Mr. Warsh, I Don't Feel So Good: Ten31 Timestamp 949,671

There are bonds in the stocks

This rally has everything: transitory inflation, new all-time highs for Cisco, permabears capitulating into semis at the pico-top, regime change at the Fed. Another week of wildly bullish moves across the stock market and AI complex was capped by a violent selloff on Friday, as investors everywhere googled “Thucydides Trap” after the latest Trump-Xi meeting and didn’t like what they saw in the top hits (or in the “@grok is this true” follow up). The latest headline inflation data gave the market even more cause for concern, with both CPI and especially wholesale price inflation coming in above estimates and pushing more Fed rate cuts firmly out of consensus for at least the rest of this year, which is an interesting setup considering that Rate Dove Extraordinaire Kevin Warsh officially cleared Congressional confirmation to take up the helm as next Chairman of the Federal Reserve. President Trump’s totally independent and impartial pick to lead the central bank has long emphasized his view of an oncoming productivity boom that will free up capacity for lower benchmark interest rates, and as monetary policy becomes a more overt tool of statecraft, we’re not convinced that a few hairy data points are going to be enough to derail the pro-growth, pro-reshoring agenda, particularly given the precarious state of the US federal interest burden, which now demands some combination of suppressed rates, short-end funding, captive buyers from friendly trade surplus countries, and a ripping GDP denominator to remain serviceable. To be sure, the long end may try to revolt – and it certainly got a little frisky this week – but longtime readers may recall that when push comes to shove, we have tools for that. As a popular saying goes, there are bonds in the stocks stonks, which is to say that higher / lower rates on benchmark debt flow through to lower / higher long-duration discounted values of cash flows to equity holders (read: stock prices), and those values can only be allowed to fall so far before the game is fundamentally imperiled (higher rates / lower stock prices → lower capital gains tax receipts and high-end consumer spending / less headroom for hyperscaler capex → higher sovereign debt yields / lower forward GDP growth and leverage against China → rinse / repeat). If we were still in the world of monetary technocrats studiously applying the (dubious) wisdom of the Phillips Curve, we might have more sympathy for this week’s market reaction, but the lesson of the past 6 years and especially the last 12 months is that we are definitively not in Kansas anymore, and we think that many investors still have yet to fully catch up to that reality.

{kind=link}

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Media

Strike Founder and CEO Jack Mallers appeared on What Bitcoin Did to discuss his long term vision for Strike, Twenty One, and bitcoin’s ongoing integration into traditional capital markets.

Giga Energy Co-Founder and CEO Matt Lohstroh appeared on popular tech and finance show TBPN to dig into the company’s explosive, capital-efficient growth as a leading HPC infrastructure provider.

Fold Founder and CEO Will Reeves participated in a panel on bitcoin financial services at this year’s Bitcoin Conference in Las Vegas.

AnchorWatch Co-Founder and COO Becca Rubenfeld joined the Galaxy Brains show to discuss the evolving custody landscape and Becca’s personal story.

Market Updates

After more than a month of playing footsie on a potential deal with Iran, President Trump kicked off the week by lamenting that the fragile ceasefire is on “major life support” after rejecting Iran’s latest proposal to end hostilities.

With Iranian texts left on read, Trump crossed the Pacific for a pivotally timed two-day summit with Chinese President Xi Jinping. Trump packed light for the trip, bringing only a few dozen of America’s most significant business leaders (whose collective market cap is roughly equivalent to the entirety of the Chinese stock market) along for the ride.

The two aspiring Great Men of History discussed avoiding the Thucydides Trap (which may or may not actually be a thing), whether Trump would defend Taiwan (but he’s not telling), and the potential for China to “open wider” to business with more American companies (potentially like a crocodile opens wider for its dinner).

With oil still hovering firmly above $100, Treasury Secretary Scott Bessent suggested China is working behind the scenes to lean on Iran for a resolution in the Strait of Hormuz. All parties involved in this week’s talks reportedly agreed that they want to see normal oil flows restored as soon as possible, including no future where Iran extracts tolls from ships in the waterway.

