You Gotta MOVE: Ten31 Timestamp 957,573

Here we go again?

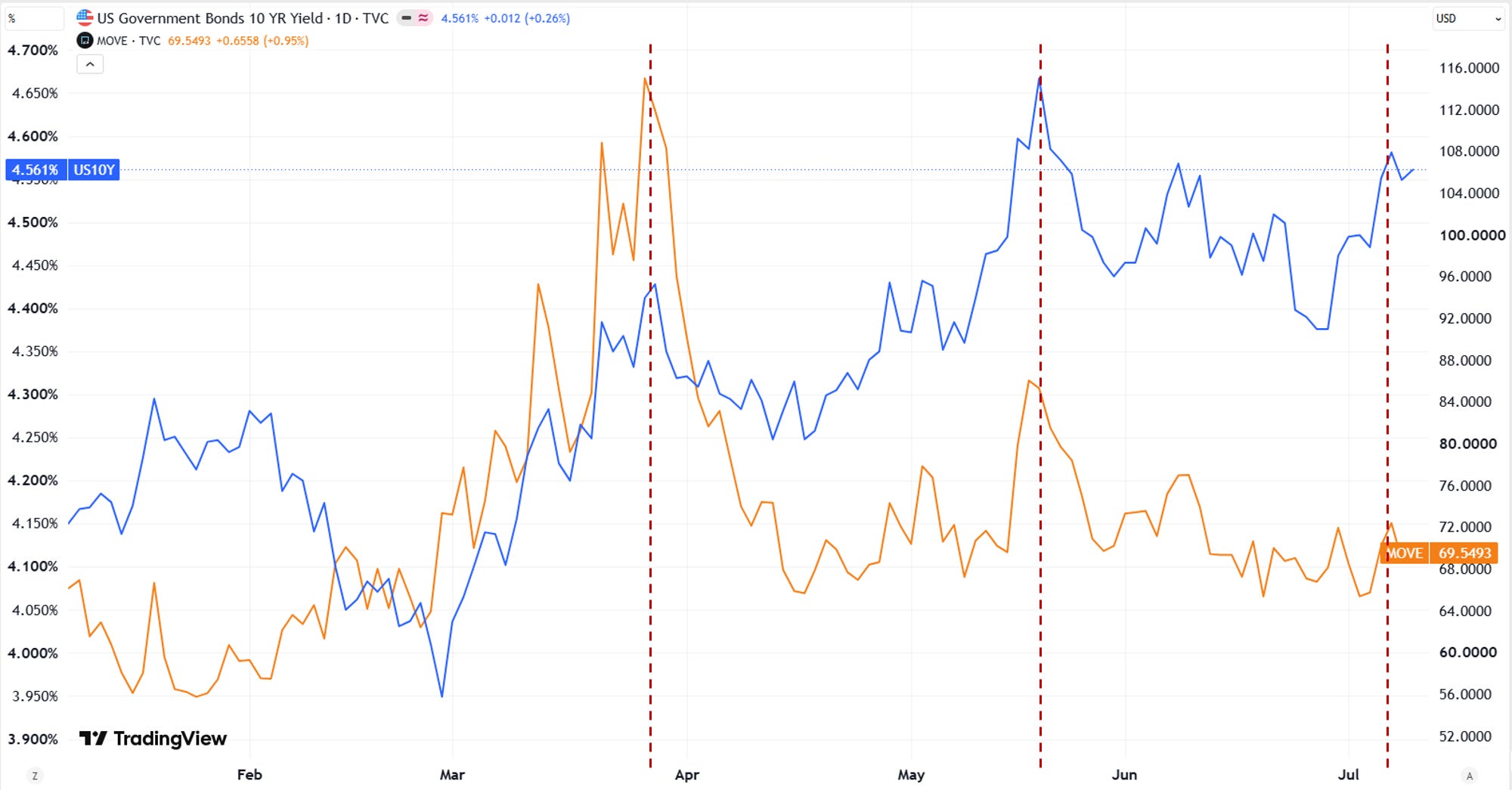

You just knew it was too good to be true. The next season of everyone’s least favorite will they / won’t they drama was greenlit by the studio this week, as the US and Iran put aside their tenuous (and apparently poorly worded) “Memorandum of Understanding” to return to trading strikes around the Persian Gulf. As usual, this latest round of slap fighting was accompanied by declarations from both sides that their counterparty is unreliable scum who can never be trusted (but also talks are ongoing). Notably, though, this recent escalation has (for now) not done much to oil prices, as key benchmarks fell back near pre-war levels after a quick spike up earlier in the week, and even more significantly, bond volatility has generally been subdued even with US Treasury yields heading back toward YTD highs. As prominent liquidity observer Michael Howell has noted, managing the Treasury market’s volatility may be even more important in the near-term than managing exactly where yields shake out (though as we’ve argued elsewhere, that will eventually matter too), but in any case the action this week shows a market that does not believe that network execs will keep this new season on the airwaves for very long, or at least that its impacts on the US’s strategic position are getting closer to a point of diminishing returns. It’s too early to call here, but if that intuition proves correct (i.e. if the bond market can avoid reflexively puking longer than IRGC hardliners can hold out), analysts should bear in mind the implications that would have for the administration’s pursuit of its broader policy agenda in the near term.

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Selected Portfolio News

Giga Energy announced GigaBase, a comprehensive, scalable system for AI data center development:

Strike launched volatility-proof loans, a unique product offering protection against loan liquidation from bitcoin price volatility:

Media

Upstream Data Founder and CEO Steve Barbour discussed his pioneering work in deploying bitcoin mining in the oilfield.

Market Updates

After roughly a month of relief from a news cycle dominated by a narrow strip of water most Americans had never heard of at the start of the year, the US and Iran put their “Memorandum of Understanding” on ice this week as Iran attacked several ships making passage through the Strait of Hormuz.

