The Empire Strikes Back: Ten31 Timestamp 945,622

You can't blockade me, I'm blockading you

It turns out having the biggest stick still matters. After weeks of many analysts tap-dancing on the apparent grave of US military hegemony as traffic through the Strait of Hormuz remained disrupted by Iranian attacks, the US took the dramatic step of moving a group of aircraft carriers and destroyers into position to blockade Iran’s ports, immediately disrupting millions of barrels per day in oil and potentially putting the war-torn and export-dependent country in dire straits. It remains to be seen how well this will work in the long run, and whether the downstream impacts of disruptions in the Gulf will cause the US to blink before Iran and its Eastern proxies (though newsflow for most of the week clearly favored one more than the other), but we think it’s fair to say that the TACO meme has officially grown stale. Many commentators have spent the past couple decades highlighting, with good reason, how the US is showing all the signs of a decaying Great Power – and the decadent AI slop posted by its Commander in Chief may be particularly strong evidence for this thesis – but we think the events of the past few months, and especially this week, speak more to the US’s full embrace of the imperial phase of the Great Power cycle. We don’t celebrate this trend by any means, but it’s increasingly tough to deny all the ways the US is consolidating leverage and carving out a hard sphere of influence around the world (a large collection of which are documented below).

While we moonlight as armchair geopolitical Situation Monitors, we are humble bitcoin stackers at heart, and we think the implications of these trends remain underappreciated for bitcoin. The machinations of this administration are far from guaranteed to work, but what if they do? What if the US is able to – through influence, force, spycraft, financial incentives, maritime controls, Artful Deals, or all of the above – establish and protect a firm sphere of dollar- and Treasury-friendly partners among the GCC, Japan, Korea, and commodity-rich South American countries? What if it’s able to leverage its position as the world’s largest consumer, net energy exporter, and operator of (for now) the world’s most important financial rails to secure favorable deals for key resources? What if it succeeds in using a captive audience of onside trade surplus countries (plus some backdoor Fed support) to stabilize Treasury yields long enough to pursue reshoring of key industries? What would the headroom for issuance of dollar claims created by that framework imply for the dollar-denominated price of the globally available, politically neutral, scarcest asset in human history? What if the dollar doesn’t need to collapse for owning bitcoin to make sense?

Selected Portfolio News

Strike’s line of credit product now supports interest rollovers:

And Strike opened up term loans and BLOC access to South Dakota:

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Media

Ten31 Managing Partner Matt Odell appeared on RoxomTV to discuss the rise of bitcoin treasury companies.

Fold Founder and CEO Will Reeves was featured in a profile on CCN.

Market Updates

After the market got all hot and bothered by last week’s ceasefire news, Vice President JD Vance rained on the We’re So Back parade over the weekend by announcing that his talks with Iran had concluded with no deal.

President Trump immediately announced the US would initiate a full naval blockade of Iranian ports, playing the classic “you can’t blockade me, I’m blockading you” reverse card.

While there were legitimate concerns over the quick escalation that might happen if the blockade were tested, the maneuver appeared to hold up through the week, as the Navy turned away or interdicted (a word we all totally knew before this week) dozens of ships without major incident.

At the same time, the Treasury Department ramped up Operation Economic Fury, extending sanctions on various individuals and companies in the Iranian oil industry, while noting temporary authorizations to sell Iranian oil will not be renewed. The Treasury also reportedly issued warnings to Chinese banks with ties to Iranian fund flows.

