A Print By Any Other Name: Ten31 Timestamp 934,501

Our long national Fed Chair sweepstakes is over

After months of a Will They / Won’t They soap opera breathlessly covered by the financial press, President Trump finally announced Kevin Warsh as his pick to replace long-suffering Fed Chairman Jerome Powell. Warsh has spent the last year in a hot / cold relationship with prediction markets as the presumptive nominee, but his selection for the seat sent the dollar higher, bitcoin lower, and an extremely overheated precious metals complex spiraling into a shocking drawdown on Friday, with gold down over 10% and silver down as much as 32% intraday. Consensus seemed to view the pick as relatively hawkish given Warsh’s years of consternation about inflation even during the depths of the Great Financial Crisis, as well as his recent commentary about hoping to match a more accommodative Fed Funds stance with a more restrictive posture on the Fed balance sheet, which Warsh ostensibly thinks should shrink. Whether that hawkish read on the new appointee’s framework is correct (we suspect that it may be more bark than bite given his close family ties to the President and the administration’s clear need for no obstructions to its high growth agenda) and whether or not Warsh actually gets confirmed (we suspect this may be harder than Trump hopes given the recent DOJ probe into Chair Powell), we are highly skeptical that such a strategy is actually workable by Mr. Warsh or anyone else.

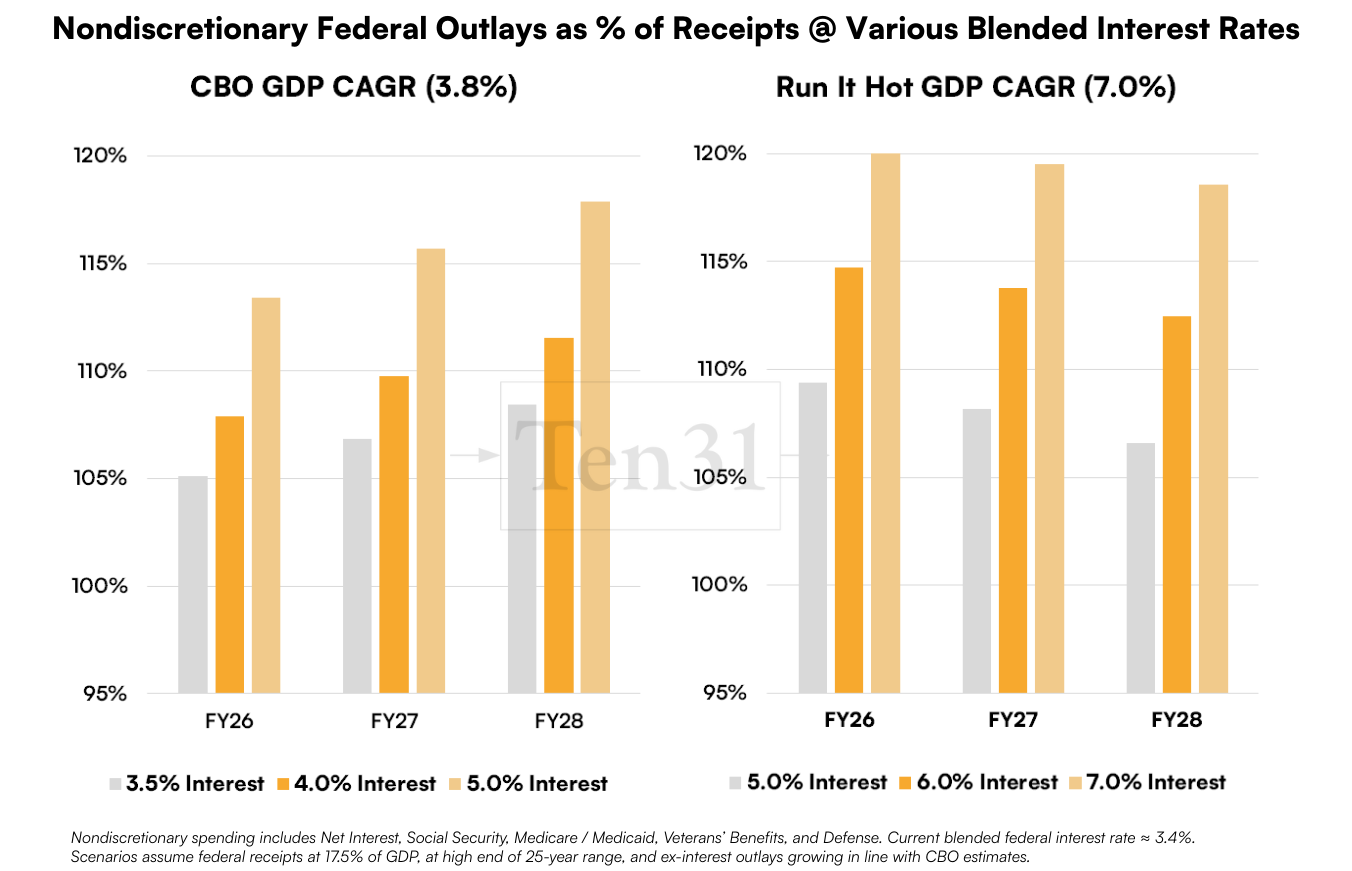

It’s a reasonable soundbite to argue for lower rates and a lower Fed balance sheet, and we sympathize with the desire to “let Main Street have its turn.” However, the fiscal reality the US has created over the past 50 years makes that extremely difficult: with nondiscretionary federal spending already right around 100% of annual tax receipts, the game doesn’t work if someone is not ready to be a price-inelastic buyer of marginal new Treasury issuance. Even if the new Fed Chair can successfully dictate the Fed Funds Rate materially lower, longer duration rates may or may not follow if left unchecked, and given all the forces at play – a “run it hot” agenda which, even if successful, should tend to bias long-end rates higher, with or without a meaningful inflationary impulse; a massive boost to major government line items like defense spending; and an administration whose trade policies are extremely likely to drive foreign capital repatriation on the margin – it’s not clear why there should be material downward bias on longer maturities. At current yields, the blended effective interest rate on outstanding US debt is already trending higher over the next few years as pre-2022 ZIRP issuance continues to mature, so if the long end just doesn’t respond to the path of Fed Funds (or worse, drifts higher per the factors just discussed) the US will quickly move into scenarios like the charts above where nondiscretionary spending blows out relative to tax receipts – and that’s before even considering the possibility that Clawdbot takes everyone’s job and kicks unemployment benefits and stimmy checks into high gear. Without an accommodative balance sheet somewhere in the system to exert downward pressure on realized federal interest expense, it strikes us as highly questionable that this plane will land as intended.

