When Donald Met Kimi: Ten31 Timestamp 958,548

Barrels, benchmarks, and bitcoin

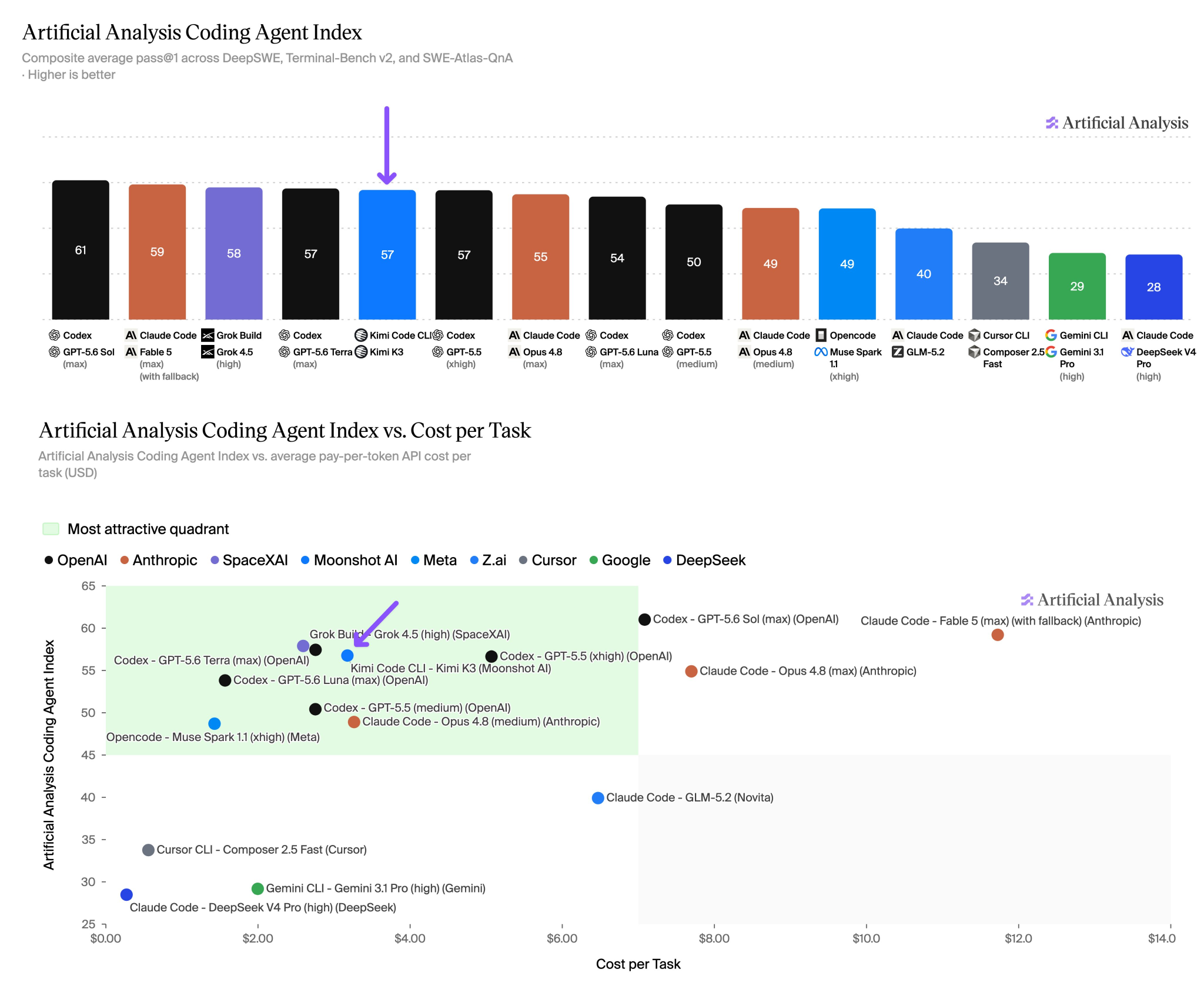

How you liking those summer doldrums, anon? The Great Power Race skidded into its next lap with a clear re-escalation of the conflict in Iran (can we just go ahead and call it a war now?), driving a cascade of impacts across critical supply chains. At the risk of beating a dead horse, we’ll highlight again that many of the results of this resurgent disruption will probably relatively favor the US over both China and Europe (the latter of which may be, from the White House’s perspective, strategically important to bring the junior partner in this project we loosely call “the West” fully onside). That said, we might actually argue that the more meaningful data point for the global chess board this week came not from Tehran but rather Beijing, as China’s Moonshot AI ignited another round of hand-wringing in a niche but increasingly influential corner of the internet with the release of Kimi K3, its latest open source model. K3 is the first Chinese open source model to score comparably to leading American frontier models on a variety of benchmarks at a much lower nominal sticker price, despite not benefiting from access to superior American chips used to train the most cutting edge models to date (though virtually everything about this sentence comes with massive caveats, including questions on benchmark-maxxing, relative model size, distillation / IP theft, the internal progress that frontier companies have allegedly made but not actually released publicly, and actual cost per task inferiority in real-world use).

