To Hike or Not to Hike: Ten31 Timestamp 942,634

There are no inflation hawks in foxholes

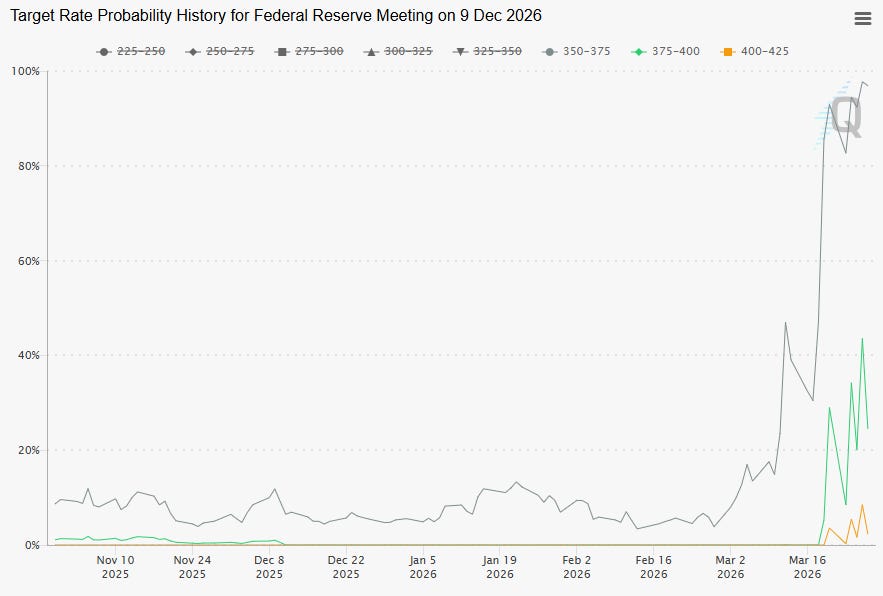

That’s a wrap on Week Four of Mr. Trump’s Wild Ride, and unfortunately the Fog of War just continues to grow thicker by the day, with journalists and newly-minted maritime experts on Twitter breathlessly repeating and trading on every remark from the US, Israel, and Iran (three famously transparent and reliable regimes). As the market waits to see whether we’re looking at a repeat of Britain’s international downfall in the 1956 Suez Crisis or the start of a 50-year era of peace and trade stability led by the US, our attention increasingly turned this week to an emerging consensus view that, far from being able to cut benchmark rates this year, the Fed will actually need to hike rates to combat the inflationary impacts of ongoing oil flow disruptions out of the Middle East. For part of this week, the CME Fedwatch tool indicated coin-flip odds of some degree of rate hikes by year-end, and while we’re far from rates traders, we remain deeply unconvinced that the Fed has any real room to get meaningfully tighter, absent a political willingness for true fiscal austerity (lol, lmao even). As we wrote about earlier this year following the Kevin Warsh nomination, the US fiscal position is far from what it was even 20 years ago – much less 50, during the last major global oil shock – and blended interest expense even a bit higher than the current level is consequently unworkable relative to nondiscretionary federal outlays, particularly now that we may need untold incremental trillions to kill bad guys. We won’t try to call the exact transmission mechanisms or new alphabet soup facilities that may ultimately be required, but history clearly suggests that the exigencies of any (real or Trumped Up) emergency that threatens a sovereign’s hegemony will dominate any concerns over headline inflation prints. To anyone who believes the Fed can’t be accommodative for fear of inflation in the face of commodity shocks and supply chain disruptions, we would suggest your grandparents might beg to differ.

With all that in mind, we also thought it was an interesting week for some fundamental developments in bitcoin. First off, ETF flows are now almost back to flat on the year despite massive volatility both in the price and the broader global stage, and Morgan Stanley – whose overall asset management business runs nearly $10 trillion in AUM – announced that their upcoming bitcoin ETF (one of just a few vehicles bearing the flagship Morgan Stanley branding) will be the cheapest option on the market, undercutting IBIT on fees in a signal of the demand the platform is likely seeing from its advisors. Meanwhile, Fannie Mae opened the door to a new mortgage structure that lets bitcoin-backed financing (without any mark to market component) support officially conforming mortgages, opening such loans up to the secondary market and potentially paving the way for a major new integration of bitcoin into traditional financial products. While most investors remain focused on hedging the minute to minute remarks of bureaucrats around the world, we would encourage readers to stay focused on this ongoing drumbeat of fundamentally constructive news flow for bitcoin, particularly if our thoughts on the Fed’s posture in the current environment prove to be directionally correct.

