The Reality Distortion Field: Ten31 Timestamp 937,699

There's no fishing in the Rubicon

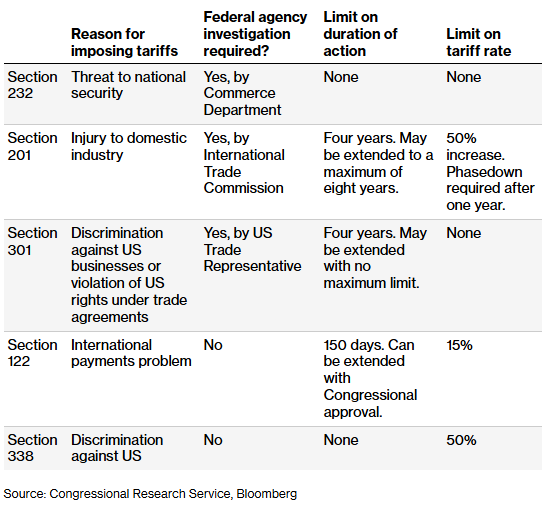

Anyone who’s read a Steve Jobs biography or watched one of his many biopics probably remembers the famous concept of the “Reality Distortion Field” (RDF), whereby the Apple founder’s charisma (or abusive personality, depending on your source) would lead those in his orbit to ignore conventional assumptions about real-world constraints and push through to complete a task anyone else would dismiss as impossible. We’d argue most people have their own RDF, but it typically runs in the opposite direction – a kind of magical thinking that bends perception of reality to flatter preconceived notions – and we think this week showed a few examples of the RDF’s influence on legacy institutions, which seem to be under the impression this is still 1992. Most notably, the Supreme Court struck down the Trump administration’s unilaterally imposed “emergency” tariffs, essentially the lynchpin of the White House’s entire economic policy agenda, prompting many RDF-plagued opponents of these tariffs to immediately celebrate Trump’s apparent defeat. However, the President quickly made clear that the tariffs will be imposed in some other way, and it indeed looks like he has all the legal firepower he needs to at least keep the matter alive for years to come, largely thanks to a half-century of both parties enthusiastically vesting ever more power in an increasingly unaccountable administrative state. The institutional RDF would suggest this is the end of the line for tariffs, but we think the past year clearly shows the die has been cast on the global economic reordering, and – for better or worse – we’re not reverting to pre-Liberation Day norms just because of procedural disagreements on which statute technically provides the necessary window dressing.

The institutional RDF also seemed to be on display at the Federal Reserve this week, as the minutes from the latest FOMC meeting continued to point to a divided Fed still dithering about the minutiae of how it messages the speed of rate cuts, with some officials even arguing for forward guidance toward the potential for rate hikes. While Fed officials wring their hands and prudently rearrange deck chairs, the Treasury Department appears to already be in the process of writing the next chapter, as Treasury’s latest quarterly refunding documents clearly assume an increasingly accommodative Fed and greater coordination with the central bank to manage the government’s ballooning funding needs. At the end of the day, when a sovereign – particularly the most powerful sovereign in the world – feels itself to be existentially threatened by a rival or needs dependable funding for its strategic priorities, history suggests that no amount of institutional RDF will get in its way. We’re not taking a particular view one way or the other on the various goals of the administration, but we do see the decades-old assumptions of Wall Street and K Street (clean separation of powers, effective checks and balances, Fed independence) to be increasingly at odds with the realities of the present moment, and we’d argue the breakdown of those frameworks has significant implications for both neutral reserve assets and, more importantly, technologies like bitcoin that can provide a permissionless bulwark for individual liberties in a time of rapidly shifting norms.

Selected Portfolio News

Strike launched Agent Playground, an open source reference template for portable AI agent environments:

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Media

Ten31 Managing Partner Marty Bent joined Bram Kanstein and Onramp to discuss the latest in bitcoin, AI, regulation, and more.

Market Updates

Though the headline dropped in the middle of a Friday, the biggest news of the week was the Supreme Court’s long-awaited decision on President Donald Trump’s sweeping tariffs. Despite a bench of justices optically tilted in Trump’s favor, the high court ruled against the current incarnation of the tariffs in a 6-3 decision.

Taken at face value, this decision undermines one of the key components of the White House’s economic agenda; however, President Trump quickly emphasized that his team has many other fallback options in place and suggested he may roll out “even stronger” tariffs in the near term.

