront their offenses before the breaking point. This mechanism can transmute bad behavior from a hidden liability into a public current affair, where individuals within markets, rather than bond vigilantes and regulatory mandates, impose corrective pressure, fostering a global ecosystem where credibility is not assumed but continuously earned.

Complementing bitcoin’s role as the capped neutral layer, stablecoins have emerged as novel digital mechanisms for onshoring eurodollars by digitizing and repatriating the vast offshore dollar liquidity that has long existed beyond the U.S.’s borders. Eurodollars (U.S. dollar-denominated deposits held in foreign banks) have enabled global dollar circulation outside of U.S. control, satisfying dollar demand and offering regulatory arbitrage while remaining in a fragmented and opaque market. Tokens pegged to USD, such as USDC or USDT, function as modern digital eurodollars: they enable seamless, borderless transfers of dollar-denominated value from any digital client. These stablecoin issuers effectively repatriate offshore eurodollar reserves into programmable, digital pipes ring-fenced within the purview of U.S. Treasury-backed regulation, enabling the further expansion of U.S. debt. Without physical branches, vaults, or heavy legacy overhead, these issuers slash distribution costs to near-zero, providing channels for billions in remittances, trade settlements, and savings ability for global markets. This broadens voluntary access to the U.S.’s equity tranche, accelerates global economic integration, and can reinforce U.S. dollar hegemony. Hegemony not through imperial imposition, but by making offshore dollar liquidity more compliant, transparent, and demand-generating for U.S. debt in a digital era.

Bitcoin sits atop the stack and counterweights with pure choice unlike manipulable debt instruments that sovereigns can endlessly issue, refinance, or sweeten with flexible incentives. This unrelenting competitive pressure of choice produces a negative feedback loop that can induce an equilibrium. Sovereigns and corporations must continually enhance their debt and equity offerings through superior yields, geopolitical protections, exclusive trade deals, regulatory favors, or other dynamic perks to stop capital from migrating to an elegantly simple alternative. A simple solution creating a market, not a one-way-function as transacting in bitcoin offers none of the active externalities that dominant powers deploy through alliances, military umbrellas, or market privileges. Nevertheless, its open-source foundation, simple design, unique balance of incentives, and lack of any prior or future claims keep it flexible. Proven market demand can spawn integrations such as long-term dual-collateral loans and BitBonds that bridge bitcoin with real-world assets and governments, affording competition while isolating geographical, political, or executive risks. These innovations, along with yield mechanisms and governance tools, can be added without ever diluting bitcoin’s finite scarcity or resistance to unilateral control.

In this adjusted framework we see bitcoin completing the transformation from static electricity to electrical current. Bitcoin serves as the ultimate adjudicator of trust and scarce value, while stablecoins operate as the scalable pipelines for sovereign currency distribution. Together they form a single, self-correcting system: stablecoins broaden access and lower friction, while bitcoin’s fixed scarcity ensures that no issuer can escape market discipline indefinitely. They compel sovereigns to compete on genuine merit rather than coercion or monopoly, dismantling entrenched inefficiencies and unlocking unprecedented potential. As credibility trends toward becoming currency, markets will not simply reflect realities; they will shape them, granting innovation and fiscal prudence a privileged seat in the sovereign arena.

It would be great to get your analysis on efforts within the bitcoin dev community - individuals and organizations- who are working to ensure that bitcoin becomes the default ‘currency’ between AI agents…