The situation has continued to pressure China domestically, as the country’s independent oil refiners (long-time key customers of Iranian oil) slashed their output by more than 50% in April on the back of depressed margins. In the meantime, China has agreed to buy more oil from the US.

Also of note from the week’s talks were comments from US Trade Rep Jamieson Greer, who indicated that exports of rare earth minerals from China have returned to “better levels” over the last few months.

Back on the homefront, the guns continued to impinge on the butter, as the latest CPI reading for April came in at 3.8% (including 2.8% ex food and energy), good for the highest level in a few years. The latest PPI also printed at +6% annually, its highest reading since 2022.

The resurgent inflationary pressure collectively ignited fears that the Federal Reserve’s cutting cycle may now be at risk, with the market increasingly pricing in near-term rate hikes.

Secretary Bessent was unconcerned, noting that he forecasts “substantial disinflation” ahead after just “one or two more” hot prints. You might even say it’s…transitory?

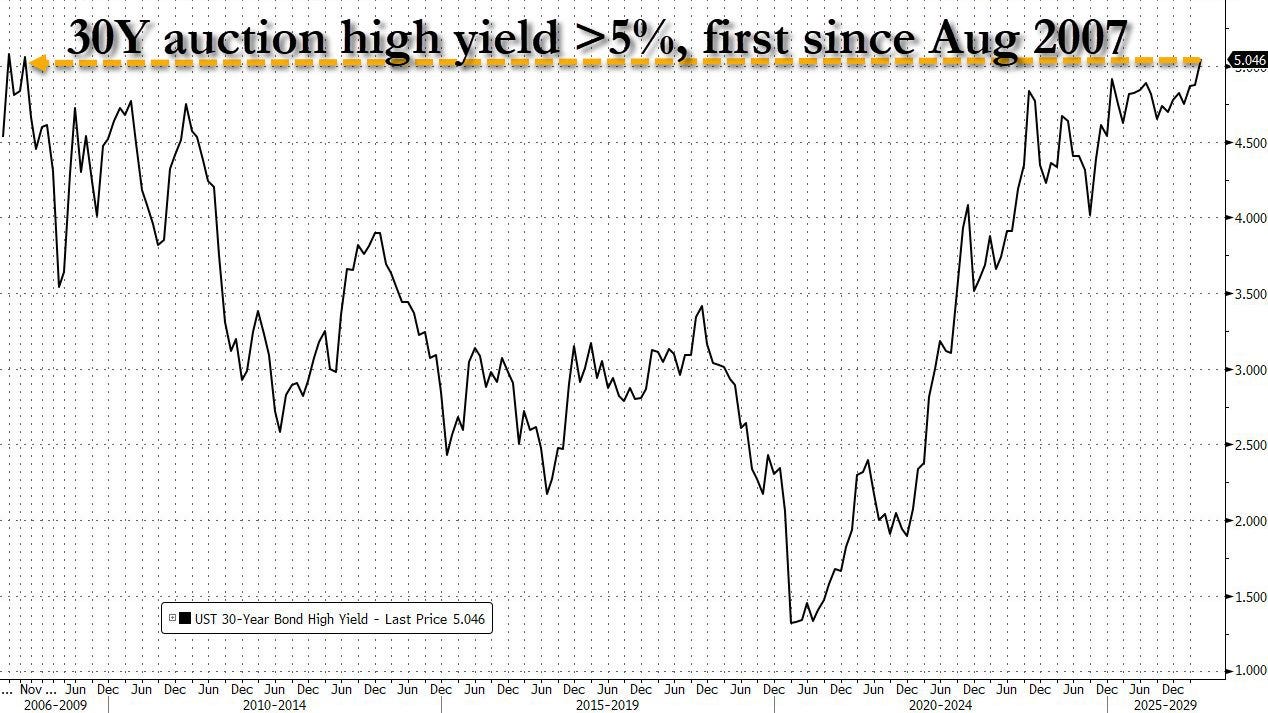

The bond market was less convinced, as the 10-year Treasury yield convincingly broke 4.5% – a level which seems to have historically been a line in the sand for the Trump administration – for the first time since the Tariff Tantrum, closing the week above 4.6% while the 30-year reached a new post-Financial Crisis high.

