The Wartime Economy Is Here, It's Just Not Evenly Distributed - Ten31 Timestamp 931,727

Even more than usual, it was the Trump Show this week, as the President said “hold my beer” to everyone who thought 2026 couldn’t possibly be crazier than 2025. Following last weekend’s sudden and much-memed seizure of Venezuelan leader Nicolas Maduro, the administration seemed to drop all pretense and take the gloves off, with Trump explicitly highlighting the ascendant “Donroe Doctrine” of renewed US dominance in the Western Hemisphere (a dynamic we were calling out in this newsletter during the back half of last year). Throughout the week, the administration ramped up its rhetoric against virtually every major player in Central and South America, while also highlighting plans to annex or in some way exert significant control over Greenland, including by means of “the hard way” if necessary. At the same time, the President announced a litany of unilaterally declared measures (most of which likely have questionable enforceability) that escalate last year’s forays into outright industrial policy and point very clearly to a wartime mentality, including hard ceilings on executive compensation for defense firms; a massive increase to the American military budget; and various blunt-instrument approaches to capping consumer-facing interest rates. We highlight all this in a bitcoin-oriented newsletter because consensus still doesn’t seem to have processed that we appear to already be at war in the minds of those at the geopolitical switchboard, and the unipolar, “rules-based order” moment of the last fifty years is likely over. If we’re right, this will all have significant implications for American fiscal policy, financial repression, and global capital flows, and in turn, significant implications for the world’s only globally accessible, permissionless, fixed-supply, neutral monetary network. Political leanings aside, we encourage all readers to look beyond the Red Team / Blue Team kayfabe and consider that Treasury Secretary Scott Bessent might not have been kidding when he promoted the idea of a global economic reordering.

Selected Portfolio News

Primal released version 2.6 of its flagship app, which now includes an innovative remote signing flow for all Nostr apps:

As the world’s largest investor focused entirely on bitcoin, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem, and we expect 2026 to be the best year yet for both bitcoin and our portfolio. Visit ten31.xyz/invest to learn more and get in touch to discuss participating.

Media

Ten31 Advisor and Zaprite Head of Business Development Parker Lewis gave a compelling talk on the outsized positive asymmetry of bitcoin adoption.

Market Updates

The Donroe Doctrine – no longer just a smarmy Atlantic headline, but a title actively embraced by the President himself – seemed to reach escape velocity this week, as Trump doubled down on last weekend’s extraction of Venezuelan leader Nicolas Maduro by indicating the US will be “very involved” in the Venezuelan oil industry from now on.

Specifically, the President suggested Venezuela will immediately turn over up to 50 million barrels of oil and will be supplying oil to the US “indefinitely,” as US oil majors are allegedly set to spend $100 billion in the country with US protection.

Potential downward pressure on US gas prices would no doubt be a welcome secondary effect for the administration heading into midterms, but the primary motive likely has more to do with Chinese and Russian influence in the region, as the White House reportedly demanded Venezuela’s new leadership immediately cut ties with the rival powers.

Elsewhere in hemispheric dominance, the President insinuated that Colombia is now on notice, while Secretary of State Marco Rubio declared that the Maduro ouster should be a warning to the Cuban government.

Even more notably, Trump suggested that “something has to be done about Mexico” and that the US will soon begin direct land strikes against cartels in the country.

Meanwhile, the President reiterated for good measure that the US still wants control over Greenland as a key strategic asset. The ultimate wisdom of all this rhetoric aside, the White House unfortunately appears to be taking some cues from Senator Holden Bloodfeast.

{kind=link}

The Venezuelan box-out seems to be putting an early squeeze on Chinese oil refiners, who have reportedly ramped up calls to Canadian producers in recent weeks. This is particularly noteworthy in conjunction with Trump’s rhetoric toward Mexico, as the US-Mexico-Canada (USMCA) trade agreement – which replaced NAFTA in 2020 – is up for its first renegotiation this July.