Selected Portfolio News

Fold launched the full rollout of its credit card, which offers users up to 4% back in bitcoin:

Debifi launched the beta for its institutional lending API:

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Media

Ten31 Managing Partner Matt Odell joined the Bitcoin News show to discuss a wide variety of topics, including the increasing convergence between bitcoin and AI.

Market Updates

President Trump once again made sure everyone had a pleasant weekend with a vintage Truth Social post – crucially, after markets were closed – threatening Iran with strikes on the country’s power plants if the Strait of Hormuz was not opened in 48 hours.

Before Monday’s market open, though, the President suggested talks for a resolution have been productive and agreed to extend the deadline to Friday, then later extended that deadline for another 10 days after simultaneously suggesting that Iran has given the US a “very big present”, they’re begging to make a deal, but also that their negotiators need to “get serious before it’s too late.”

While Trump continues his classic Michael Scott snip-snap routine and Treasury Secretary Scott Bessent suggests we need to “escalate to de-escalate”, Iranian officials have largely projected an adversarial posture and insisted all week that no negotiations are taking place.

Perhaps most aggressively and notably, the speaker of Iran’s parliament tweeted that the country will specifically target large holders of US Treasuries, the conflict’s first explicit acknowledgment of one of the US’s main points of vulnerability (though to be fair, this is also a pretty long list that basically amounts to most major US allies).

We’d probably tend to fade the reliability of all public comments made from all sides of the conflict, as well as all corporate press reporting based on “sources familiar with the matter,” but for whatever it’s worth, various reports suggested the US has delivered a 15-point plan that has gained traction with factions of Iran’s government.

Secretary of State Marco Rubio was less optimistic, suggesting to G7 allies that the fighting will continue for another 2-4 weeks. It remains unclear if that will be enough time for the President to establish joint custody of the Strait with the Ayatollah and rebrand it as the Strait of Trump.

Even amid all the disruption and oil prices hitting highs not seen in several years, the President commented this week that he actually expected prices to go even higher than they have, but either way they’ll all return to prior levels soon.

But all the feints at de-escalation – which seem to be progressively losing their efficacy – weren’t enough to get oil prices meaningfully lower, as WTI closed the week just above $100. Meanwhile, the Brent-WTI spread we flagged last week has remained elevated and around decade+ highs.

To that point, the Washington Post flagged this week that US natural gas exporters will be key beneficiaries of this conflict, in line with our prior observations about asymmetric impacts between energy exporters and importers.

At the same time, local reports suggest the disruptions are starting to bite Chinese manufacturing, with many producers curtailing production due to spikes in raw material and logistics costs of more than 50%.

Chinese ships have reportedly also not been able (or have elected not to attempt) to exit the Strait this week despite explicit assurances from the Iranian regime, an interesting data point for the consensus view of affairs in the area.

However, reporting out of the Gulf also suggests Iran’s ongoing strikes around the region have severely damaged many nearby US bases, potentially crimping the military’s influence and operational capacity near the Strait.

Meanwhile, the disruptions have naturally also started to present significant headwinds for US allies in the East, as the Philippines became the first country to declare a national energy emergency due to the war, while South Korea imposed new export controls and “hoarding bans” on key commodities, and over 8% of Australian fuel stations are now struggling to stay stocked.

Finally, and most crucially for the US’s ability to sustain its current posture, US Treasury yields hovered around recent highs all week and escalated to almost 4.5% on Friday before pulling back a bit, as the MOVE Treasury volatility index – which has significant implications for the hedge funds that have come to represent a key pillar of issuance absorption – continued to climb to another post-Liberation Day high of 115.