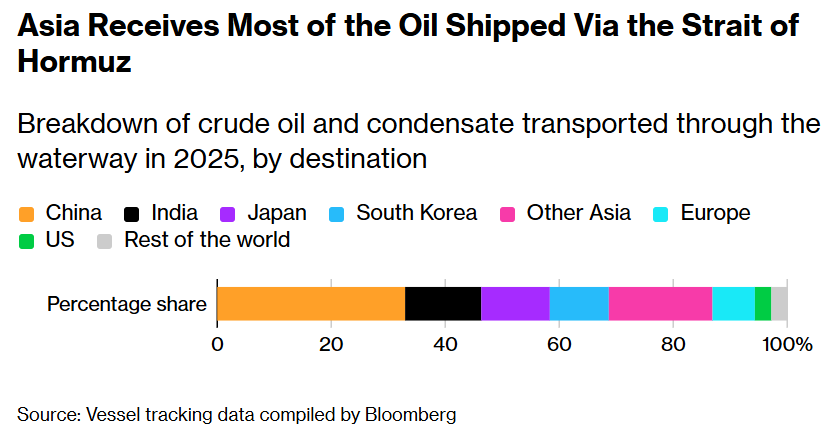

Bloomberg put out a feature highlighting how disruptive an extended blockade would be for Asian economies, with comparatively little direct damage to the US. Of course, the downstream impacts like fertilizer production remain a major concern, and in any case the move won’t be cost-free for President Trump, as he admitted this week that gas prices may remain elevated through midterms.

However, the President reiterated mid-week that it will all be over very soon, after which point the stock market “is going to boom.”

Shortly thereafter, the administration announced that Iran had agreed to surrender its enriched uranium – a key point of contention in negotiations – and Iran announced (on the back of a 10-day ceasefire between Israel and Lebanon) that the all-important Strait of Hormuz would be open to all traffic during the ongoing ceasefire.

These headlines sent oil prices tumbling more than 10% lower on Friday and pushed equity indices firmly back to new all-time highs – more than erasing losses since the start of the war – as bitcoin surged back to $78,000 before retracing a bit early Saturday.

That said, the whole situation continues to be history’s largest double-slit experiment, as the President later suggested that the naval blockade would remain in force until a final deal is reached, prompting Iran (or some faction thereof) to respond Friday night that it has actually rejected the uranium deal and that traffic through the Strait of Hormuz will remain restricted as long as the US blockade stays in place.

Our guess is that consensus on the situation will transition from wave to particle several more times before markets open on Monday, but lost in the shuffle of the week were several more examples of the US consolidating power abroad, including a “major defense cooperation partnership” with Indonesia, which may be particularly noteworthy for a maritime-focused administration given the importance of the Strait of Malacca.

Elsewhere, the UK agreed to pause its handover of the Chagos Islands to Mauritius following pressure from the US. The islands are home to the Diego Garcia airforce base, often thought to be a key military asset for the US’s influence in East Asia.

The week also saw several noteworthy headlines for the US-China relationship, which we’ve argued is the closest thing to a Rosetta Stone for Trump 2.0 that we’re going to get. First off, the President threatened 50% tariffs on China if they supply Iran with weapons as rumored last week; shortly thereafter, the Middle Kingdom allegedly assured the President it would hold off.

An in-depth article from the Financial Times highlighted China’s recent aggressive push into advanced tech exports, which has put competitive pressure on prized industries of many Western economies. On the flipside, after a strong start to the year, Chinese exports were up only 2.5% in March, and were significantly outpaced by imports.

In response to rising protectionism abroad, China imposed new rules to prevent multinational companies with operations in the country from pursuing a “decoupling” strategy for their supply chains.

Amid the recent fracturing of the World Is Flat global order, Russia reiterated support for China this week, offering to ramp up energy flows to backfill disruptions out of the Middle East. In a totally unrelated development, US officials suggested the military is gaining influence in Libya, progressively squeezing Russia out of its main resource-rich beachhead in Africa.

Back in the Western Hemisphere, the Pentagon is reportedly ramping up plans to make a move on Cuba following months of speculation in rags like this one, and President Trump said on Friday night that a “new dawn” is coming for Cuba very soon.

Meanwhile, Jair Bolsonaro – the MAGA-friendly former Brazilian President often dubbed the “Trump of the Tropics” – has now edged out Xi-aligned incumbent Lula as the Polymarket favorite to win Brazil’s next presidential election this fall.

Finally, Commerce Secretary Howard Lutnick indicated that the USMCA agreement – which governs trade between the US, Canada, and Mexico – needs to be significantly reworked during this summer’s renegotiation. Regarding the US’s relationship with Canada, Lutnick (ever the diplomat) noted that “they suck.”

