War Doves and Inflation Hawks: Ten31 Timestamp 954,568

A week of narrative violations

Ladies and gentlemen, we made it. After months of false starts, frameworks of deals, messy breakups, and asymptotic progress, the US and Iran finally reached a deal to end (?) hostilities in the Persian Gulf and reopen shipping lanes through the closely watched Strait of Hormuz. Assuming this peace deal armistice extended pause whole thing holds for any meaningful amount of time, it will bring with it a series of major narrative violations that analysts and investors would do well to reckon with: oil didn’t go to $250, the 10-year didn’t go to 7%, the world didn’t reflexively de-dollarize, and the US didn’t (so far) get pulled into another neverending Middle Eastern quagmire (despite the exhortations of some Fox News regulars). That doesn’t justify the whole (mis)adventure, nor does it guarantee long-run success, but it should be a sign that the US still has a few rabbits to pull from its fraying hat, many of which will no doubt involve socializing any required pain from the workout of a long-term debt cycle onto the broader world (see Secretary of War Pete Hegseth’s “NATO 3.0” speech this week and ongoing “export restrictions” on frontier AI models for more).

While the market seemed to fret that newly-minted Fed Chair Kevin Warsh will throw a wrench into this whole gambit with his ostensibly hawkish desire to be “tough on inflation,” we continue to fade the narrative that Warsh will be, on net balance, meaningfully restrictive in the face of: more room to maneuver if the Iran deal holds; an already-struggling private credit backdrop; an increasingly K-shaped economy where the rates-sensitive lower half of the K is barely hanging on; a strategically critical AI buildout that can no longer rely solely on hyperscaler free cash flow; and federal nondiscretionary spending already roughly matching tax receipts. We can’t say for certain what moves the new Fed Chair might make – which appears to be exactly the way Warsh wants it given his rejection of the Bernanke-era “forward guidance” framework – but given all the outstanding constraints and Warsh’s long-running relationship with Treasury Secretary Scott Bessent (who has repeatedly called for greater coordination between the two institutions), we’d aggressively shade away from the narrative of Volcker 2.0.

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Selected Portfolio News

Giga Energy Co-Founders Matt Lohstroh and Brent Whitehead were named among E&Y’s Entrepreneurs of the Year:

Media

Various Ten31 portfolio companies were highlighted in Michael Saylor’s keynote speech at the Bitcoin Prague conference.

Market Updates

President Trump kicked off the week by announcing that the US and Iran had finally reached a deal (seriously guys, a real one, we mean it this time, no take-backs) to end the ongoing conflict that has roiled the Middle East for much of this year.

In what may be a first for any event scheduled by a government, the two sides managed to sign the “Memorandum of Understanding” ahead of schedule, putting pen to paper on Wednesday evening rather than the originally planned Friday signing date.

The 14-point “milestone-based” memo seems to have something for everyone, with neocons, pacifists, MAGA bros, and IRGC hardliners all loudly trumpeting their preferred narrative on how amazing or unconscionable the deal is for one side or another.

Most importantly for markets, though, the agreement provided for an end to the US’s blockade of Iranian ports and a normalization of shipping in the Strait of Hormuz, which quickly led to three Saudi tankers carrying 6 million barrels of oil to exit the waterway, followed by a steady uptick of traffic through the week.

In response, crude oil prices fell below $80 per barrel for the first time since the war broke out. And don’t look now, but the DXY Index – which measures dollar strength against a basket of global currencies – hit new YTD highs this week, despite months of rabid de-dollarizer fanfiction likely flooding your timeline since the onset of hostilities.

But just like your favorite comic book villain, the conflict may simply be dormant until the next episode rather than fully dead and buried, as the agreement includes a 60-day window for “final negotiations” that could end with both sides right back in the same spot if key points like Iran’s nuclear program remain unsolved. Moreover, many sharp analysts of the situation have suggested that even if the MOU holds up for now, this bears the hallmarks of a tactical pause to make way for midterms before firing up the full regime change sequel sometime in 2027.

That said, the strategic picture – particularly Iran’s leverage over the narrow waterway we’ve all unwillingly come to know too well – may look very different a year from now, depending on the pace at which various GCC countries can complete pipelines and other megaprojects to avoid the Strait altogether.