We’ll have to see whether this is just another DeepSeek moment (you may recall, but probably not, that GLM 5.2 was supposed to be the model that would kill the frontier labs roughly 4 weeks ago), but either way we think this highlights an important dynamic that is likely to animate much market action across asset classes over the next several years. The most straightforward readthrough would be that this kind of aggressive fast-following by a geopolitical rival in one of the few domains where the US has had a clear advantage up till now is likely to catalyze even more urgency on the part of key American companies and the White House to do everything possible to further entrench American dominance at the frontier, which likely means both more “anti-espionage” measures (Exhibit A: this week’s China-focused revival of 2020 election audits) and, of course, more spending. But the second-order question many inventors are rightly asking here is whether the recent capex pace we’ve seen can reasonably be sustained if the inevitable free-rider problem of open source models durably crimps the expected ROIC of aggressive investment in training next-generation models. Game it out, though: if it’s no longer economical for private companies – even the biggest in the world – to build new frontier models, but scaling laws are still holding, the world’s most powerful government has made that investment push the key bulwark for what it sees as an existential reindustrialization agenda, and no defense department in the world feels comfortable waiting around to see if the other guy gets to the next frontier generation first, then who picks up the tab? The likely answer to that question – in conjunction with an unfunded global sovereign liabilities bill well north of $100 trillion – has many downstream implications, but we continue to think one of them is that it may make sense to own portable, apolitical scarce assets just in case they catch on.

As the world’s largest investor focused on the convergence of bitcoin, energy, and AI, Ten31 has deployed over $200 million across two funds into more than 30 of the most promising and innovative companies in the ecosystem. Visit ten31.xyz/invest to learn more and get in touch about participating.

Selected Portfolio News

AnchorWatch launched multi-institution custody support, allowing customers to leverage the company’s uniquely powerful Trident Vault technology and optional 1:1 insurance coverage without holding private keys directly:

Fold launched the first bitcoin gift card for TikTok users:

Media

Ten31 Managing Partner Marty Bent appeared on the Bitcoin News show to discuss how he sees bitcoin’s near-term setup.

Market Updates

The Strait of Hormuz was thrown back into its ongoing quantum superposition this week, as Iran told the world it has once again closed the waterway even as a key international maritime group indicated traffic was continuing to flow early in the week.

But the wave function collapsed mid-week as Iran expanded its attacks on targets around the Persian Gulf and the US responded in kind with its own strikes, sending tanker volumes to three-week lows.

In response, President Trump assured the world that the US is prepared to take up the mantle of “guardian of the Strait” for a meager 20% fee (hey, we’re not running a charity here, ok?).

The President walked back the idea of a protection fee shortly thereafter (around the same time as various ships apparently said “nah, we’re good”), but in any case the eruption of new dangers in this maritime chokepoint has clearly increased Middle Eastern urgency to build out alternative export paths to bypass Hormuz entirely (some tinfoil hat enthusiasts might say this is not an entirely unintended outcome).

More specifically, Iraq’s Prime Minister made the trek to Washington this week to sign several MOUs aimed at bringing various US companies into the country to boost oil & gas production, as well as to accelerate work on an Iraq-Syria pipeline that would offer a new non-Hormuz alternative through a partnership with Chevron.

Zooming out, Goldman Sachs estimated that ongoing pipeline projects across the Gulf will be able to facilitate ~45% of pre-war volumes by the end of next year and 60% by 2028, alongside longer-term term plans from Saudi Arabia and others to expand capacity well beyond that.

To be fair, these projects by themselves won’t solve the issue of Iran using targeted strikes and drone attacks to disrupt refineries and terminals in the area, not to mention potential attacks by the Iran-linked Houthis in the Red Sea.

But while the world waits on new pipeline infrastructure to come online, oil prices are moving higher once again, with both WTI and Brent breaking well into the $80+ per barrel range, while diesel surged 20% in just a week.

Even more notably, benchmark European natural gas prices have jumped aggressively, with winter futures contracts now closing in on highs from the spring, contributing to some terrible, horrible, no good, very bad price action across the European sovereign debt complex.

But as we’ve discussed in prior newsletters, the reality is that it’s a relative game, and Nikkei ran a noteworthy piece to that effect this week highlighting that this year’s disruptions have made the US a clear emerging winner on helium exports – a key input to many critical industries, most notably semiconductor manufacturing.