While the Supreme Court threw a wrench into the White House’s trade agenda and the President vowed to push forward, the latest trade data released this week showed a significant jump in the US’s trade deficit in December, back to levels that look much closer to the prior few yeras. Overall, the 2025 trade deficit came in basically in line with 2024, though a variety of early-year pull-forwards and the impact of gold flows complicate the picture.

Potentially complicating another important pillar of the President’s platform, the minutes from the latest FOMC meeting continued to point to a divided Fed and an uncertain path for further benchmark rate cuts from here, with some officials considering new “two-sided language” to leave open the possibility of rate hikes.

That said, as part of its Quarterly Refunding Announcement, the Treasury Department released its latest TBAC presentation, which explicitly highlights a strategy of using the Fed’s new Reserve Management Purchase program to shift more debt issuance toward short-end bills and reduce incremental supply of duration.

The data also seem to assume that, rather than being just a temporary measure used to stabilize bank reserves, RMP purchases will continue at their current levels (close to $500bn annually; see page 20) indefinitely. While not yet directly comparable to QE, these data points hint at a continuing shift to subordination of independent monetary policy to the fiscal needs of the government.

The Fed minutes also highlighted some general concerns with “vulnerabilities” in the private credit complex, which potentially got some additional validation this week when large alternative asset manager Blue Owl Capital permanently halted redemptions on one of its funds targeted at retail investors.

Blue Owl was able to sell off $1.4 billion in assets at nearly 100 cents on the dollar to meet withdrawal requests, so it’s too soon to say this is The Big OneTM, but it bears monitoring given ongoing fragility in parts of the illiquid credit complex, highlighted elsewhere this week by a sharp uptick in distressed loans linked to software companies.

On a similar note, the Wall Street Journal ran a feature on commercial real estate lenders increasingly moving into the foreclosure stage of non-performing loans rather than playing the “extend and pretend” game any longer, as delinquencies in many verticals of this market continue to increase to new multi-decade highs. Notably, less than half of the $100 billion of securitized CRE loans coming due this year are expected to make repayment at maturity (down from 75-80% in 2024 / 25).

Fed Governor Michelle Bowman introduced a new proposal that would reduce bank capital requirements for originating mortgages, the latest sign of bank regulators’ desire to incentivize more credit creation out of the traditional banking system.

Overseas, the US military continued to amass considerable military assets in the vicinity of Iran, with Vice President JD Vance indicating that Iran has yet to address key American demands.

For his part, President Trump suggested he’s considering a “limited strike” against the country. He also indicated he will move forward with new UAP disclosure, which pretty much seals the deal that we’re going to war.

Potentially buried under other headlines this week was the GDP report for Q4, which showed growth of only 1.4%, well below consensus estimates for 2.5% and juuuust a bit outside of the administration’s near-term target of 10-20%. A chunk of this gap was driven by the quarter’s lengthy government shutdown, though the Commerce Department suggested the actual net impact “could not be quantified.”

As 13F season ramps up again, a few notable updates have started to trickle out. Most significantly, two major Abu Dhabi sovereign wealth funds materially increased their IBIT positions during the fourth quarter even as bitcoin experienced a significant drawdown.

A representative from one of the funds reiterated to Bloomberg that they view bitcoin as a “store of value comparable to gold” and a part of the fund’s long-term strategy. On the flipside, Harvard’s endowment trimmed its IBIT position during the quarter, though it remains the university’s largest publicly reported liquid position.

While bitcoin’s price has yet to recover from its February selloff, bitcoin mining network hashrate has experienced an explosive V-shaped recovery over the past few weeks, climbing firmly above 1 ZH/s again and erasing most of the YTD decline.

Regulatory Update

The Trump administration issued a March 1st deadline for a CLARITY Act compromise between the banking and digital assets industries. White House Digital Assets Advisor Patrick Witt suggested talks on the stalled legislation are progressing well and he expects to meet this deadline.

Noteworthy

River published some preview snippets of the latest refresh of its Lightning Network research, which includes some pretty impressive statistics on the steady progress of bitcoin’s main second layer.

Longtime bitcoin developer Matt Corallo highlighted some interesting conservative proposals for preparing bitcoin against future advances in quantum computing without major architectural overhauls today.

CME announced it plans to begin offering 24/7 futures trading for digital assets beginning in May of this year.

The Wall Street Journal published a feature on various countries around the world increasingly pushing to add aggressive KYC to social media platforms in the name of protecting the kids.

{kind=link}

Travel

OPNext, New York, Apr 16

Bitcoin 2026, Las Vegas, Apr 27-29