Of course, we suspect that the Warsh camp – including Scott Bessent, his fellow Druckenmiller protégé – all generally know this and that Warsh would not have ultimately gotten the nod if he were not prepared to play ball to keep the wheels from falling off. Furthermore, it’s possible that the commercial banking system may be able to step into what has been the Fed’s role over the past several decades and become the Treasury buyer of first and last resort, a path that regulators have clearly been trying to shore up with much less restrictive bank balance sheet rules. But whatever the ultimate source of absorption, the math dictates pretty simply that – absent an AI productivity boom that proceeds at precisely the right pace – the monetary base will need to expand to maintain the stability of the Treasury market, government finances, and ultimately US hegemony. While the mainstream press runs with the popular balance sheet hawk narrative, we encourage readers to keep their eyes on the system’s hard constraints and to not be surprised when the appetite for balance sheet rectitude winds up in the same heap as DOGE.

Selected Portfolio News

Strike reduced minimums for bitcoin-backed loan users in Iowa:

Start9 began rolling out the latest models of its Server One product:

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Media

Giga Energy published a new piece digging into bitcoin mining’s relationship to utility demand response programs.

Market Updates

Following months of Polymarket liquidations and Truth Social browbeating, President Trump finally announced Kevin Warsh as his pick to replace Fed Chairman Jerome “Too Late” Powell.

The market reaction may not have been what the President was looking for, as stocks slid, bitcoin fell, and precious metals got annihilated – with gold and silver both putting up one of their worst days in history – on the consensus view that Warsh is a more hawkish choice than other frontrunners like Rick Rieder and Kevin Hassett.

Indeed, Warsh had a long track record of concern about inflation during the nadir of the Great Financial Crisis – even as unemployment pushed double digits – and he has more recently advocated for reducing the size of the Fed balance sheet alongside a lower Fed Funds Rate.

Notably, though, the new Fed Chair appointee has longstanding ties to the Trump family, which may or may not come into play as the White House increasingly looks to take a stronger hand in Fed policy.

Perhaps even more noteworthy was an interview with Stanley Druckenmiller just after the announcement, where the famed hedge fund manager suggested that Warsh – who has worked closely with Druckenmiller in recent years – “is not a permanent policy hawk” and is “very open minded” to the approach of Plunge Protection Team leader Alan Greenspan.

Finally, Druckenmiller noted he’s excited to see Warsh partner with Treasury Secretary Scott Bessent (another of his close associates) to build a new “accord between the Fed and the Treasury.” We feel like we’ve heard that somewhere before.