Domestically, the market at least got some positive (if admittedly backward-looking) news this week, as June’s CPI data came in well below expectations, marking the largest monthly decline since spring 2020’s COVID crash as both energy and core inputs came in soft. The PPI also posted an unexpected M/M decline.

A cynic might posit that the headlines out of Iran over the last two weeks suggest this is a local bottom and we’re gearing up for the next move higher, but new Fed Chair Kevin Warsh told Congress this week that the inflation of the last five years will be a thing of the past thanks to better monetary policy and the disinflationary impacts of the AI boom (NB: your latest implicit confirmation that making the AI trade work is the lynchpin for a number of other policy objectives).

Several of Warsh’s colleagues pointed in a similar direction, with Fed Governor Christopher Waller suggesting that rate hikes from here are still possible but that the Fed “shouldn’t fight the last war” by focusing excessively on inflation. New York Fed President John Williams similarly suggested that inflation has peaked and benchmark rates are now well positioned.

They’d better hope that’s the case, as the US’s reported fiscal deficit through nine months of this fiscal year came in slightly higher than the same period last year, with most analysts projecting the US will surpass $2 trillion again on the year (though deficit hawks can perhaps take some small consolation that the Y/Y growth in the deficit has roughly flatlined in the past couple years, even as GDP growth hasn’t yet done enough work to get the deficit down much as a percentage of GDP).

For now, though, Warsh and co may have some breathing room, as Treasuries caught a small bid on the week while bond volatility once again remained pretty subdued despite the clear negative turn in the headlines.

Treasury Secretary Scott Bessent publicly confirmed this week that all the gold held in Fort Knox is still present and accounted for (I mean, what else was he going to say?), which could also offer another rabbit for the US to pull out of its hat if push comes to shove via gold revaluation.

Warsh and Bessent’s AI buildout hopes arguably got some additional positive signals as earnings season kicked into gear this week, with IBM warning investors that its Q2 print will be below guidance given the magnitude of customer spend shifting toward data center capex and AI budgets.

At the same time, industry bellwethers and near-monopolies ASML and TSMC both put up blowout prints, with TSMC increasing its capex guide off an already eye-watering figure. But despite the newsflow, semis and most AI-derivative trades got absolutely trucked on the week, giving everyone their latest reminder of what happens even to great stocks when multiples creep up to 60x+ earnings and everyone convinces themselves it’s cheap on 2030 numbers (pour one our for your local bottleneck bro).

An announcement from Chinese lab Moonshot AI also poured fuel on the fire, as the company unveiled the next generation of their open source Kimi model, which seems to come close to US frontier models on many benchmarks. This immediately triggered all the typical arguments about benchmark-maxxing and token efficiency, and we do think there’s strong reason to be skeptical about the actual impact on the broader AI complex here, but again, it doesn’t take much to ignite a violent selloff after the vertical market performance we’ve seen over the past couple months.

Meanwhile, a new report that Google’s upcoming Gemini 3.5 Pro model has been delayed due to poor performance further dented sentiment, though interestingly the delay seems to be due at least partially to engineers not having sufficient compute capacity to make improvements given internal compute constraints (not exactly a signal of excess supply).

But whatever the excuse / reason, that update won’t help ease nerves in the hyperscaler bond market, which the Wall Street Journal reported is seeing more queasiness from investors in new rounds given the quantity and pace of issuance.

Mag-7 bondholders may perversely get some relief from fears about the capex binge near term as regulatory momentum against the data center buildout is clearly picking up steam, with New York (who would have guessed?) becoming the first state to impose a moratorium on new data center buildouts while well-organized (and totally not astroturfed) activist groups continue to ramp up protests against AI generally.

Amid all these headlines, you could be forgiven for forgetting about bitcoin, and many of its recent buyers certainly have, as the ETF complex set a new outflows record in June. That said, against the aggressive selling, bitcoin’s price has remained largely rangebound, all while historically useful bottom indicators continue to stack up.

Regulatory Update

The American Reserve Modernization Act – the latest strategic bitcoin reserve bill with more than a dozen sponsors – advanced to a hearing by the Financial Services Committee, making it the first SBR legislation to reach the committee stage.

President Trump met with a group of Senators to urge passage of the long-delayed CLARITY Act, though time is running out to get the bill across the finish line before the August recess, in which case the likelihood of passage this year would drop substantially.

Overseas, Japan and South Korea both made updates to their regulatory treatment of bitcoin and digital assets to bring them closer to each country’s traditional financial system.

Noteworthy

The IEA published its latest global critical minerals outlook, which unsurprisingly highlights China’s continued dominance in refined production of most key rare earth minerals.