At the same time, uprisings in Iran escalated substantially this week, potentially posing a material threat to the current regime. This might also present an issue for China, which was reportedly hoping to backfill lost Venezuelan oil supply with increased Iranian exports. A more cynical observer (definitely not us) might note that this is all very interesting timing given the US’s colorful history of participation in Iranian politics.

In a probably unrelated update, US forces in South Korea are reportedly preparing rapid response capabilities for a potential Chinese incursion against Taiwan.

As the US’s wartime footing becomes more explicit, President Trump said this week that he “will not permit” defense companies to do stock buybacks and dividend payouts until they address his concerns about the industry, including building more production capacity and delivering weapons more quickly. Moreover, Trump called for defense executives’ pay to be capped at $5 million.

However, no denizen of the Military-Industrial Complex should lose much sleep, as the President went on to call for a $1.5 trillion military budget next year, which would represent close to a 70% Y/Y increase in the latest clear indication of Trump’s desire to “run it hot.”

Elsewhere in unilateral Truth Social demands with questionable enforceability, the President said he will take steps to prevent institutions from owning single-family homes in an attempt to free up housing supply and control home prices. If this sticks, it’s worth noting that, on the margin, this would reduce the store of value premium baked into housing, and it may be instructive to consider where some of that premium might flow instead.

Lest you forget about monetary policy amid all the overseas adventurism, Treasury Secretary Scott Bessent suggested this week that the only missing ingredient for a stronger economy from here is lower interest rates.

Once again, Trump tried to take matters into his own hands here by demanding that government-sponsored mortgage securitizers Fannie Mae and Freddie Mac purchase $200 billion in mortgage bonds to push mortgage rates down. He also indicated he will mandate a 10% cap on credit card interest rates for one year starting next week. We’re confident that neither of these maneuvers will have unintended downstream consequences.

On the employment front, Minneapolis Fed President Neel Kashkari said the proliferation of AI is now causing a hiring slowdown at large companies; however, he still doesn’t think rates need to come down much more.

Jobs data on the week were mixed, as ADP figures came in slightly below consensus, while the official Non-Farm Payrolls data came in fairly weak as well, with particular softness in manufacturing.