For his part, Bessent commented just before the announcement that he encourages the next Fed Chair to be open minded about accommodative policy given “what’s coming over the next few months,” which Bessent elsewhere said he believes will be a “non-inflationary boom.”

Based on all the fiscal realities at play – including a tax season set to increase refunds by more than $100 billion Y/Y – we expect this kind of open-mindedness will likely be very necessary soon, particularly if President Trump wants to “drive up home prices” to keep current homeowners wealthy, as he suggested in a press conference this week (we will leave readers to do their own calculations on how this helps to address the “national housing emergency”).

As another sign of the changing temperature at the Eccles Building, recent Fed appointee Stephen Miran – whose term technically expires this week but who can stay on until a replacement is approved – chimed in to reiterate that he believes unemployment is still “about half a point too high.”

That said, the latest PPI reading for January came in well above consensus at 3% and may complicate the narrative around aggressive easing, at least until the administration just chooses to bite the bullet on prices.

All the consternation and speculation may still be premature, though, as GOP Senator Thom Tillis quickly reiterated that he will not confirm Warsh or any other nominee until the recent DOJ probe into Jerome Powell is settled.

For what it’s worth – which may not be much – Warsh has previously said that bitcoin is the “new gold” for people under 40 and praised elements of bitcoin’s design.

You could be forgiven for forgetting that there was other news out of the Fed this week, but the latest FOMC meeting on Wednesday saw the central bank hold rates steady as expected, though the more noteworthy update was the committee removing language about a weakening labor market from its statement.

The President responded predictably on Truth Social, but his latest tirade threw out an interesting nugget about Powell endangering “national security” by not lowering rates. As far as we can tell, this was the first time Trump has directly suggested this, and we think it may be an interesting signpost for how the new Fed-Treasury nexus will operate.

While the White House continues to work on remaking the Fed, Congress has once again found itself in shutdown mode as Democrats looked to block DHS funding in the latest appropriations package amid high tensions over the President’s immigration policy.

The government officially entered a partial shutdown on Saturday morning, though as of this writing there appears to be decent momentum toward a near-term resolution.

Elsewhere in monetary plumbing, news emerged over last weekend that the New York Fed had conducted a rate check on the USDJPY cross as the Yen weakened aggressively this month, often seen as a precursor to intervention and likely the driver for the major gap-up in the Yen last Friday. However, Secretary Bessent dismissed the rumors, noting that the US is “absolutely not intervening” in the Yen market.

Lost in the shuffle of the week were a couple other overseas headlines. First off, the Trump administration signed an executive order declaring a “national emergency” over actions taken by the Cuban government, presumably a precursor to the next regime change efforts in the US’s backyard. Similarly, a local court voided a Chinese company’s contract to operate ports in the Panama Canal, potentially paving the way for more US influence in the region.

Amid the wild week, precious metals continued their unprecedented rollercoaster, with gold and silver both ripping up to historic new highs while also getting hit with massive downside volatility. Multiple times this week, the two metals lost bitcoin’s entire market cap over just a few hours, with silver dropping over 30% on Friday.

Asset management giant BlackRock filed an S1 for a new income-oriented bitcoin ETF targeting payouts based on a covered call strategy. Elsewhere in traditional finance, Morgan Stanley officially created a new role dedicated to digital asset strategy.

Bitcoin’s network hashrate – which has climbed parabolically over the last two years almost regardless of price action – fell off sharply this week, likely the result of massive winter storms that blew through the US, triggering demand response shutdowns in many grid systems. We note for any concerned readers that this is exactly the kind of use case that makes bitcoin so unique and powerful as a highly flexible, energy-linked network.

Regulatory Update

Blockchain analysts alleged that a family member of the company hired by the US Marshals to secure the agency’s seized bitcoin holdings stole $40 million from the account this week.

The leaders of the SEC and CFTC joined the Wall Street Journal for a joint interview where they indicated plans to craft their own rules and guidelines for splitting authority in the absence of a more formal partition from the long-awaited and again-delayed “market structure bill.”

Noteworthy

A large and growing group of autonomous Clawdbot instances initiated their own bots-only social forum this week, and shortly thereafter began discussing how to leverage bitcoin and Nostr, an interesting validation of our long-held thesis about how AI agents would likely interact with each other over time.

OpenSats published its annual report highlighting over $30 million of cumulative contributions to open source developers around the world.

Prominent international crypto exchange Binance announced it will convert its $1 billion emergency fund into bitcoin.

Travel

Bitcoin Investor Week, Feb 9-13

Bitcoin 2026, Apr 27-29