All that said, so did equities (before giving some back on Friday).

Overseas bond markets got even more frisky on the week, with yields on JGBs, Bunds, Gilts, OATs, and probably every other overwrought foreign bond nickname you can think of all entering the dreaded banana zone.

Against the intermittently squirrely bond market backdrop, the Treasury Borrowing Advisory Committee introduced a proposal for the US Treasury to, for the first time, begin acting as a lender into the Treasury repo market as a means of using some of the TGA’s excess cash to shore up repo market volatility. For those keeping score at home, this would mean the Treasury may begin lending against its own debt in the name of market stability.

Amid a growing bond market kerfuffle, Kevin Warsh was officially confirmed to the role of Fed Chairman this week. We’ll wait to see if the SOFR shorts are right that Warsh will pivot on a dime to raising rates and allowing the bond vigilantes to take the day, but we’ll just say we have our doubts.

The sovereign debt volatility probably won’t improve the backdrop for private credit, which saw more negative headlines this week as KKR’s largest private credit fund held by individual investors reported a $560 million loss in Q1, roughly ~10% of fund NAV. The company said it will invest another $300 million into the fund to boost confidence as default rates increased over 250bps to 8.1% in the quarter.

Elsewhere, Apollo is reportedly in talks to sell off MidCap Financial, its $3 billion publicly listed private credit fund, which also saw default rates jump last quarter.

While the market got wobbly late in the week as bond yields ripped, the latest Empire State Manufacturing Index for May surged M/M to a four-year high, the latest data point highlighting accelerating industrial activity in the US.

Overseas, the memory market, an increasingly constrained chokepoint for the AI race that has become the main de facto driver of GDP and national security, faced another potentially massive kink this week as thousands of workers at Samsung threatened to strike over compensation disagreements. A top South Korean policymaker suggested that companies like Samsung – which has swiftly become one of the most valuable in the world – should pay everyone in the country a “citizen dividend” from their recent windfall.

While we haven’t heard much about US territorial expansion recently, BBC reported this week that the US has been in talks to open three new bases in Greenland, all of which would be formally considered sovereign territory. At the same time, President Trump suggested he is “seriously considering” making Venezuela the 51st state.

Regulatory Update

After an apparent compromise was reached last week on the long-delayed CLARITY Act, the American Bankers Association sent a letter to all banks urging opposition to the bill due to the law’s treatment of stablecoin yield.

Notably, the latest version of the bill maintains much of the core language from the Blockchain Regulatory Certainty Act to limit liability for developers of noncustodial software, though the draft also contains notably vague terms that could still be used to prosecute developers under money transmission laws.

Despite those concerns, police unions and politicians have publicly argued that the legislation does not go far enough in applying legal liability to developers (though we can surmise from contextual clues that many of these commentators are, um, insufficiently informed about small matters such as how bitcoin actually works).

Regardless, the bill successfully made it out of committee this week, much to the chagrin of certain tribal elders.

The Financial Services Committee introduced the Price Stability Act, which would remove “maximum employment” from the Fed’s dual mandate (which they’re forgetting is actually a triple mandate, the third leg of which – moderate long-term interest rates – is arguably the most critical at the moment).

President Trump and his associated family entities disclosed purchases of Coinbase, Strategy, and MARA during the first quarter.

Noteworthy

Major public bitcoin miner MARA signaled support for BIP-54, a generally popular bitcoin improvement proposal colloquially known as the “Great Consensus Cleanup,” which addresses a variety of small but important long-running vulnerabilities to bitcoin.

Strategy’s STRC preferred stock reached a record for daily volume this week, driving purchases likely north of 15,000 bitcoin through Friday.

So many good one liners that are consistently put in these writing which always get me to crack smile, haha. My favorite one for this piece and oh so true, "we are definitively not in Kansas anymore."

I miss Toto, looking forward to making it over the rainbow!

Well written- thank you!