Domestically, the military continued to move closer to the World War II industrial playbook, as the Pentagon has reportedly held discussions with American automakers including Ford and GM about leveraging their factory capacity to produce munitions and military equipment.

Despite the massive spike in oil prices over the past month, the latest Producer Price Index reading for March was up much less than expected at just +0.5% M/M, though that still works out to +4% Y/Y. Notably, Core PPI (ex-energy) was barely up at all on the month.

Almost all US bank quarterly earnings reports were generally solid this week, with Bank of America CEO Brian Moynihan indicating the US economy looks resilient. The strong headline prints may mask ongoing questions about the health of institutional balance sheets more generally, as the Federal Reserve has reportedly asked US banks for more detail on their exposure to the troubled private credit market.

Fed Chair nominee Kevin Warsh filed disclosures on his personal holdings this week that show he would be easily the wealthiest Chairman in history. However, Warsh’s path to actually landing the job was further complicated this week by another flare-up in the Powell / Trump feud, as prosecutors from the DOJ reportedly stopped by the construction site of the Fed’s controversial new building.

Like any good showman who knows people just want to hear the greatest hits, Trump revived his classic “I’m Going to Fire Too Late Powell” this week, noting he would have to remove the outgoing Chairman from the central bank if he doesn’t voluntarily step down from the Board of Governors.

Trump’s long-running focus on getting benchmark rates lower notwithstanding, Treasury Secretary (and close Warsh associate) Scott Bessent said this week that it’s reasonable for the Fed to “wait and see” what happens with energy prices before making any further moves on rates.

Despite the foreign chaos and a deeply uncertain regime at the Fed – which have ramped up calls for imminent international de-dollarization – Norway’s $2 trillion sovereign wealth fund says it has no plans to reduce US asset exposure. At the same time, three major Gulf States have raised ~$10 billion in cumulative dollar-denominated bonds since the start of the war.

All the same, former Treasury Secretary and TARP architect Hank Paulson told the press this week that regulators need to develop an emergency plan for an eventual “vicious selloff” in Treasuries.

Strategy’s STRC preferred stock ramped up its bitcoin acquisitions once again over the past two weeks, driving purchases of roughly 14,000 bitcoin last week and an estimated 17,000 this past week. The company noted on Friday that it will move to paying dividends twice per month to reduce face value volatility.

It was a very strong week for spot bitcoin ETFs, as the whole complex took in just under $1 billion of inflows. Morgan Stanley’s MSBT ETF – launched just last week – has already exceeded the AUM of WisdomTree’s bitcoin ETF.

Goldman Sachs jumped on the increasingly crowded bandwagon of traditional finance bellwethers launching mainstream bitcoin-linked products, as it announced its own bitcoin income ETF based on a covered call strategy.

Wealth management behemoth Charles Schwab announced that it will launch direct bitcoin trading on its platform in the next few weeks.

Regulatory Update

White House digital assets adviser Patrick Witt said this week that a list of roadblocks to passage of the CLARITY Act previously thought to be unsolvable have now been resolved.

The SEC published a path for some non-custodial digital assets tools to bypass broker registration rules if they meet a series of requirements. This doesn’t directly apply to bitcoin given its treatment as a commodity, but signals an ongoing shift in the broader regulatory understanding of non-custodial applications.

Noteworthy

Leading stablecoin issuer Tether launched tether.wallet, the company’s first product that directly interacts with end users. This development may align nicely with the glide path we projected for stablecoin issuers in our recent stablecoin deep dive.

Presidio Bitcoin released a summary of the current state of bitcoin’s readiness for the potential emergence of quantum computers. A key differentiated finding of the report is that actual on-chain migration from vulnerable addresses to post-quantum addresses may be much faster than is often feared.

A group of developers published BIP-361, a controversial proposal for post-quantum migration that would eventually render vulnerable coins unspendable. Major exchange BitMex, meanwhile, published a proposal for a “quantum canary fund” as an alternative.

Major US aluminum producer Alcoa is reportedly in advanced talks with NYDIG to sell one of its dormant smelter assets in upstate New York for use in bitcoin mining.

Travel

Bitcoin 2026, Las Vegas, April 27-29