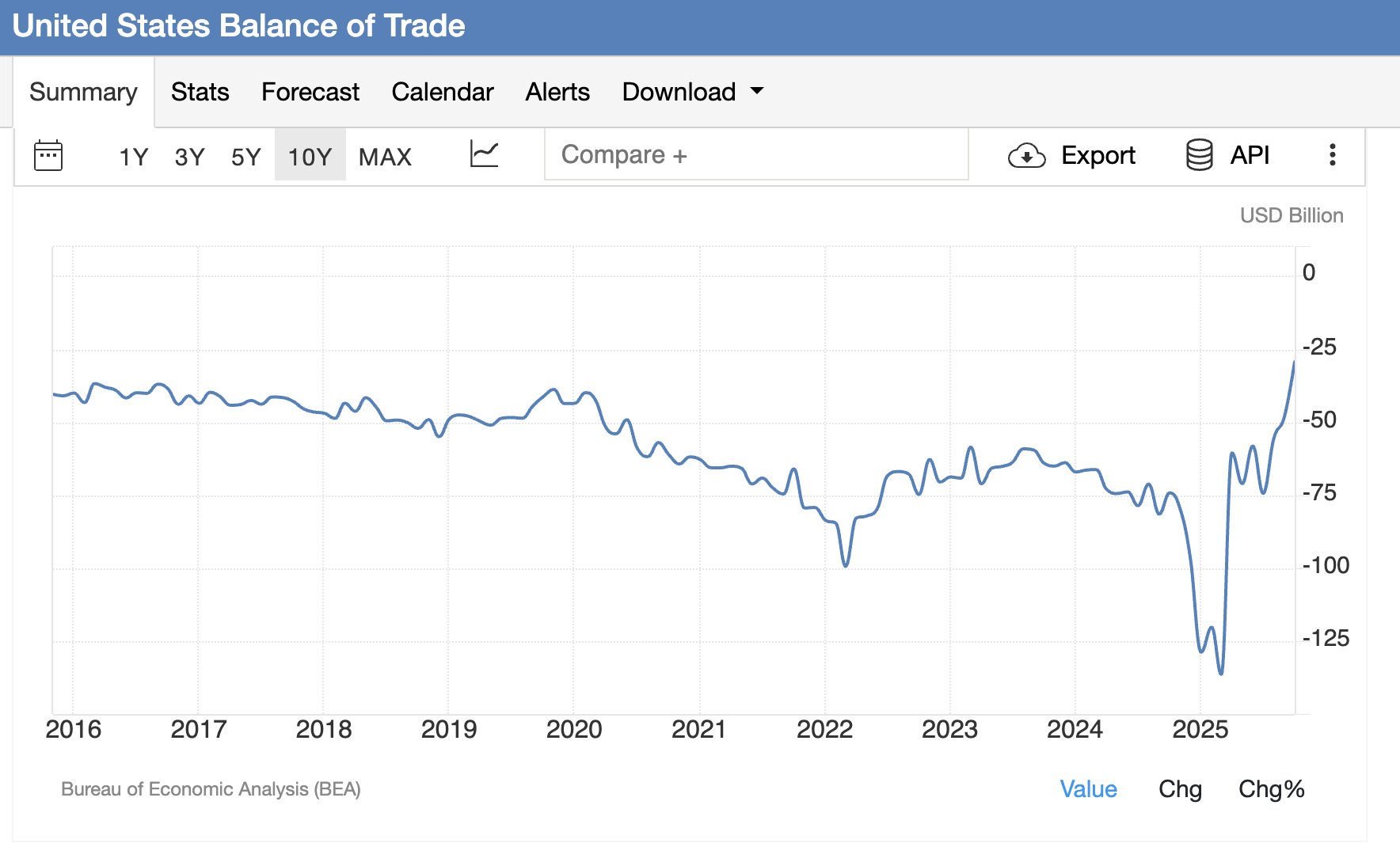

More encouragingly, the Atlanta Fed’s GDPNow indicator is now pointing to 5.4% growth in Q4, though this appears to be largely an artifact of much higher net exports Y/Y as the latest US trade deficit figures came down dramatically. This trade deficit headline by itself requires a few major qualifications including collapsing pharma imports (reversing some frontrunning earlier this year) and large gold exports.

A dramatic week for global markets also included some very noteworthy headlines for bitcoin, as Bank of America officially began allowing all wealth advisers to recommend bitcoin ETFs to clients.

Meanwhile, a few months after opening up access in their wealth channel, Morgan Stanley filed an S1 for its own bitcoin ETF. Very notably, this will be just the bank’s third ETF to bear the flagship Morgan Stanley branding.

Regulatory Update

Reports this week suggested the Department of Justice potentially violated an element of last year’s Strategic Bitcoin Reserve Executive Order by selling bitcoin forfeited as part of the Samourai Wallet indictment, though the US Marshals denied the accuracy of the report.

Florida legislators proposed a new bill to stand up a state bitcoin reserve, the latest in a series of similar attempts in the state over the past year.

Noteworthy

After months of consternation among bitcoin treasury company investors, index provider MSCI elected not to exclude these vehicles from its indices for now.

Various rumors swirled around Bitcoin Twitter this week about a supposed stockpile of 600,000 bitcoin held by the Venezuelan government and the potential implications for the Strategic Bitcoin Reserve. Significant ethical questions aside, we’ll take the under on the headline figure.

Pseudonymous bitcoin and ecash developer Calle posted a demo using Bitchat to send bitcoin without internet on the sender side.

Prominent crypto hardware wallet producer Ledger announced another leak of sensitive user data, the latest in a long string of data security incidents at the company.

Alternative video platform Rumble unveiled an integrated noncustodial wallet enabling payments and creator tipping with bitcoin, Tether, and Tether Gold.

Travel

Nashville Energy & Mining Summit, Jan 2026

Bitcoin Investor Week, Feb 2026