While we hesitate to point mouth agape at every negative Treasury auction headline that comes across the wire, it was also a rough week for new issuance, as three separate auctions put up poor results.

In response, a former Fed analyst and advisor to temporary Fed Governor Stephen Miran published a piece arguing the Fed should extend swap lines to foreign sovereign wealth funds, pension funds, and similar private / semi-private actors that have large Treasury holdings they may otherwise need to tap into for liquidity during the ongoing Gulf chaos.

Pro-liquidity implications of that plan aside, Miran himself said he believes the Fed has a path to slowly reducing the size of its balance sheet by $1-2 trillion.

The Financial Times published a piece this week suggesting that Secretary Bessent is explicitly seeking greater control over the Federal Reserve, a regime shift that the dynamics above could make increasingly important. However, Bessent – never one to mince words – denied the claims in no uncertain terms.

Like last week, overseas sovereign debt markets felt even more pain, as yields on long-dated Bunds, OATs, Gilts, and JGBs all continued to surge to new multi-decade highs (and don’t look now, but the USDJPY cross broke through the closely watched 160 level for just the second time in nearly 40 years late Friday).

The growing quagmire and upward energy price pressure has now officially pushed traders into betting on Fed rate hikes before year-end to counter expected inflation pressure.

Negative headlines continued to pile up in the private credit complex as well, as Apollo and Ares joined their megafund peers in gating redemptions by wide margins, and Moody’s cut its ratings on several other funds.

Nevertheless, BlackRock CEO Larry Fink argued that Social Security’s trust funds should invest more aggressively into higher-return instruments (like maybe…private credit?) to help Americans more effectively build wealth.

All the volatility and uncertainty continued to weigh on equities as well, officially pushing the Dow and Nasdaq into correction territory. The general liquidity backdrop is not helping matters here, with multiple indices pointing to sharp recent declines in global liquidity.

Despite the will-they / won’t-they between Trump and the Ayatollah and rough bitcoin price action on the year, flows into bitcoin ETFs have remained extremely resilient and have now almost erased all cumulative outflows from early in the year.

Morgan Stanley’s upcoming spot bitcoin ETF plans to charge only 14bps on AUM, making it the cheapest ETF option available, an interesting signpost for the type of demand the bank may be seeing within its asset management channel.

Following a directive from FHFA Chairman Bill Pulte last year, US mortgage market lynchpin Fannie Mae announced it will begin supporting a new form of bitcoin-backed mortgage. The agency will treat mortgages that use bitcoin as collateral – without any mark to market component – as standard conforming mortgages, potentially opening up a major new integration of bitcoin into traditional financial plumbing.

Elsewhere, bitcoin has seen a steep decline in network hashrate over the past two weeks, with the headline figure declining more than 50EH/s since the start of March, likely due at least in part to energy disruptions from the conflict in the Gulf.

Regulatory Update

The long-stalled CLARITY Act reached a new compromise proposal this week, potentially positioning the bill to move forward. However, key industry participants apparently remain unsatisfied as the latest version would still prevent stablecoin issuers from paying yield to holders, an update that drove significant declines in Circle and Coinbase stocks this week.

The Bitcoin Policy Institute brought together representatives from Coinbase, Block, and River on Capitol Hill to push for a bitcoin de minimis tax exemption.

However, the recently released PARITY Act appears to still exclude bitcoin from de minimis exemptions (while protecting, humorously, stablecoin payments). The bill also only provides double-taxation relief for staking protocols and leaves bitcoin mining still exposed to the same punitive treatment (whereby mining rewards are first taxed as ordinary income upon generation, only to be also subjected to capital gains tax when those rewards are sold or spent).

Noteworthy

Major public bitcoin miner MARA retired a $1 billion convertible note by selling ~15,000 of bitcoin from its corporate treasury. The company continues to hold over 38,000 bitcoin on its balance sheet.

As an interesting data point in the US-China decoupling we’ve flagged in this newsletter over the past year, Murata Manufacturing – a key Apple supplier worth ~$50 billion – announced a move to separate its Chinese rare earth supply chain from the rest of its business.

Travel

OPNext, New York, April 16

Bitcoin 2026, Las Vegas, April 27-29