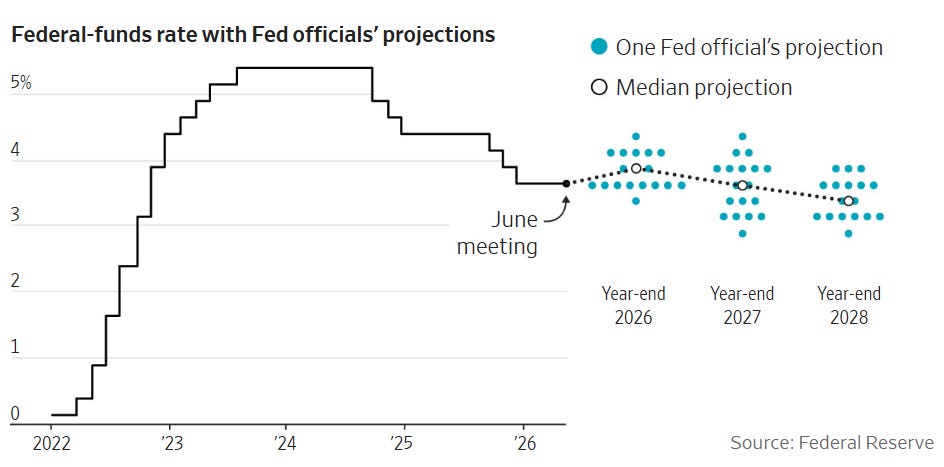

In any case, the potential tailwinds for sovereign bond yields that might have been stimulated by easing oil prices were largely offset by the first FOMC meeting under new Fed Chairman Kevin Warsh, where the central bank held rates steady but 9 of 19 officials indicated that a rate hike would be the likely next move from here (up from 0 pointing that way in March).

For reasons we’ve discussed elsewhere, for now we continue to fade the idea that hikes are coming this year – particularly if the US and Iran can maintain a tenuous peace through year-end and keep a lid on oil prices – and we’d argue the more notable takeaway from the meeting was Warsh staying true to his desire for “regime change” at the Fed, starting with a dramatically slimmed down official FOMC statement that begins the transition away from “forward guidance” (i.e. managing rates by informal jawboning).

Investors chose to once again interpret Warsh as moving the Fed in a more hawkish direction (partially thanks to his new task force to review the central bank’s ~$7 trillion balance sheet, whose size he has often criticized) and reacted accordingly, pushing stock indices to their worst “Fed day” move for any new Fed Chair since 1994.

One week on from the sudden forced removal of Anthropic’s Mythos-class models from public access, the situation remains unresolved (though Bloomberg reports some early users still have access).

As the frontier AI lab wrangles with the Commerce Department on the issue, President Trump indicated that no G7 countries will receive a carve-out from export controls on the model, which in our view should be seen as a warning shot for the strategic value the US ascribes to its lead in frontier intelligence (and which shouldn’t be surprising to readers of this newsletter).

In a similar vein, Secretary of War Pete Hegseth ramped up recent critical commentary of NATO in a speech this week, calling for a new 6-month DOW review of the US-NATO relationship, with a goal of moving toward a “NATO 3.0,” where Europe shoulders more of the financial burden for its own defense.

Meanwhile, following months of pressure from the Trump administration and biweekly half-serious threats of a ground invasion, Cuba initiated a sweeping privatization campaign this week that will represent the most significant shift in the country’s economy since Fidel Castro took power nearly 70 years ago, marking the latest win in the White House’s aggressive campaign to exert influence across Central and South America.

Elsewhere in US-led trade restrictions, Commerce Secretary Howard Lutnick suggested that Dutch lithography giant ASML – which essentially holds a monopoly over the most complex and critical technology required for producing advanced semiconductors – violated export controls on its key EUV technology by allowing a machine to make its way into China. The company denied the claims, which we note appear to be mostly a rehashing of reports from late last year.

Meanwhile, the wartime economy – and its re-run of the Freedom’s Forge playbook – got its latest nudge forward this week, as General Motors is reportedly in talks to supply weapons parts to defense contractor Lockheed Martin.

It was a typically boring bear market week for bitcoin’s price action, as the orange coin hovered in the low $60,000 range once again. In response, bitcoin continued functioning exactly as intended, with target mining difficulty adjusting downward for the 11th largest drop on record.

However, the institutional asset management world continued to ram up its bitcoin-linked offerings, as BlackRock’s BITA ETF (a bitcoin derivatives strategy targeting 15-25% in yield through covered calls) officially launched, and Franklin Templeton filed for two new ETFs that look to funnel dividend payments into bitcoin purchases rather than traditional equity reinvestment.

It wasn’t as quiet a week for the bitcoin treasury complex, as Strategy’s popular STRC preferred stock took its largest dip from par since inception, all the way down to ~$82 before retracing a bit. This is probably at least partially the result of a liquidation cascade from “looping” strategies popular with “DeFi” borrowers, but it no doubt complicates the comparisons of these vehicles to stable money market funds.

Regulatory Update

The Bitcoin Policy Institute team made a noteworthy trip to Taiwan to meet with policymakers regarding bitcoin’s strategic value to the closely-watched island nation. The trip came in response to BPI’s policy paper on the topic earlier this year.

Back in the States, Congressman Nick Begich conducted a lengthy interview walking through the rationale for and mechanics of his recently proposed ARMA legislation that would see the US accumulate a national reserve of 1 million bitcoin.

On the opposite side of the spectrum, Illinois passed a new bill that will levy a first of its kind 0.20% tax on essentially all bitcoin activities taking place in the state.

Key banking regulators including the Fed, Treasury, FDIC, and OCC published their first rulemaking proposal for GENIUS Act-compliant stablecoins. Among other points, the proposal would require full bank-style KYC for all onshore stablecoins.

Noteworthy

The UK announced a blanket ban on social media use for children under 16. While we have some sympathy for the deleterious impact of doomscrolling on young minds, we can’t help but wonder if this might be a convenient pretext for something more invasive.