The US immediately withdrew its recent waiver allowing the country to sell oil without sanctions and resumed strikes on various Iranian targets.

Alongside some choice words for his counterparty, President Trump declared the ceasefire (peacefire?) dead as he no longer wants to deal with all this (you and me both, pal), briefly sending oil up ~6% midweek.

The timeline for a durable resolution here once again remains elusive and is complicated by ongoing reports (which used to be confined to tinfoil hats on Twitter but have since breached containment to outlets like the New York Times) that leadership in Iran remains deeply divided, with a hardline IRGC faction aggressively opposing any deal with the US.

That said, both WTI and Brent retreated close to prewar levels over the course of the week, even as the White House ramped up threats of a renewed blockade on Friday, suggesting investors aren’t yet buying that this is a Spring 2026 Redux.

Importantly, though, Qatar said it would pause its efforts to restart production at Ras Laffan, the world’s largest LNG facility, in response to the renewed disruptions, and unlike oil, European natural gas benchmark prices are trending back toward highs from the spring, which definitely bears monitoring as we inch closer to winter.

Various sources reported that Saudi Arabia is pursuing plans to expand the capacity of its East-West pipeline – a key alternative export option that bypasses the Strait entirely – by 2 million barrels per day (vs ~7 million today), though such an expansion would take several years.

Alongside the pop in energy prices, US Treasury yields also rose toward historically uncomfortable levels again on the headlines, but on notably low volatility, as the MOVE Index barely, uh, moved all week.

Japanese government bonds were not quite as tranquil, with yields continuing to break out to new 30-year highs.

Meanwhile, Treasury’s War has continued apace, as Iraq agreed to US demands to cut off dollar flows to Iranian-linked militias in exchange for a resumption of billions in dollar shipments to Baghdad that have been cut off since the start of the war.*

On the same front, the New York Times ran an editorial acknowledging the overall posture shift from Scott Bessent’s Treasury, citing his keynote speech at the Economic Club of New York that we flagged last month while noting that “the days of America being played are over.” Agree or disagree, it’s no doubt a noteworthy vibe shift to see the Gray Lady featuring a piece like this, and an interesting sign of some ideological pump-priming that may be taking place behind the scenes at the country’s foremost opinion-making institutions.

But lest you think that the Trump administration has gotten too distracted by the conflagration in the Middle East, the President renewed his calls for the US to acquire Greenland at a NATO Summit this week.

AI continued to grab its share of headlines this week, as SK Hynix – one of three members of the global DRAM mafia oligopoly, which was already publicly traded in Korea – officially went public in the US, immediately popping 13% and pushing the company into trillion-dollar market cap territory.

SK’s introduction to US capital markets should put them in a strong position to play nicely with Commerce Secretary Howard Lutnick, who is reportedly pressing both SK and Samsung to move more memory manufacturing to the US.

On the lab front, OpenAI rolled out its new class of GPT 5.6 models that were delayed for several weeks by government oversight, and as per protocol with frontier model releases, they immediately became the hot new kid on the block that’s going to take all the jerbs.

That said, the company is reportedly pushing back its plans for an IPO to next year on valuation concerns (no low ballers, Sam knows what he’s got).

One week after joining a special advisory board at the Department of War, prominent venture capitalist and AI evangelist Marc Andreessen was appointed to a new Federal Reserve advisory group to evaluate the economic impacts of AI.

The folks in the Eccles Building may first need to figure out which direction they’re rowing on more basic matters, as the latest Fed minutes unsurprisingly point to ongoing division on the right path for benchmark rates from here (though there appears to be solid consensus on new Fed Chair Kevin Warsh’s goal of reducing reliance on “forward guidance”).

As the Fed waffles on rates, existing home sales in the US continue to languish near decade lows, with the latest numbers for June showing a 2% decline M/M.

After selling a token amount of bitcoin last month for the first time since 2022, leading bitcoin treasury company Strategy sold a more meaningful chunk of 3,588 bitcoin this week to fund dividend payments on its preferred shares.

Circle, the largest US-based stablecoin issuer, received its final OCC approval to establish a national trust bank (despite ongoing protests from the banking industry of these licenses being granted to such upstarts), the latest move bringing digital assets players closer to traditional monetary plumbing.

*Evergreen tweet for everything about this headline.

{kind=link}

Regulatory Update

Bloomberg reported that various officials and agencies in the Trump administration – specifically those in the Treasury and Commerce Departments – are in the process of wrangling over who has legal authority to control the strategic bitcoin reserve (which could be read as bullish or bearish depending on your inclination).

But whoever ultimately gets the keys to the orange Ferrari, the President reiterated at a press conference this week that he’s a “big crypto guy” while indicating that bitcoin might become eligible for his recently launched Trump Accounts.

On the flipside, in a decision that seemed to amount to “because volatility,” New Hampshire’s Executive Council voted not to advance a $100 million bitcoin-backed bond that seemed to have a good deal of momentum coming into this year.

Overseas, the EU continued to march steadily toward its apparently preordained Orwellian end state with the passage of the first leg of its mostly unpopular “Chat Control” framework to enable mass warrantless surveillance of digital communications.

Noteworthy

River published an updated article on the US as the world’s “bitcoin superpower,” outlining various metrics by which the US is in clear position to disproportionately benefit from growth in bitcoin adoption.

Polymarket added instant bitcoin deposit functionality over the lightning network.

A new study out this week (published, interestingly, by Chinese researchers) suggested that the Chinese rare earth minerals industry, a sector the country currently dominates and which has become a flashpoint in rising tensions between China and the US, effectively relies on patents controlled by the US and Japan (though it’s unclear how much this really matters given the questionable international enforceability of IP law).